- Spanish growth tied to exports

- Tepid rise in US consumer spending

- ISM data expected to be on the rise

Tuesday is a busy data for economic reports, including an early look at June’s macro profile for Spain via Markit’s manufacturing purchasing managers index (PMI). Keep in mind that flash estimates are not published for this number and so today’s report will be one of the first data points for assessing Europe’s fourth-largest economy for last month. Later, we’ll see US numbers on weekly retail store sales and the ISM Manufacturing Index.

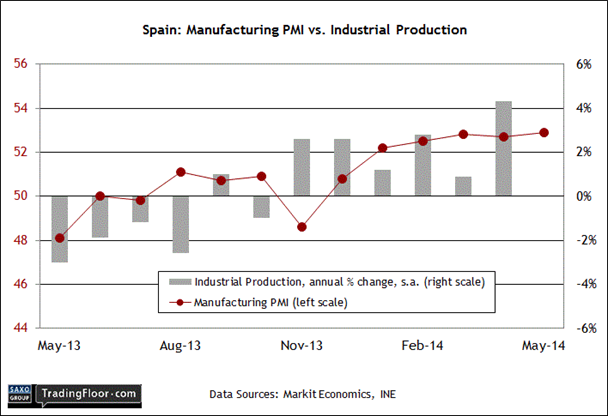

Spain: Manufacturing PMI (07:15 GMT) Spain suffered the most among Europe’s big four economies in the past several years, but now it’s arguably showing the strongest recovery momentum. There is still a long way to go to repair the damage, but the upside potential looks increasingly robust.

Germany is still the continent’s primary growth engine and a critical source of macro stability, but Spain has become the poster child for revival in the Eurozone. “Growth is already boosting employment, opening the way to a virtuous cycle of increased demand and more job creation,” The Economist noted in this week's edition. “Growth predictions for next year are being revised upwards, some to over 2 per cent. Investors have arrived in force, hoping it will soon be party time again.”

Deciding if the encouraging numbers of late are genuine will take time, although there are several reasons for optimism. One is that the recent growth is tied to exports, which suggests that Spain business sector has learned to be competitive on a global scale. That's crucial, given the still weak state of domestic consumption, due in no small part to the high unemployment rate. In any case, an exports-led recovery is a sign that the current revival is based on a fundamental restructuring rather than a short-term pop that's vulnerable to internal shocks.

Today’s business survey data for June will provide an early clue for last month’s macro profile. In the previous update for May, Markit’s purchasing managers index (PMI) showed that “output and new orders continued to increase at solid rates”. The hard data on industrial production confirm that that the brighter mood among manufacturers is linked with higher output. Industrial activity increased more than 4 percent in April on a year-on-year basis, the most in four years. Unsurprisingly, the recovery in the industrial sector has been preceded by encouraging PMI numbers. Today’s update will likely tell us that the positive momentum continued in June.

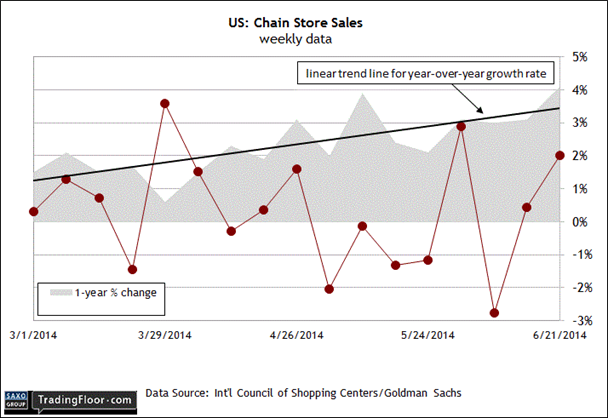

US: ICSC Chain Store Sales (11:45 GMT) Consumer spending rose less than expected in May, increasing a sluggish 0.2 percent - half the rate of the consensus forecast, although higher than the flat performance in the previous month. Nonetheless, the tepid gain raises questions about the outlook for the economy. Consumer spending represents about three-quarters of GDP and so any weakness in spending patterns on Main Street casts a long shadow over the macro outlook generally. But the soft numbers in May aren’t likely to persist in the summer, based on the more-recently updated chain store sales data from the International Council of Shopping Centers (ICSC).

The last two weekly comparisons through June 21 reflect back-to-back gains for the first time since late April. A stronger signal can be found in the year-on-year comparisons, which have been uniformly positive - and rising - for several months. Another round of growth in today’s update would strengthen the case for expecting faster growth in the monthly reports on retail sales and personal consumption expenditures.

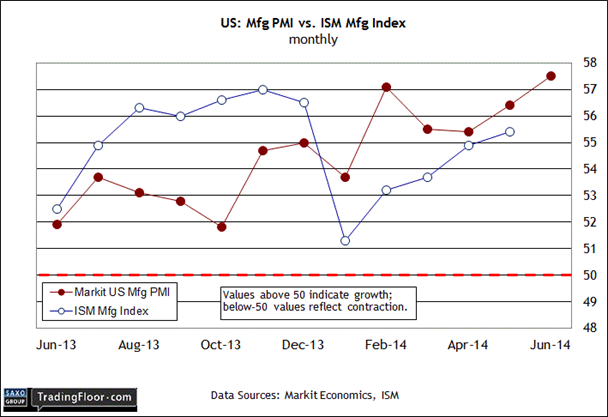

US: ISM Manufacturing Index (14:00 GMT) The cyclically sensitive manufacturing sector in June posted its “strongest improvement” in overall business conditions in four years, according to the flash estimate of the Markit US Manufacturing Purchasing Managers Index (PMI). Rising to 57.5 last month - the highest since May 2010 - the initial PMI number suggests that today’s ISM update will follow suit. Not surprisingly, the consensus forecast sees another round of improvement for the ISM data: 55.6 for June versus 55.4 in the previous month. A marginal gain is also the projection in my econometric modeling.

June’s macro profile is still largely a mystery, but the PMI figures (and the projections for today’s ISM release) imply that the acceleration in economic activity will roll on for the US. We’ll have a deeper look at how the business cycle is faring later this week with June reports on the labour market, starting with tomorrow’s estimate of private payrolls via ADP followed by Thursday’s employment numbers from the government (released a day early because of the July 4 holiday on Friday that will shutter markets and offices in the US).

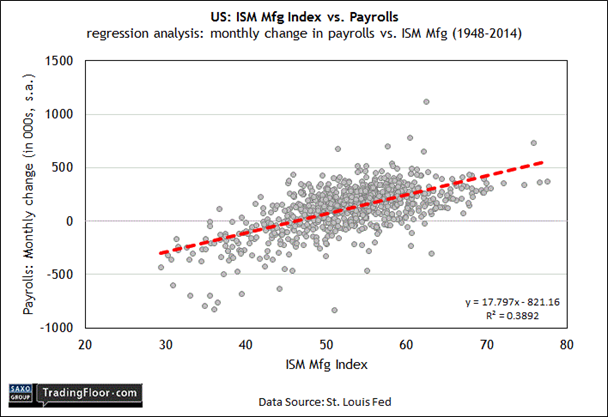

Let’s assume that the consensus forecast for today’s ISM number is right. What does that imply for payrolls on Thursday? One way to formulate a prediction is to take the linear relationship between the ISM and employment numbers, a pairing that stretches back to the late-1940s. As you’d expect, it’s not a perfect relationship (the R-squared is 0.39, which implies at best a modestly tight link, albeit one with a fair amount of noise for any one report). In any case, the numbers imply that a 55.6 June reading for the ISM translates to a gain of 168,000 for payrolls for the month. That’s lower than the 200,000 plus gain that many economists are expecting. Then again, noise infects any one data point with forecasting and so the econometric-based point prediction will probably be wrong. For now, the market’s assuming that it will be wrong on the upside.