Forming positions in the USD/JPY depending on the results of the FOMC meeting

Is the Japanese yen a safe haven or has it already lost this status? The question stirred investors' minds for most of 2018. Neither the trade wars, nor the panic on the markets of developing countries, nor the fall of the Shanghai Composite by 25% from the levels of annual highs prevented the USD/JPY bears from getting dividends. The pair soared by almost 8% in six months. It would be understandable if the yield of 10-year Treasury bonds steadily moved north, but the rates settled near the 3% mark and did not rush to grow. The yen's correlation with the VIX fear index fell from -0.6 in mid-2016 to -0.22, which is another argument in favor of the theory that the yen has lost status of a reliable asset.

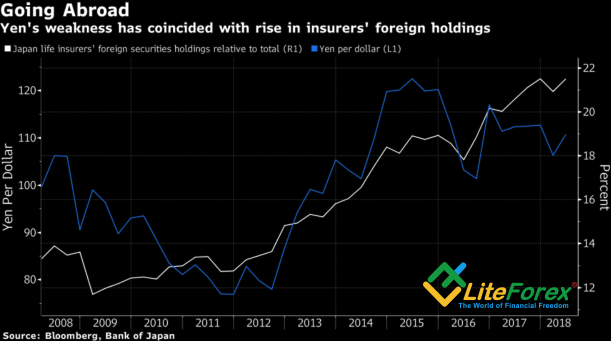

In my opinion, the USD/JPY has two key bullish drivers: disappointment with the BoJ's reluctance to normalize monetary policy and the flow of capital from the Land of the Rising Sun to other regions, including the United States. In the second quarter, the share of foreign securities in the portfolios of Japanese pension funds increased to 22%. Their total value is ¥ 377.8 trillion ($ 3.4 trillion). In general, in April-June, the companies purchased twice as much shares and bonds abroad as in January-March.

Dynamics of the USD/JPY and the share of foreign securities in portfolios of Japanese insurance companies

Source: Bloomberg.

As the main reason for the flow of capital from Asia to the United States is the BoJ's policy of targeting the yield curve. By keeping rates low, the regulator, on the one hand, stimulates the economy and, on the other, deprives those who need it of the ability to earn. Pension funds and insurance organizations are forced to look outside the Land of the Rising Sun, which, contrary to the favorable external background for the yen, contributes to its weakness.

At the same time, the bulls USD/JPY is disappointed by the Bank of Japan's unwillingness to normalize monetary policy. The impressive yen start in 2018 intensified rumors of the completion of the QE and the BoJ's refusal of negative interest rates. Investors believed that the yen would repeat the fate of the euro that strengthened at the end of 2017. Alas, a few months have passed, and it's still there. The Governing Council is not going to make adjustments to monetary policy, and the expansion of the trading range for bonds from +/- 0.1% to +/- 0.2% is considered an additional incentive.

At the same time, in his last speech, Haruhiko Kuroda noted that the time has come when the central bank should weigh risks and compare the effectiveness of cheap money policy and its side effects. I do not think that such a worldview implies the possibility of expanding the QE, so the supply is completely transferred to the side of the Fed. If, following the results of its September meeting, the FOMC raises the forecast for the federal funds rate from the current 3.25% by the end of 2019, then the USD/JPY will continue the rally in the direction of the upper boundary of the previously designated trading range 109-113.5. On the contrary, Jerome Powell's dovish rhetoric and worsening of the estimates of the trajectory of the rate will not allow the bulls to gain a foothold above 112.8.