Although we don’t have any major central bank decisions on this week’s agenda, the calendar appears much busier than last week, with several important data points having the potential to well affect expectations around monetary policy.

Among them are a bunch of UK data releases, including the CPIs, employment and retail sales, the Australian employment report, the Canadian CPIs, and the US retail sales. We also get the minutes from the latest RBA gathering, as well as speeches by Fed Chair Jerome Powell, and several other important central back officials.

On Monday, during the Asian session, we already got China’s industrial production, retail sales, and fixed asset investment, all for the month of April. Industrial production shrank 2.9% yoy, retail sales fell 11.1% yoy, while fixed asset investment slowed to +6.8% yoy from 9.3%, all three of them missing their consensus forecasts. In our view, this suggests that China’s zero-COVID policy is hurting the economy more than initially estimated and raises more concerns with regards to spillover effects to the rest of the world. That’s maybe why we saw China’s Shanghai Composite trading lower this morning, despite the decent rebound on Friday.

Remember, on Friday, we noted that the rebound may be the result of short covering and portfolio rebalancing at the end of the trading week. We stick to our guns that there is still room for further declines in equities, as the fundamental landscape has not change much. The cocktail of developments affecting the financial world are still global growth concerns, expectations over fast tightening by some major central banks, especially the Fed, and the uncertainty surrounding the war in Ukraine.

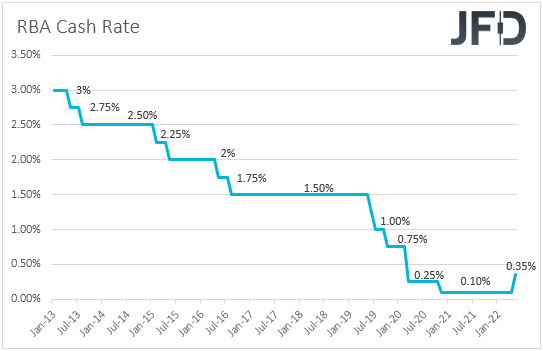

On Tuesday, during the Asian session, we get the minutes from the latest RBA meeting, where the Bank hiked interest rates by more than expected and committed to doing what is necessary to ensure that inflation returns to target over time. Officials explicitly said that this will require a further lift in interest rate over the period ahead.

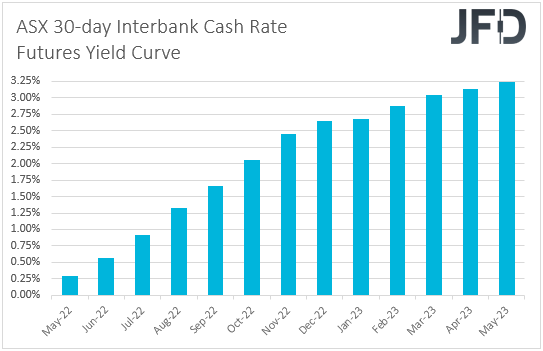

This added some credence to the overly hawkish market expectations around this Bank’s future course of action and resulted in a spike higher in the Australian dollar. However, officials have yet to confirm how fast they are willing to proceed, and it will be interesting to see whether the minutes will give any information on that front. According to the ASX 30-day interbank cash rate futures yield curve, market participants are anticipating another 25bps hike in June, while they see the rate exceeding 2.5% by the end of the year. Anything validating more those expectations could support the Australian dollar, while the opposite may be true in case the narrative is more cautious.

Having said all that though, even in the Aussie strengthens on a potential hawkish outcome, we would treat this as a corrective bounce of its recent short-term downtrend. It seems that the currency is not responding that much to expectations surrounding monetary policy lately, rather than concerns over the global economic performance, and especially the Chinese economy, as China is Australia’s main trading partner.

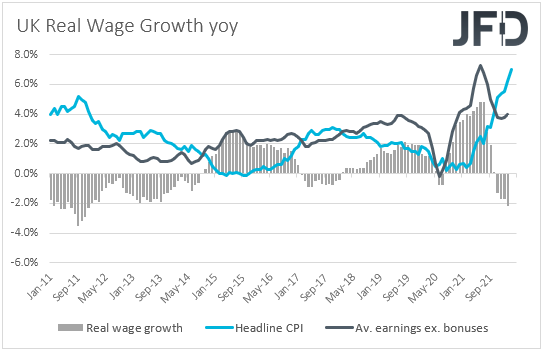

A few hours later, during the early European session, the UK employment report for March is coming out, with the unemployment rate expected to stay unchanged at 3.8%, and the net change in employment to show that the economy has gained 5k jobs in the three months to March, compared to 10k in the three months to February. Those numbers are very low compared to the numbers we got in the period from July to October last year, and in our view, following last week’s disappointing GDP data, they add to fears over a recession in the UK economy next year. Remember that those concerns have officially been expressed by the BoE at its latest monetary policy meeting, with officials projecting a 0.25% contraction for 2023.

Average earnings including bonuses are expected to have grown 5.4% yoy, the same pace as in February, while the excluding bonuses rate is forecast to have risen to +4.2% from +4.0%. However, with inflation well above those numbers, real wages are still negative, which adds another reason why the BoE needs to keep rising interest rates, but also be careful over hurting the economy more.

Our base-case scenario is that the BoE will not stop hiking, but the pace moving forwards may be slower than previously estimated. This is likely to leave the pound vulnerable to more declines, especially against the US dollar. Remember that the Fed is widely anticipated to continue delivering double hikes.

From the Eurozone, we get the second estimate of the GDP for Q1, alongside the employment change for the quarter. The GDP numbers are forecast to have confirmed their preliminary estimates, while there are no projections for the employment change, and thus, we don’t expect this set to affect the euro much.

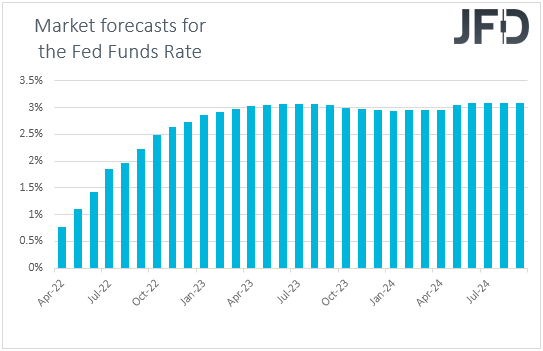

During the US session, we get the US retail sales and the industrial production, both for April, while we will get to hear from Fed Chair Jerome Powell. Headline sales are forecast to have accelerated somewhat, to +0.8% mom form +0.7%, but the core rate is forecast to have slid to +0.3% mom from +1.4%. Industrial production is also expected to have slowed, to +0.4% from +0.9%. Despite the potential slowdowns, we don’t expect any major changes to market expectations around the Fed’s future course of action from this data set.

After all, Fed Chair Powell is very likely to reiterate his view that 50bps hikes are on the table for the next couple of meetings. That said though, given that investors are already aware of that view, and that they have already adjusted to that, we expect them to pay attention to what other Fed officials have to say during the week. In our view, even if we don’t get more hawkish remarks than those of Powell, as long as there is more support over double hikes, the US dollar could continue to benefit, as the Fed will stay among the most hawkish, if not the most hawkish major central bank.

On Wednesday, during the Asian session, we get Japan’s GDP for Q1, with expectations pointing a 0.4% qoq contraction, after a 1.1% expansion in the last three months of 2021. This could add to concerns over the global economic performance, but we don’t expect it to hurt the yen much. Actually, due to its safe-haven status, the yen has been attracting flows from such concerns. Therefore, even if there is an initial slide to the release, we don’t expect it to be significant or last for long.

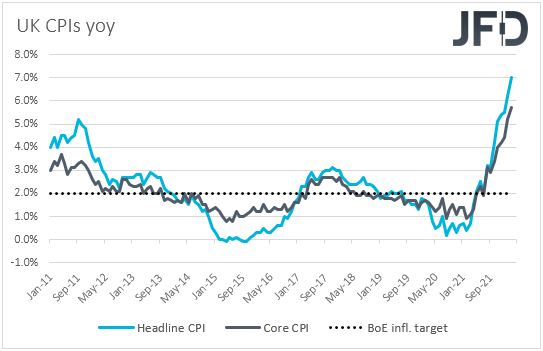

During the early European morning, we get the UK CPI data for April. The headline rate is expected to jump to +9.1% yoy from +7.0%, while the core one is forecast to rise to +6.2% yoy from +5.7%. This could add credence to our view of more rate hikes by the BoE, but the economic wounds and the risks over a recession could keep the path slow, at least slower than some other major Banks. Adding to fears over those risks may be the retail sales data due out on Friday, which are forecast to reveal another month of contraction.

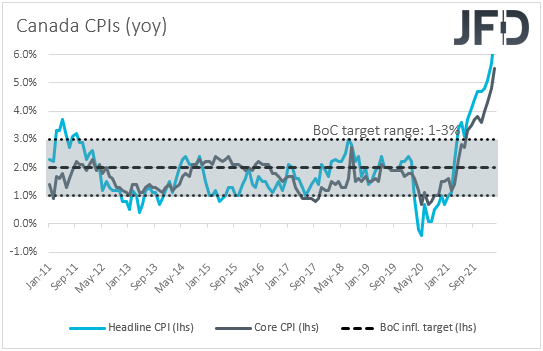

Later in the day, we get more CPI data for April, this time from Canada. The headline rate is forecast to have held steady at +6.7% yoy, while the core one is anticipated to have declined to +4.2% yoy from +5.5%. At its latest gathering, the BoC decided to hike rates by 50bps as was expected, noting that interest rates will need to rise further. Governor Macklem specifically said, “We need higher rates, and the economy can handle them”, adding that they are prepared to move as forcefully as needed to get inflation on target.

However, a decent slowdown in underlying inflation may be an indication that this Bank, although within the hawkish group of the majors, may not need to hike as fast as initially estimated, or at least not as fast as the Fed. Something like that could result in another upside wave in USD/CAD.

On Thursday, Asian time, Australia releases its employment report for April. The unemployment rate is forecast to have ticked down to 3.9% from 4.0%, while the net change in employment is forecast to show that the economy has added 30k jobs after gaining 17.9k in March.

Overall, these numbers point to a decent report and may support somewhat he Aussie, especially if the minutes add some credence to market expectations around the RBA’s future course of action. However, as we already noted, we stick to our guns that the Aussie is likely to stay in a downtrend mode. Due to its risk-linked status and its close trade relationship with China, it is feeling the heat of global growth concerns more than monetary policy expectations.

Finally, on Friday, during the Asian trading, Japan’s National CPIs for April are coming out, but we don’t expect yen traders to pay much attention. We believe that they will stay focused on developments pointing to how the global landscape is affected. Just for the record, there is no forecast for the headline rate, while the core one is expected to rise to +2.1% yoy from +0.8%. Though a decent jump to fractionally above the Bank’s target, it is still well below the high numbers in other major economies, and thus, we don’t expect BoJ policymakers to start thinking altering their monetary policy after that.

New Zealand’s trade balance is also coming out, while later, during the early European morning, as we already noted, we get the UK retail sales for April, with both the headline and core rates expected to have risen, but to have stayed in negative territory.