Monday November 7: Five things the markets are talking about

Market volatility continues with a risk-on rally gaining momentum overnight now that the FBI said Sunday that no new evidence was found to warrant charges against Clinton.

Last week saw global equities slide again, crude oil under pressure on doubts about OPEC’s ability to cut production at its next meeting in Vienna (Nov. 30). Economic data was mixed, as too were corporate earnings, while Friday’s non-farm payroll (NFP) provides a shout out for a Dec. Fed hike. The RBA, BoE, BoJ and Fed all met and left their respective policies unchanged.

The ‘mighty’ dollar is posting strong gains this morning on the perception of increased chances of a Clinton victory over Trump in tomorrow’s U.S. election. Ebbing risk aversion is also helping emerging market currencies.

Data is relatively light this week with releases centering around September industrial production and merchandise trade data. China releases its merchandise trade and consumer and producer price indexes.

Investors’ attention will be on the outcome of the U.S. presidential election.

1. Equities rally hard on FBI bombshell

Europe and the U.S’s nine-day equity loosing streak looks like it may come to and end in today’s session.

Global stocks and the dollar are posting some of their biggest gains in weeks after the FBI said Sunday it stood by its earlier recommendation that “no criminal charges were warranted” against Clinton in her e-mail saga.

The news should allow some investors to shift some of their focus back to U.S. economic fundamentals – solid job gains Friday and a rise in wages has a Dec. Fed hike on the radar.

Asian bourses ex-Japan have rallied +0.9%, its biggest rise in three-weeks. Japanese shares rose +1.2%, the biggest rise in seven-weeks.

In Europe, Euro stocks were up more than +1.3% in early trading. Euro Stoxx gains are being led by financials, while energy, commodity and mining stocks also trading notably higher in the FTSE 100.

S&P 500 futures are pointing to a rise of +1.5% at the open.

Indices: Stoxx50 +1.7% at 3,006, FTSE +1.3% at 6,782, DAX +1.7% at 10,431, CAC 40 +1.8% at 4,457, IBEX 35 +1.7% at 8,939, FTSE MIB +2.2% at 16,679, SMI +1.7% at 7,723, S&P 500 Futures +1.5%

2. Oil bounces on OPEC promises

Crude Oil prices were under pressure last week, dragged lower by a surge in U.S. crude inventories, timid demand and doubts over the ability that OPEC will be able to coordinate cuts.

On the weekend, OPEC seems to have temporarily stopped the rot, again committing to the Algiers accord agreed by 14 members back in September.

Crude has rallied more that +1%, however, prices remain more than -$7 below last month’s high due to persistent doubts over the feasibility of the group’s plan.

Brent futures trade at +$46.20 per barrel, up +62c, or +1.36%, from Friday’s close. U.S. West Texas Intermediate (WTI) crude is up +75c, or +1.7%, at +$44.82 a barrel.

Crude bulls continue to trade against a record OPEC production in October, infighting between Iran and Saudi Arabia, as well as calls from Iraq for its own exemption from any cut.

Risk-on trading has gold under pressure. The yellow metal fell as much as -1.3% to +$1,288.11 ahead of the open stateside. Last week it rallied +2.3% on concerns that Trump may capture the White House. Not helping the commodity is Friday’s U.S employment data, which is boosting the case for higher borrowing costs.

3. FBI news steepens U.S curve

Global bond prices are retreating as investor risk appetite surged across the board.

U.S. 10-Year note treasury yields have backed up +3bps to +1.82%. Bund yields are also up +3bps at +0.16%, while UK Gilt yields were up +6bps points at +1.20%.

Fixed-income dealers expect the U.S yield curves to continue to shift higher on a Clinton win (U.S 10’s to trade to +2%) as the market will be looking for Fed rate “normalization.”

However, market sentiment is likely to deteriorate further if Trump wins. U.S rates should plummet, a similar scenario seen in the immediate aftermath of the Brexit vote.

Elsewhere, the price of protection against defaults by European investment grade corporates has fallen on the news that Clinton will not be facing charges.

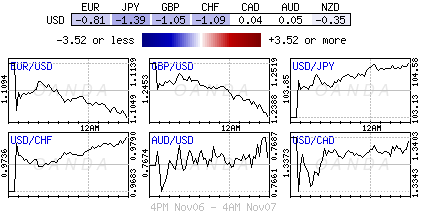

4. Dollar takes control

The “mighty” dollar is posting strong gains on the perception of increased chances of a Clinton victory in tomorrow’s U.S election after the FBI announced no new evidence was found to warrant charges against Ms. Clinton.

Trump’s stance on foreign policy, trade and immigration has unnerved financial markets, while Clinton is seen as the status quo candidate.

The dollar index is trading atop of +0.6%, with EUR/USD down -0.6% at €1.1070, USD/JPY is up +1.3% at ¥104.50 and GBP/USD is down -1% at £1.2410. The MXN and the CAD have both rallied outright, with USD/MXN down -1.8% at $18.620 and USD/CAD down -0.1% at C$1.3394.

Note: A Republican (Trump) win tomorrow would be seen as very negative for these currencies, especially MXN, due to concerns about protectionist policies.

5. Dollar and Sterling politics causing pound problems

On Friday, the pound completed its best weekly gain outright in seven-years –(£1.2150-£1.2548), as investor worries eased that the U.K would undergo a “hard” exit from the EU and lose its access to the single market.

Politics continues to dominate sterling moves, U.K or U.S, overshadowing economic data that is indicating strong growth in the U.K services sectors despite Brexit concerns.

For many, despite last week’s rebound, the pound has remained under pressure since the EU referendum. From a technical perspective, the market believes that the pound needs to trade north of £1.26 with momentum before a possible sustained recovery can be declared.

For now, the market remains content to offload sterling on any rallies.