Should we do anything? That's the question facing two of the most influential central banks today at their respected monetary policy meetings. For Governor Carney at the BoE the market expects it to be a non-event, same decision, same rhetoric and same direction. However, for the ECB, even though the decision should be rather transparent there have been some mixed readings by both the market and investors, leading to a difference of opinion on this morning's outcome. Who can blame them; the ECB can be both straightforward and erratic at the same time.

Last month, Draghi gave notice that today's meet will be an important meeting, and that by now, policy makers would likely have enough data to formulate their next move. The problem - recent economic reports have been mixed, with some indicators pointing to a Euro-zone economy "slowly on the mend" while consumer price growth (+0.8%) remains well below the ECB's target just shy of +2%. This gradual improvement, coupled with the recent "higher" inflation reading for last month along with a stable money market conditions does not require Draghi and company for any immediate action. Most believe the ECB will focus on emphasizing again the fragility of the regions recovery and signal an ongoing bias to ease further. The bulk of the 'dove' talk should be heard in the press conference after the decision.

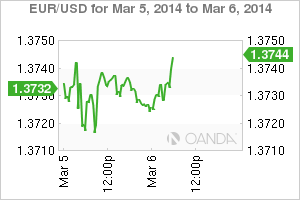

EUR/USD" title="EUR/USD" align="bottom" border="0" height="200" width="300">

EUR/USD" title="EUR/USD" align="bottom" border="0" height="200" width="300">Earlier this week Draghi told the European parliament that the current rate of inflation was way below their target, and that the longer that it hovered at current levels the higher the risk that it would not edge higher to their desired level in any reasonable time. Is this the signal that the ECB will act today? Historically, Euro-policy makers have yet to be that transparent, even though they encourage it. Even the IMF insists that the ECB should cut interest rates and either injects more liquidity into the banking system via its Long-Term Refinancing Operations (LTRO) or start public and private asset purchases. Go with the odds - it favors the ECB keeping rates at their current lows - although easing cannot be ruled out given the prolonged weakness of inflation. By the time the ECB does make up its mind most investors will be onto the next crisis!

For the 18-member single currency, the EUR, overall price action is likely to be volatile and there is a potential for some whiplash developments. Many will expect a "big" day for EUR bears if Draghi and company does happen to deliver any significant policy easing measures. The overall market has been short EUR's outright and on the crosses for most of Q1. The EUR's 6-year downtrend line comes in at the well-publicized 1.3890 levels. Any reason to break above and this market will get even messier because of some large EUR/USD buy-stops building above which could trigger a test of 1.40 quite quickly.

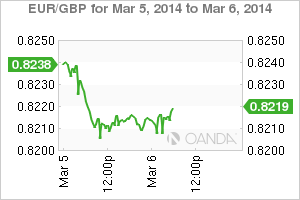

EUR/GBP" title="EUR/GBP" align="bottom" border="0" height="200" width="300">

EUR/GBP" title="EUR/GBP" align="bottom" border="0" height="200" width="300">Central Banks monetary policy has been the curse of the forex markets for months. Lower interest rate policies have handcuffed investment decisions - keeping volatility mostly at bay. Earlier this week new geo-political concerns were able to breath some life back into a contained forex market range. On the whole and despite any vulnerability, currency ranges remain tight, flipping from geo-political to fundamental event risk concerns. For the remainder of this week the market will still have to chew on North American employment even if the ECB fails to deliver.

USD/JPY" title="USD/JPY" align="bottom" border="0" height="200" width="300">

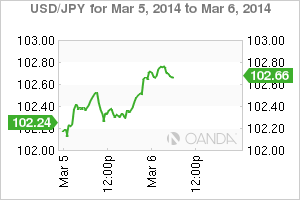

USD/JPY" title="USD/JPY" align="bottom" border="0" height="200" width="300">Yesterday's disappointing US February ADP report certainly tried to dampen Capital Markets enthusiasm. However, even coupled with a weaker non-manufacturing index job component, investors did not seem to over react. The market had expected more "shops" to adjust their US payroll forecasts a tad lower for tomorrow. The reason why they have not is that the ADP headline has been +30-40% above the corresponding NFP data for months, making yesterday's revisions in many people eyes a "catch-up exercise." The miss in the first two months of this year are being marked down to our old foe - the weather. Below is a pool of the leading contenders thoughts with only a couple of changes in opinion.

Goldman Sachs: -20k to +125k

Deutsche Bank: -30k to +120k

UBS: unch at +165k

Citi: unch at +135k

HSBC: unch at +67k

Barclay's Bank: unch at +150k

Jeff: unch at +135K

The RBA did not change monetary policy this week, but Governor Stevens again was vocal about his "historically" high currency value. Last year, his dovish rhetoric was able to walk the AUD down about -15% outright; making it the worst performing developed currency. Aussie data was again the focus overnight with retail sales growth hitting an 11-month high pace (+1.2% vs. +0.4%), while trade surplus came in at a 2-year high. This is obviously good for their economy, but is currently undoing any of the currency softening by Stevens himself this week (0.9057). It's worth noting that the trade surplus was more of a function of "less goods" coming into the economy, as shipments to China fell -12.5% m/m and exports of iron ore were down nearly -10%.

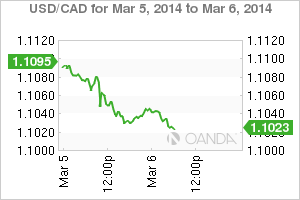

USD/CAD" title="USD/CAD" align="bottom" border="0" height="200" width="300">

USD/CAD" title="USD/CAD" align="bottom" border="0" height="200" width="300">Like all central bankers have been doing the Bank of Canada continues to tout the "downside risk to inflation." Canada is not the exception; inflation remains a primary focus of concern in spite of a recent pick up in consumer prices. Governor Poloz expects that with excess economic slack inflation will be held well below the central banks targeted +2%. As expected by the street yesterday the BoC kept rates on hold at +1%. "The timing and direction of the next change to the policy rate will depend on how new information influences this balance of risk." A statement we have heard many times from many different bankers.