The US dollar rallied as global equities slumped yesterday. Today, US Treasury yields kept marching north in Asia. A blend of concerns surrounding inflation, a possible US government shutdown, and Evergrande's (OTC:EGRNY) payments gripped the bond market, causing the spike.

All this paints a negative short-term picture in our view, but we will not hold the same stance in the long run. We prefer to take things as they come and reevaluate our outlook whenever we see fit.

Inflation, Debt Ceiling, And Evergrande Concerns Weigh On Sentiment

On Tuesday, the US dollar traded higher against all other major currencies, and the same continued during the Asian session Wednesday. The US dollar outperformed GBP, NZD, and AUD by the most considerable margins while it eked out minuscule gains versus EUR.

The US dollar rallied across the board, especially against commodity-linked currencies such as the Aussie and Loonie. The US dollar spiked against the Pound, which has been volatile lately. This suggests that market sentiment deteriorated once again yesterday.

Turning our gaze to the equity world, we see that major global indices traded in red, tumbling nearly 2% on average as the US Treasury yields kept marching north. The only exception was Hong Kong's Hang Seng, which is up 0.51%.

In our view, it was not just a single trigger that resulted in yesterday's bloodbath. It was a blend of ongoing developments. Firstly, the US Treasury yields may have kept rising on speculation that the surge in inflation is not as transitory as the Fed initially suggested. That could lead to a November tapering move and earlier-than-expected rate hikes after the program has ended.

Secondly, there is an ongoing battle in the US Congress, with Republicans appearing set to strike down Democrats' efforts to extend the government's borrowing authority and avoid a potential government shutdown.

Thirdly, we have the Evergrande saga, with the firm facing its next challenge today as the deadline for another bond coupon payment to offshore investors approaches. Another failure could revive fears that this could affect China's financial system and even impact the rest of the world. Lastly, widening power shortages in China have halted production in numerous factories.

Looking ahead, we see decent chances for equities to extend their declines. Even if we see some small rebounds, we will treat them as corrective bounces. We believe that the developments mentioned above gave investors ample reasons to abandon stocks that were considered overvalued.

That said, we stick to our guns that when the sun shines again, and all these problems will be resolved or forgotten, and equity indices, at least in the US, could rebound and march north, even if the Fed changes its stance on the monetary policy.

All this may already be priced in the current fall. And by any extensions of it, tightening policy means desired economic performance. In other words, we stay somewhat bearish in the short term, but we don't hold the same stance for the longer run. Despite all the concerns, we maintain a cautiously optimistic outlook. In any case, we will take things step by step and reevaluate our view when we deem necessary.

NASDAQ 100 – Technical Outlook

The NASDAQ 100 cash index fell sharply yesterday and briefly dipped below the low of Sept. 20, at 14815. That said, the index rebounded during the Asian session today, returning above that level. Overall, the index remains below the last upside support line drawn from the low on May 19, and thus, we would consider the short-term outlook to be negative.

Even if we see some more recovery today, we see decent chances for the bears to jump back into the action from near the low of Sept. 22, at 14940. This could result in another slide and perhaps a test at the 14715 barrier, marked by the low of Aug. 19. Breaking which, the fall could extend towards the 14525 zone, defined as a support by the low of Jul. 20.

We will start examining the case of a more significant positive correction only if we see a rebound back above 15095. Although the index would still be below the upside line as mentioned above, market participants could still drive the action towards the 15245 barrier, or even Monday's peak, at 15409.

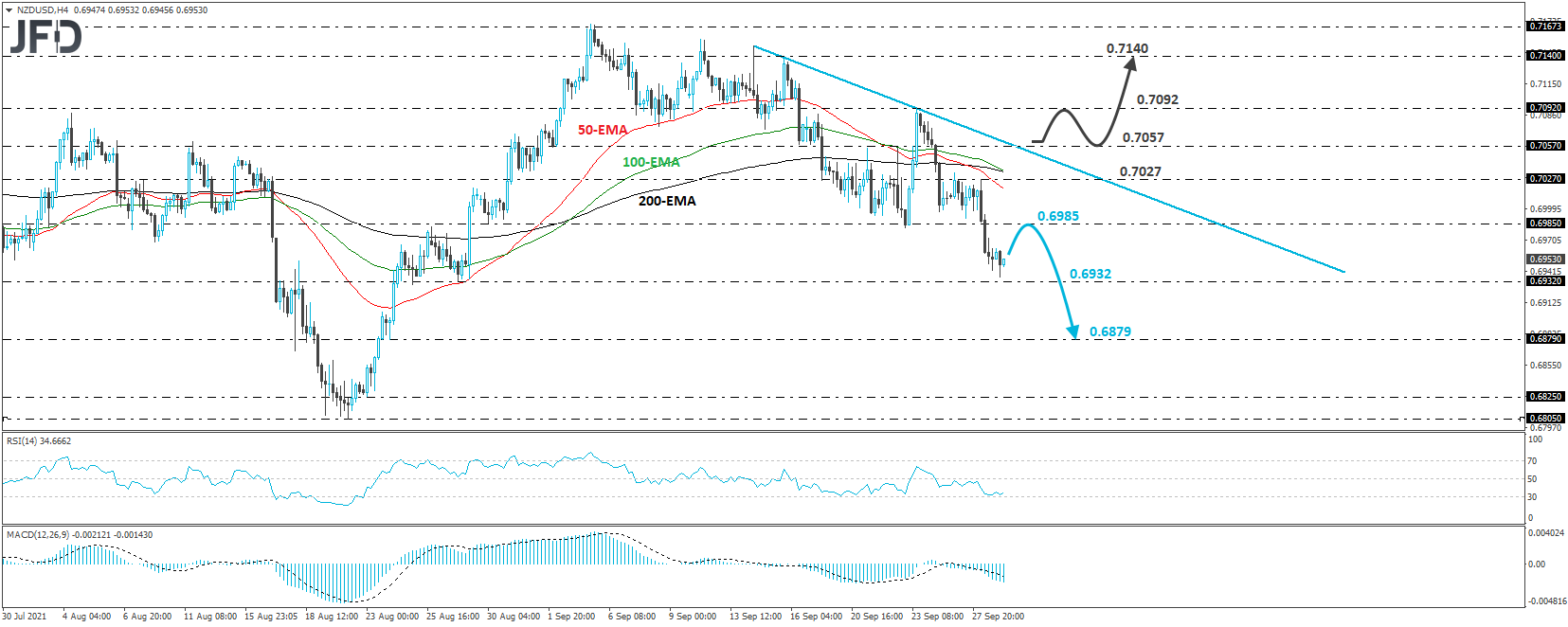

NZD/USD – Technical Outlook

NZD/USD slid yesterday, breaking below the critical support (now turned into resistance) zone of 0.6985. This confirmed a forthcoming lower low on the 4-hour chart and probably the continuation of the short-term downtrend marked by the downside line taken from the peak of Sept. 4. Thus, we will keep a negative stance.

The rate is currently resting slightly above the 0.6932 level, marked by the low of Aug. 27. A slight rebound is possible, perhaps to test the 0.6985 zone as a resistance this time, but the bears may jump in again and push the action back down to the 0.6932 area. A break lower will confirm another lower low and may extend the trend towards the 0.6879 level, marked by the low of Aug. 24.

On the upside, we would like to see a break above 0.7057 before we start examining the case of a bullish reversal. This will also take out the downside line mentioned above. After which, it may initially allow advances towards the high of Sept. 23, at 0.7092. A break higher could encourage the bulls to climb towards the high of Sept. 15, at 0.7140.

As For Today's Events

As we noted yesterday, we have several central bank chiefs speaking at the European Central Bank's Forum on Central Banking. ECB President Christine Lagarde, Fed Chair Powell, Bank of England (BoE) Governor Andrew Bailey, and Bank of Japan (BoJ) Governor Haruhiko Kuroda would be among the speakers.

Besides, it is the second day of Fed Chair Powell's testimony. He will speak before the House Financial Services Committee. It would be interesting to hear what officials say about monetary policy and see whether they provide any clues regarding their plans going ahead.

During the Asian session, we had the leadership elections of Japan's ruling Liberal Democratic Party (LDP), with former foreign minister Fumio Kishida securing victory. Kishida will succeed Yoshihide Suga as the Prime Minister, but he may not hold that position for long as he must call for national elections by Nov. 28.

As for the data, we have Germany's retail sales for August and the US pending home sales for the same month.

During Thursday's session in Asia, Japan's preliminary industrial production and retail sales for August are expected. Industrial production is expected to slide again, but at a slower pace than in July. On the other hand, retail sales are forecast to fall, 1.0% MOM, after rising 2.4% the month before.

China's official PMIs for September are also due to be released. But we only have a forecast for the manufacturing index, which is expected to tick up to 50.2 from 50.1.