Behind the scenes, TubeMogul Inc (NASDAQ:TUBE) is in a world of hurt. Digital media giant Google has practically run away with one of Tube’s biggest customers.

But this bad break – and its unfortunate future implications – has flown under the radar until now. It’s the first of three negatives threatening to clobber Tube’s share price.

Flash back to last June. Folks in the Emeryville, Calif. headquarters buzzed with anticipation that TubeMogul had seemingly knocked down a king-maker partnership with Mondelez International.

TubeMogul provides self-serve software that allows advertisers to plan, buy and measure the effectiveness of video ads. Its recent customer Mondelez manufactures Oreo, Wheat Thins and various chocolates, gum and candy.

“Mondelez International's digital branding strategy has always been ahead of the curve,” Brett Wilson, TubeMogul's CEO and co-founder said. “The way they harness the power of software to amplify their strategy is groundbreaking and we're proud to enable that in video.”

The deal helped propel the money-losing Tube to its initial public offering last July.

Tube quickly settled into an overvalued spot on the Nasdaq. Though the IPO price got cut to $7 from the originally proposed $11-$13, Tube shares blasted off, quickly gaining 240 percent. Shares settled recently around $16, handing the company a valuation approaching half-a-billion dollars.

But just four months after the TubeMogul announcement, Google and Mondelez held what’s described as contentious behind-the-scenes negotiations.

“Google wanted Mondelez to use DoubleClick Bid Manager, Google’s demand-side buying platform, instead of competitor TubeMogul, to execute the YouTube transactions as part of the deal, and it was using YouTube’s TrueView pricing system as leverage, according to multiple executives directly involved in the negotiations,” Digiday, a website for tech geeks, wrote of the Mondelez-Google negotiations.

Google had pushed Tube aside.

“The Google partnership is one of the most substantial partnerships we’ve done to date. Not only does it give us access to deep and rich consumer insights, as well as measurement and tracking, but we’re also collaborating with Google on these content-creation pilots by leveraging YouTube studios,” said Bonin Bough, Mondelez vice president of global media.

“We believe this new model of high content-creation at low cost will help us craft a path towards the future,” he added (video link).

During Tube’s November earnings call, an RBC Capital Markets analyst asked about the YouTube-Mondelez deal.

But CEO Wilson seemed to gloss over the issue:

“… broadly speaking we thought that the Mondelez announcement was positive. It is yet another large brand signaling that they are shifting TV ad dollars into digital. In this case, into digital video.

“Now this particular announcement was a spend commitment that Mondelez is making with Google as a publisher. We believe that we will continue to be used as Mondelez's software for brand advertising and will be the pipes, if you well, to facilitate any of their publisher buys Google or otherwise. The Mondelez partnership continues to do well.”

During that same earnings call, CEO Wilson’s introduction included this upbeat promotional comment:

“Mondelez (NASDAQ:MDLZ), the world's largest snack company with beloved brands like Oreo, Chip Ahoy! and Wheat Thins, has likewise indicated that they are targeting for 50% of their total ad budget to go into digital by 2016, so it is no longer a question of whether TV dollars will shift to digital. It is just a question of how much of the $200 billion global TV ad market will shift and how long it will take.”

But the promise has fizzled. Now the situation appears to be a jaw-dropping loss for Tube.

“Google’s Mondelez deal called for Google to make YouTube inventory — including TrueView ads — available to be bought programmatically sometime in early 2015, a feature that does not currently exist. The catch was that Mondelez would have to buy that inventory through Google’s DSP,” wrote Digiday.

Mondelez agreed to buy a certain percentage of ads through TubeMogul and use Google for the rest.

And the arrangement describes a greater decline in use of Tube in the future:

“But part of that compromise was an understanding that Mondelez would in subsequent years purchase a greater percentage of its TrueView ads with DBM, and use TubeMogul less,” Digiday reported.

“It’s clear Tube’s technology is nothing special, since Google did this. And besides Google, there’s a lot of other companies that could do the same,” an analyst who requested anonymity told TheStreetSweeper. “There’s no stickiness to their business.”

A Tube federal filing clearly notes the concern:

“A variety of factors outside of our control could affect our revenue growth, including changes in spend budgets of advertisers and the timing and size of their spend.”

So Google’s gain is just the beginning of Tube’s customer base erosion. What’s to keep Google and other giants from snapping up another customer - and another?

On that basis alone, we believe it won’t be long before Tube’s nearly $500 million valuation gets the ax.

Today’s press release about Tube providing the platform, not inventory, for two 15-second Mondelez ads during the Big Game is simply a test of the technology during the football game. This doesn’t cancel out the arrangement that over time, Google will take over most of Tube’s deal with Mondelez.

This also highlights how Tube issues promotional press releases about Mondelez but doesn’t want to talk about Google’s overwhelming threat to Tube’s partnership.

Investors may read other viewpoints on Tube here, but we’ll point out some other jarring bumps affecting Tube.

*Insider sells shares right after lockup expiration. Expect more to follow.

The IPO offered 6.25 million shares. But nearly three times that many shares – 22.4 million – were set aside as restricted shares for Tube officers, directors and other major shareholders.

Insiders were required under a lockup agreement not to trade those shares for 180 days. Those millions of looming shares poised to dilute stock currently held by Tube investors have now been unlocked.

With the stock trading as high as $18.40 - more than double the IPO price - the shares unlocked Jan. 14, 2015.

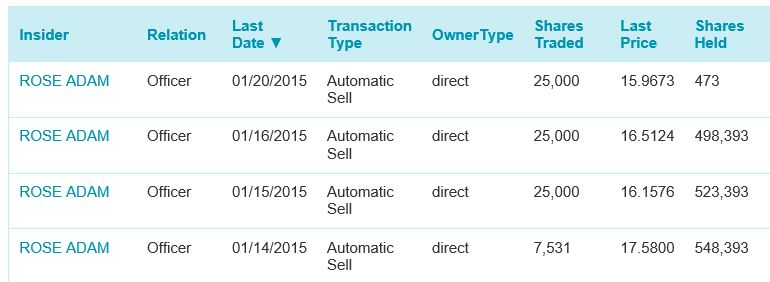

The very day the lockup expired – Bam! – Tube’s chief technology officer Adam Rose sold over 7,500 shares.

Under an automatic sales plan set up and controlled by Mr. Rose, this was the first of four batches the freshly minted millionaire has sold so far, totaling 82,531 shares at an average price of about $16.50.

As of Jan. 20, Mr. Rose had 473,393 shares left (a comma was left off in Nasdaq’s chart below), yet he’s clearly taking a lot of chips off the table, according to the filing.

Interesting that, the day after Mr. Rose's first sale, the CEO stated he knew of no insider selling.

“I’m not selling. I’m not aware of any of our major shareholders that are selling,” CEO Wilson told Bloomberg on Jan. 15, when asked to comment on the apparent sell off of company stock and resulting 20 percent price drop at lockup expiration.

What does Mr. Rose know that Mr. Wilson doesn’t? And if insiders truly believe their company’s future is strong, why sell now?

Furthermore, if the Big Game arrangement Tube announced today is so big, why on earth would insiders be selling shares now?

Mr. Rose may be leading the charge. We expect to see more insiders follow suit at these prices, further pinching the value of shares held by average investors.

*Pricey Stock Compared to Rivals

Perhaps the competition, beginning with customer-grabbing Google, is part of what has spooked the chief technology officer. In this competitive space, Tube finds itself up against 108 prepackaged software companies.

These include flexible, well-heeled household brands like Adobe Systems, Intuit and Microsoft.

Looking at a total of 169 reviews comparing Tube with nine competitors currently offering similar functionality, Tube’s competitors, with rare exception, were rated as performing well. Tube did well with the only two people who reviewed it.

In contrast, 92 people reviewed Google’s product and offered generally glowing reviews. One Google reviewer stated: “It allows us to reach a large audience with an investment that is significantly less than traditional advertising methods such as print advertising.”

Let’s compare two more similar emerging video ad companies, Rocket Fuel. (NASDAQ:FUEL) and Yume Inc (NYSE:YUME). Investors can see from the chart below that Tube – with revenue last quarter falling behind the previous quarter - is outrageously overpriced compared with these peers.

Tube’s price to earnings ratio is spectacularly high, and the often preferred metric - enterprise multiple or EV/EBITDA (enterprise value to earnings-before-interest-taxes-depreciation-and amortization) - also shows Tube is pricey for average investors. It is 4 ½ to 8 ½ times more expensive than the others. That high enterprise multiple also tells bigger companies that Tube would be a very poor buyout candidate.

TUBE FUEL YUME

Price $16 $13 $5

Trailing P/E 4,252 na na

Est. 2015 Sales 155m 631m 207m

Revenue Last Q $27m $102m $ 43m

Revenue Last Q v previous Q -4.5% +10% +6%

In a field with so many tough players, Tube will find grabbing any significant market share very tough going. Market share is vital to profitability. And as Tube noted in a recent federal filing:

“We have a history of losses and we may not achieve or sustain profitability in the future.”

Conclusion:

Tube has essentially lost a major customer to Google (NASDAQ:GOOGL), its newly unlocked shares are getting dumped on the market as Tube’s chief technology officer issues a lack-of-confidence vote in her own company, and Tube is extremely expensive and tiny amid well-heeled, proven competitors. Finally, even if the company does develop a distinguishable product, Tube is way too pricey to be a buyout target.

There’s a lot of bad news here. In our opinion, Tube stock is going right down the tubes.