This week, we will receive the FOMC minutes from the last meeting held in March. Investors will get reminded about the Fed’s view on the monetary policy outlook. Also, the spotlight will fall on the RBA interest rate decision. The board decided to keep the cash rate target at +0.1% during the previous meeting. Various countries will deliver their final services PMI figures.

Monday will be a quiet day in terms of economic data releases. China will be celebrating the Ching Ming festival, so that the Chinese market will be closed.

Australia will deliver its final MoM retail sales number for February. The current forecast is for the number to rise, going from +1.6% to +1.8%. The actual number managed to meet expectations. From Europe, we will receive the German trade balance figure for February.

The number is expected to increase, going from +9.4bln to +9.6bln. The actual reading showed up even higher. This shows another rise in Germany’s trade balance, which had turned north from last month.

On the same day, the Eurozone will deliver its MoM and YoY PPI numbers for February. Currently, the MoM figure is expected to go down slightly, from +3.0% to 2.3%, whereas the YoY reading is forecasted to rise from +26.3% to 27.0%. From Canada, we will receive the BoC business outlook survey.

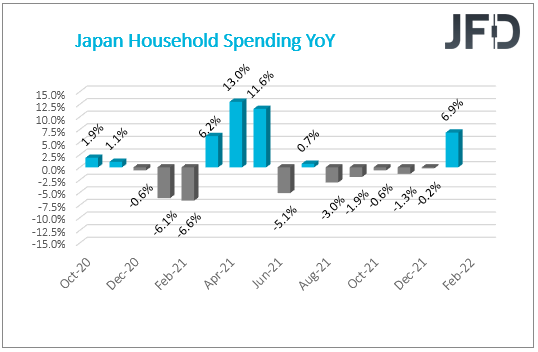

The Chinese market will remain closed on Tuesday due to the continued Ching Ming Festival. Japan, on the other hand, will deliver household spending figures for February on an MoM and YoY basis. The current expectation is to see both numbers decline.

The MoM one is believed to drop from -1.2% to -1.5%, and the YoY figure is expected to go from +6.9% to +2.7%. Suppose the actual numbers come out even below the initial forecasts. In that case, this may create additional problems for the BoJ, to see inflation rising to their target of 2% anytime soon, as this would show that consumers are holding off from spending.

But, probably, the main event during the Asian morning will be the RBA interest rate decision. The board decided to keep the cash rate target at +0.1% during the previous meeting. Although the Bank sees that the global economy has been recovering well from the pandemic, the new concern has become the war in Ukraine and the uncertainty that surrounds it.

Although the RBA is concerned about the rising inflation in various parts of the world, the Australian economy remains resilient, as consumer spending has picked up in recent months. The current expectation is for the rate to stay at the same level, at +0.1%.

During the European morning, the Eurozone is set to deliver the final services PMI number for March. The forecast is for the number to remain the same, at 54.8. Anything above 50 shows that the service sector is still improving.

If the number comes out better than expected, this may give a slight boost for the euro against some of its major counterparts. The United Kingdom will also deliver its final services PMI number for March, which is also expected to stay the same, at 61.0.

The final services PMI data from the US will be on the radar after that. The number is expected to improve from 56.5 to 58.9. However, the services PMI will not be the only piece of data that will come out from the US. The country’s ISM non-manufacturing PMI number will be on the lookout, as it is believed to have improved somewhat, going from 56.5 to 58.0.

On Wednesday, the United Kingdom will release the construction PMI figure for March. The current expectation is for the reading to go down from 59.1 to 57.3. Later on, Canada will take the spotlight with its Ivey PMI figure for March, which is expected to rise slightly, going from 60.6 to 61.0.

If the figure comes out better than the forecast, this may help CAD strengthen slightly against some of its major counterparts. Even if the number comes out better than the previous figure, this will show a continuous rise for the fourth month.

But the main event on the calendar will be the FOMC minutes from the last meeting, held in March. Investors will get reminded about the Fed’s view on the monetary policy outlook. During the last meeting, the FOMC committee decided to hike the interest rates by 25 bps. However, this will not be the last hike this year, as the Fed is preparing for another increase on May 4.

According to the CME FedWatch tool, the current expectation is to see an additional 50 bps hike. Such a move may apply more pressure to the stock market, possibly forcing some investors to move away from equities.

Thursday will be a relatively quiet day too. In the early hours of the European morning, Switzerland will deliver its unemployment rate, both seasonally adjusted (s.a.) and non-seasonally adjusted (n.s.a.). The current forecast for the s.a. number is for it to stay the same as the previous, at +2.2%, and for the n.s.a. figure also to remain at +2.5%.

Germany will be throwing out their MoM industrial production figure for March, which is expected to decline significantly, from +2.7% to -0.2%.

The United Kingdom will show us how the prices in their housing market have changed over the past month, according to the Halifax Bank of Scotland, which is one of the largest mortgage lenders in the UK. The current expectation is for the YoY reading to drop slightly, from +10.8% to +10.4%.

The Eurozone is set to provide us with its MoM and YoY retail sales numbers for February. The MoM one is believed to have improved from +0.2% to +0.6%, whereas the YoY figure is expected to go from +7.8% to +6.2%. Also, the ECB will publish the account of monetary policy from its previous meeting held in March.

The U.S. will be releasing its initial and continuing jobless claims. The initial claims are forecasted to have dropped just slightly, from 202k to 200k. The continuing one is also expected to fall slightly from 1307k to 1302k.

Friday will kick off with Australia delivering the RBA financial stability review. That review, quote,

“Provides the Bank's assessment of the current condition of the financial system and potential risks to financial stability”.

We do not expect AUD to move much after the release of that report.

Europe will be relatively quiet on the economic data front. However, it will be Canada’s turn to release employment numbers for March. The unemployment figure is expected to tick lower, going from 5.5% to 5.4%. Currently, there is no forecast available for the participation rate, but we know that it has been coming out around the same level, slightly above the 65% mark.

The employment change figure is believed to have declined strongly, going from 336.6k to 80.0k. If the actual reading comes out even lower, this could hurt the Canadian dollar. That said, the effect might be temporary, as CAD may remain vulnerable to movements in oil prices.

Some market participants will be keeping a close eye on the Russian inflation numbers, both MoM and YoY for March. The MoM reading is expected to double, going from +1.1% to +2.1%. The YoY one is forecasted to go from +9.2% to +16.9%.

The explanation for such high numbers is clear, as the country is experiencing a shortage in supply of certain imported goods due to sanctions from the West. Also, Russia will deliver its GDP growth rate for Q4, which is believed to have improved from +4.3% to +5.0%.

If that’s the case, this may give the ruble a slight boost against its major counterparts. However, the currency will mostly remain vulnerable to the situation in Ukraine and to the progress in the negotiations between Russia and the EU on the method of payments for Russian gas.