Investors’ appetite improved during the US session yesterday following headlines saying that Congress Democrats are working on a USD 2.2trln coronavirus-aid bill, that could be voted on next week. Having said all that though, we stick to our guns that equities could resume their slide soon as fears over a second round of lockdown measures around the globe due to the fast-spreading coronavirus remain well entrenched.

Headlines Over A COVID-Aid Bill In The US Support Sentiment

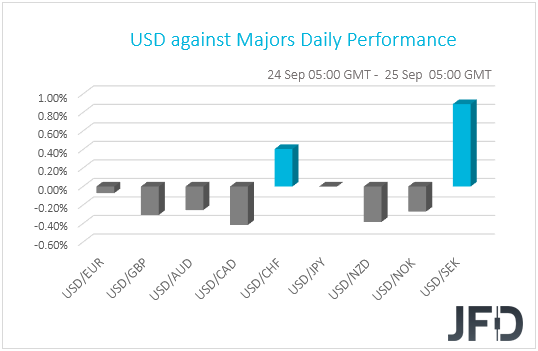

The US dollar traded lower against the majority of the other G10 currencies on Thursday and during the Asian morning Friday. It gained only against SEK and CHF, while it was found virtually unchanged against JPY. The greenback lost the most ground versus CAD, NZD, and GBP in that order.

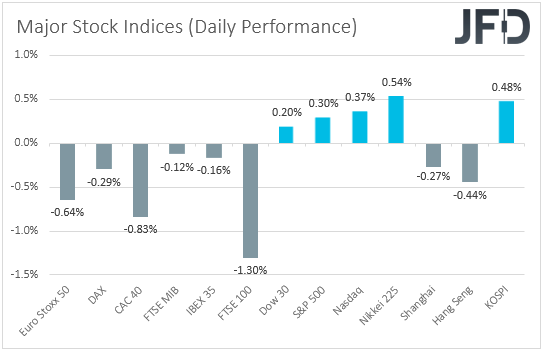

The weakening of the Swiss franc and the US dollar, combined with the strengthening of the commodity-linked currencies Loonie, Kiwi and Aussie, suggests that markets switched to “risk on” at some point yesterday. Indeed, although major EU indices fell, the US ones managed to close their session in positive waters. As for today, during the Asian session, the picture was more on the mixed side. Both Japan’s Nikkei 225 and South Korea’s KOSPI gained 0.54%, and 0.48% respectively, while China’s Shanghai Composite and Hong Kong’s Hang Seng slid 0.27% and 0.44%.

The improvement in investors’ morale during the US session may be owed to headlines saying that Congress Democrats are working on a USD 2.2trln coronavirus-aid bill, that could be voted on next week, with House Speaker Nancy Pelosi reiterating that she is ready to negotiate with the White House.

A USD 2.2trln package is more-than-double the initial 1trln proposal by Democrats and is closer to the 3trln suggested by Republicans, which means that the chances for the two sides reaching common ground have increased. The fact that US new home sales rose to their highest level in nearly 14 years in August may have also helped in lifting US stocks. This followed earlier data showing that existing home sales also hit a 14-year high.

Having said all that though, we stick to our guns that equities could resume their slide soon as fears over a second round of lockdown measures around the globe due to the fast-spreading coronavirus remain well entrenched, and this is evident by the fact that risk appetite softened somewhat during the Asian session today.

We repeat that among currency pairs, those which can better track the broader market sentiment are those consisting of a risk-linked currency and a safe haven, the likes of AUD/USD, AUD/JPY, NZD/USD and NZD/JPY. During periods of market euphoria, these pairs tend to perform very well, while the opposite is true during periods of market turbulence and fear.

Back to the currencies, the pound was among the main G10 gainers after British finance minister Rishi Sunak announced more government support to rescue businesses and jobs. The strength in the pound may have been the reason why FTSE 100 was the main loser among major EU indices. Remember that many companies of the index generate profits in other currencies, so in a strengthening GBP environment, if those profits are converted to pounds, they worth less.

In any case, with the EU and the UK still far apart in reaching a trade deal, we see the case for the pound to come back under selling interest soon, as day by day, the probability of a no-deal Brexit at the end of the year increases. The fact that the BoE is considering adopting negative rates may also weigh on the British currency. Yesterday, BoE Governor Bailey said that they are seeking answers on the suitability of negative rates.

We also had two G10 central banks deciding on interest rates yesterday: the SNB and the Norges Bank. The SNB kept is policy untouched, reiterating that the Swiss franc is highly valued and that they remain ready to step up FX-market interventions when deemed necessary. The Norges Bank kept interest rates unchanged at 0.0% and repeated that they will most likely stay there for some time ahead. With both central banks reiterating the same language as they did at their prior gatherings, the Swiss franc and the Norwegian Krone did not react.

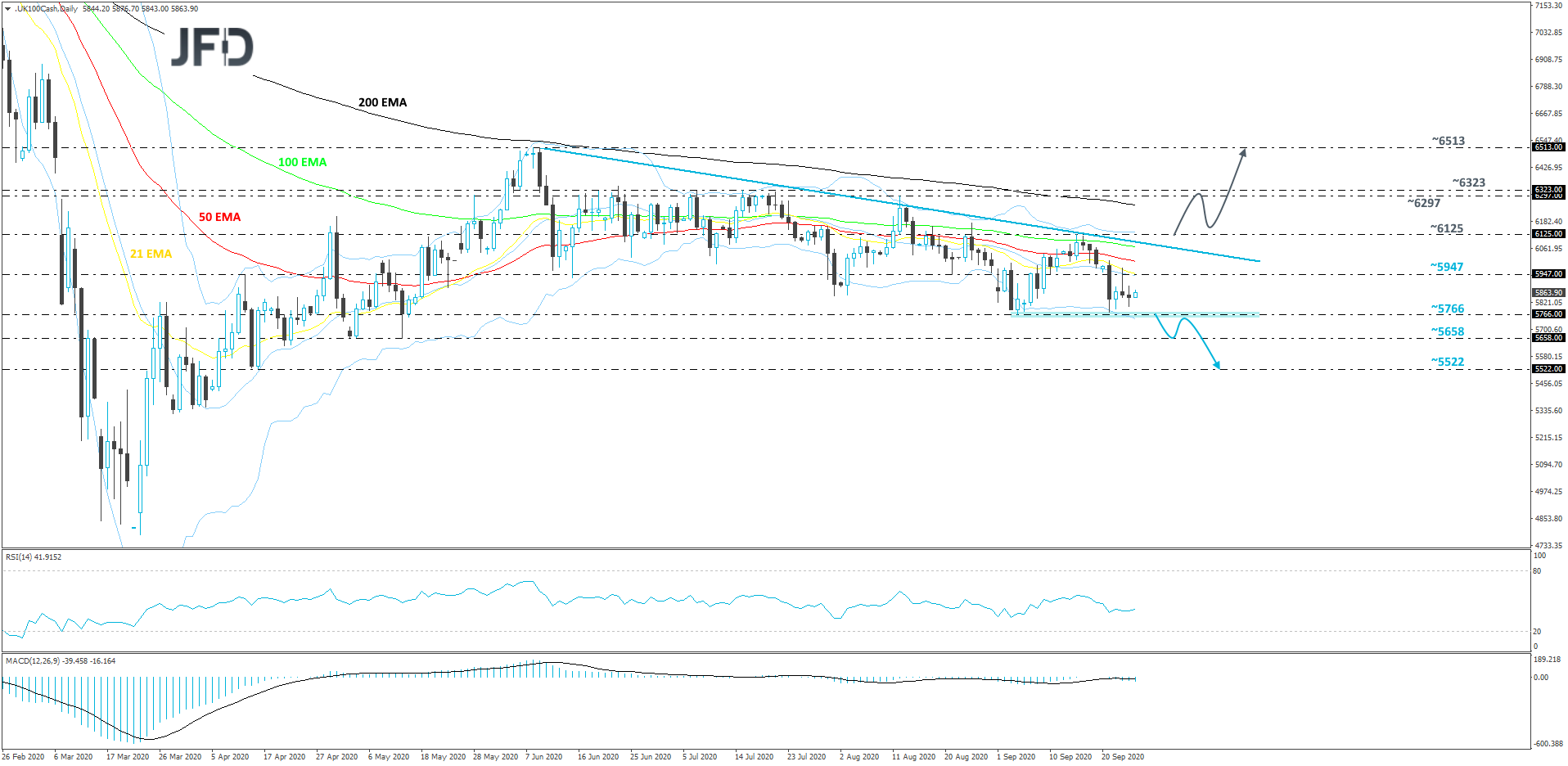

Technical Outlook FTSE 100

FTSE 100 continues to trade below its medium-term downside resistance line drawn from the high of June 9th. Recently, the index came close to breaking one of its key support areas, at 5766, but got halted near it. In order to aim for lower areas, a break of that support hurdle is needed. Until then, we will stay cautiously bearish.

A drop below the previously-discussed support hurdle, at 5766, could attract more sellers into the game, as the move would confirm a forthcoming lower low. That’s when we could target the 5658 obstacle, a break of which may set the stage for a push to the 5522 level, marked by the low of April 16th.

Alternatively, a break of the above-discussed downside line and a price rise above the high of September 15th, at 6125, would confirm a forthcoming higher high and open the door to some higher levels. That’s when FTSE 100 could test out its next possible resistance area between the 6297 and 6323 hurdles, marked by the high of August 12th and the highest point of July. If the buying interest is still high, a further uprise might bring the index to the 6513 barrier, which is the highest point of June.

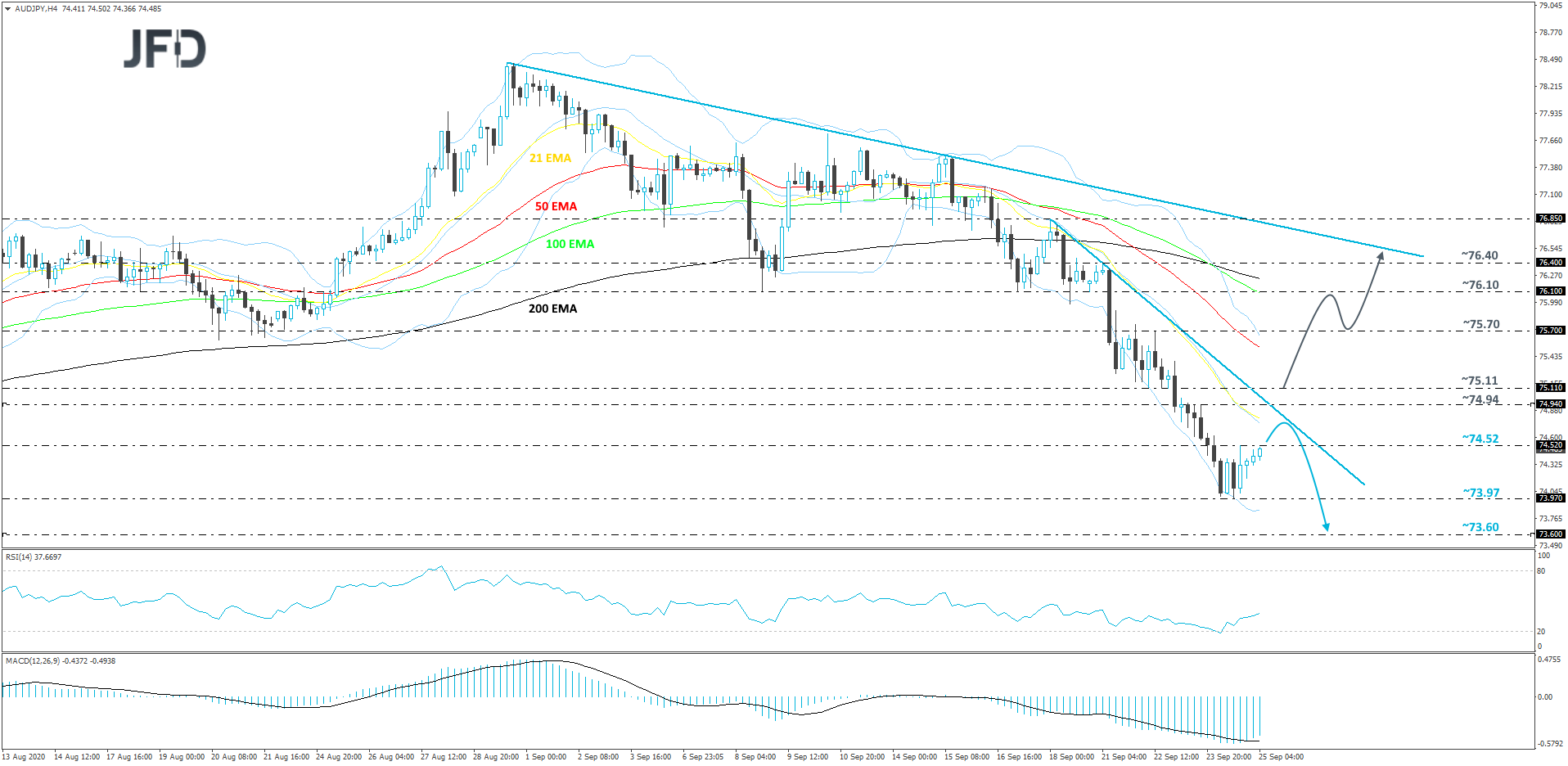

Technical Outlook AUD/JPY

AUD/JPY has been hit heavily by the bears, as seen by this week’s slide. The pair is trading below a short-term tentative downside resistance line taken from the high of September 18th. Although we are currently seeing a bit of a rebound, that might be a classed as a corrective move, if the rate fails to break the above-discussed downside line. We will take a somewhat bearish stance for now.

A push a bit further up may bring the rate to the aforementioned downside line, which if stays intact, could help the bears get back into the game and drive AUD/JPY lower again. The rate could fall back down to the 73.97 territory, which is marked by this week’s current low. The pair might stall there for a bit, but if the bears are still willing to send AUD/JPY lower, this could result in a break of that support territory. Such a move would confirm a forthcoming lower low and may clear the path to the 73.60 level, which is the low of June 30th.

Alternatively, if the rate breaks the previously mentioned downside line and then climbs above the 75.11 barrier, marked by the low of September 22nd, that might temporarily spook the sellers from the arena, allowing more buyers to join in. AUD/JPY could then travel to the 75.70 obstacle, or even to the 76.10 area, marked by the lows of September 8th and 17th.

The acceleration may slow down a bit around that area, but if there is still enough buying interest floating around, the pair could rise again, potentially aiming for the 76.40 level, marked by the high of September 21st. But the upmove might get halted by another short-term tentative downside line, which is taken from the high of August 31st. If the rate is not able to overcome that line, this whole move higher may be considered as a temporary correction.

As For Today's Events

The only release worth mentioning is US durable goods orders for August. Both headline and core orders are forecast to have slowed to +1.5% mom and +1.3% mom from +11.4% and +2.6% respectively.

We also have one speaker on today’s agenda, and this is New York Fed President John Williams .