We live in a time with unprecedented and simultaneous easy-money policies from the world’s largest central banks; the Federal Reserve, the European Central Bank, and the Bank of Japan. Easy money policies, without question, distort asset prices, which speaks to investment risk. However, as we witnessed between 1998 and 2000, distorted asset prices and stretched valuations can remain in place for much longer than traditional fundamentals would suggest, which speaks to an opportunity to profit.

More On Bubble Blowing Front

When the Federal Reserve buys bonds in the process known as QE, they inject freshly printed greenbacks into the global financial system. That “liquidity” can create demand for other assets, such as residential real estate or stocks. Monday’s session was influenced by pro-printing statements from James Bullard. From Reuters:

The Federal Reserve should not rush a decision to scale back its asset purchase program because of low inflation, a senior U.S. central banker said on Monday. “For me, you don’t have to be in a hurry because of low inflation,” St. Louis Federal Reserve President James Bullard told CNBC television.

PEs vs. Technical Analysis

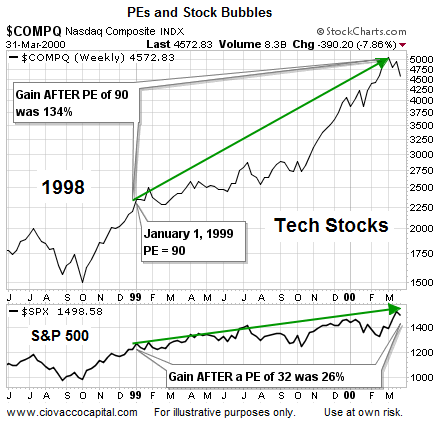

If global central bankers inflate asset bubbles in the coming years and we hope to profit as prices rise, it is important that we have a proven method to monitor the market’s risk-reward profile. Said another way, we need to have some method to manage portfolio risk as prices rise. Were price earnings ratios (PE) a helpful risk-management tool during the final euphoric stages of the dot com bubble? The text below is from a January 1, 1999 posting on The Street.com:

However, I did just get my morning email from Don Hays at Wheat First Union. In the email he talks about the P/E on the Nasdaq: “As you know, we have been concerned with the S & P 500’s all-time-record-high price-to-earnings ratio soaring to 32.19. But based upon our calculations this morning, the Nasdaq Composite makes that look dirt-cheap. Our calculated price-to-earnings ratio for the Nasdaq Composite is 90.2. That is not a typo.”

What level of returns were available to investors in the NASDAQ after January 1, 1999? As shown in the chart below, with a PE of 90, the NASDAQ gained an additional 134% from January 1, 1999 to the euphoric peak in March 2000. With a stretched PE of 32, the S&P 500 gained an additional 26%.

Stocks Are Worth What The Market Is Willing To Pay

The moral of the story is PEs make lousy timing tools. The previous statement is indisputable based on historical facts. From a timing perspective, standing aside based on stretched valuations in stocks on January 1, 1999 meant you would have been wrong for the next fifteen months and missed a 26% gain in the S&P 500 Index. Avoiding the NASDAQ based on stretched valuations on January 1, 1999 meant you would have been wrong for the next fifteen months and missed a 134% gain.

As traders and investors, our job is to make money and manage risk within the present day global financial system. Understanding the system is quite a bit different than agreeing with or being comfortable with the system. If we understand how asset prices are set, we can better discern between favorable and unfavorable risk-reward environments, which is the key to long-term investment success.

Can Investors Participate During Market Advances?

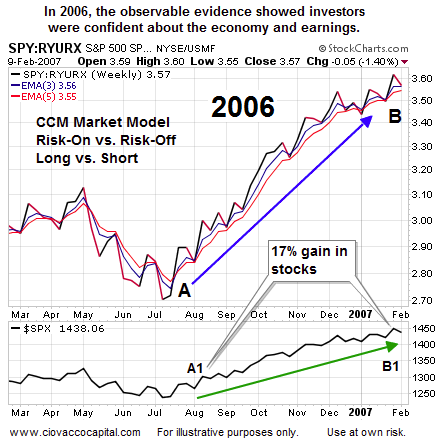

When markets peak, it is logical to assume that investor demand for stocks begins to drop relative to (a) more conservative assets, such as bonds, or (b) risk-off assets, such as inverse stock ETFs (aka shorts). The charts below show how monitoring the demand for longs (SPY) vs. shorts (SH) can assist us with managing risk while attempting to profit from a rising stock market. This video clip describes how the ratio of longs vs. shorts below helped identify the favorable risk-reward environment that existed in 2006 as the S&P 500 gained 17% between point A1 and B1. The short explanation is when the demand for longs is greater than the demand for shorts it indicates bullish economic conviction is greater than bearish economic conviction. During periods of bullish economic confidence, the ratio below rises, which it did in 2006 when the S&P 500 tacked on 17%.

Can Investors Manage Risk When Bubbles Pop?

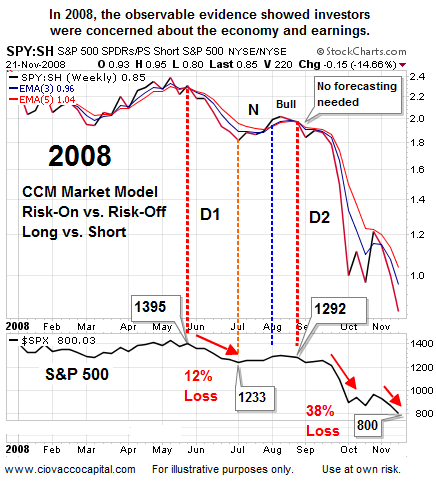

This video clip describes how the ratio of longs vs. shorts below helped identify the unfavorable risk-reward environment that existed in 2008 as the S&P 500 experienced a 12% loss in June, and another 38% drop in Q4. Unlike 2006, in 2008 economic conviction was clearly lagging economic fear during the periods where the S&P 500 dropped (the ratio was also in a bearish downtrend).

Fed 2013: There Is No Rush

By placing an emphasis on moving at a measured pace, Federal Reserve Board Governor Jerome Powell echoed the dovish comments from James Bullard. From Reuters:

“What is reasonable to expect us to do is to be transparent and to move gradually when it is time to withdraw accommodation, or even to begin reducing the pace at which we add accommodation and go slowly in doing that,” Powell told the Asia Economic Policy Conference. The Fed should also “hold to our obligation to only do that as demand does strengthen in the United States,” he said. “Those are the things that we can do and we must do, should do.”

How About The 2010 Flash Crash?

The 2007-2008 peaking process in stocks took several months. Did the observable evidence provide warning signals before a much faster bearish event, such as the 2010 flash crash? The text below from The Economist serves as a refresher course on the 2010 plunge in equities:

On Friday October 1st, America’s Securities and Exchange Commission and its Commodity Futures Trading Commission issued a joint report on the “flash crash” of May 6th. That afternoon, American share and futures indices went into a seemingly inexplicable tailspin, falling 10% in a matter of minutes, with some blue-chip shares briefly trading at a penny, only to recover most of the lost ground before the end of the trading day. The short-lived plunge raised awkward questions about whether trading rules had failed to keep up with markets that now handle orders in milliseconds.

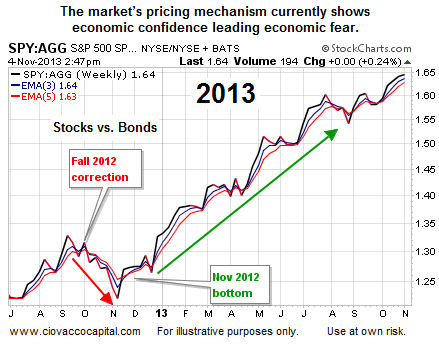

The weekly chart below shows the performance of the S&P 500 (SPY) relative to bonds (AGG). When the ratio falls, it reflects weak demand for stocks relative to the demand for bonds. Common sense aligns with demand for conservative bonds increasing as investors begin to question the economy, earnings, or the stability of the financial system. Three trendlines were violated in a bearish manner on the chart below before the flash crash, which showed demand for bonds was increasing relative to stocks. The lower portion of the chart shows the S&P 500 also violated a trendline 10 days before the flash crash, which told us economic confidence was losing ground to economic fear.

Investment Implications - Skewed Markets Require Flexibility

In October, we listed flexibility as one of the keys to investment success. When financial markets rise with an unbalanced skew toward speculation relative to economic fundamentals, stocks can drop faster than they would in a more healthy and balanced environment. As long as the observable evidence shows a bias in favor of economic confidence relative to economic fear, we will continue to hold a risk-on allocation, which includes broad U.S. exposure (SPY) and money printing friendly ETFs, such as energy (XLE), small caps (IWM), foreign stocks (EFA), and emerging markets (EEM).

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Stocks Bubbles: Can You Profit While Monitoring Risk?

Published 11/05/2013, 01:17 AM

Updated 07/09/2023, 06:31 AM

Stocks Bubbles: Can You Profit While Monitoring Risk?

Money Printing Brings Opportunities And Risk

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.