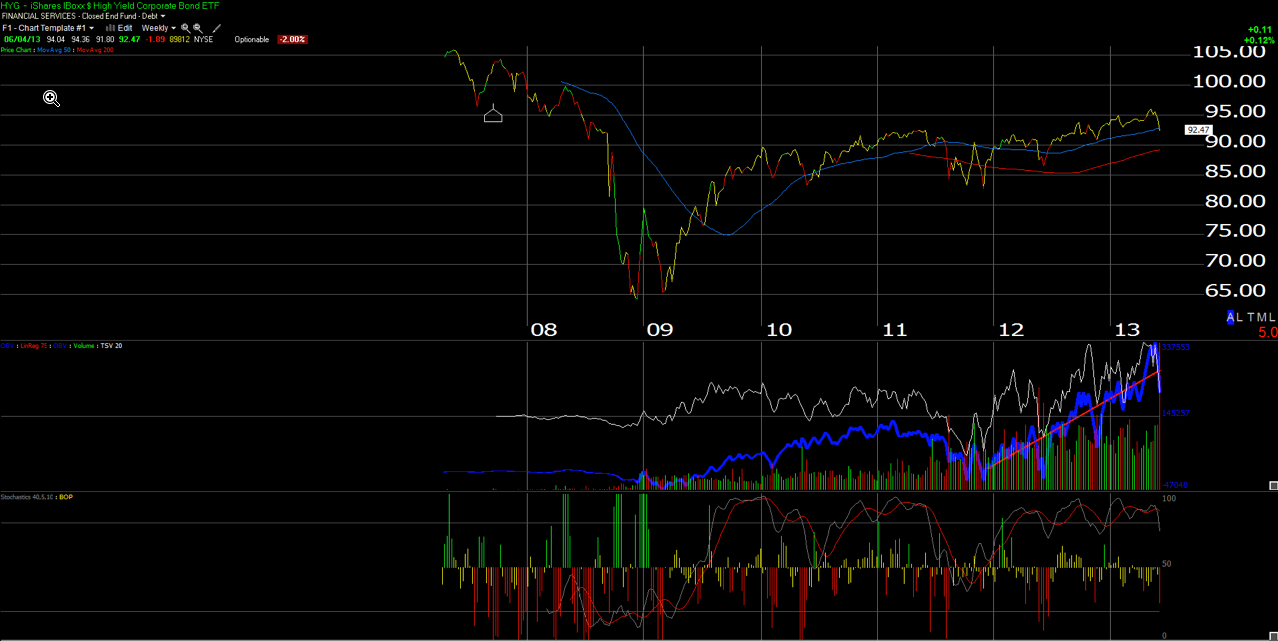

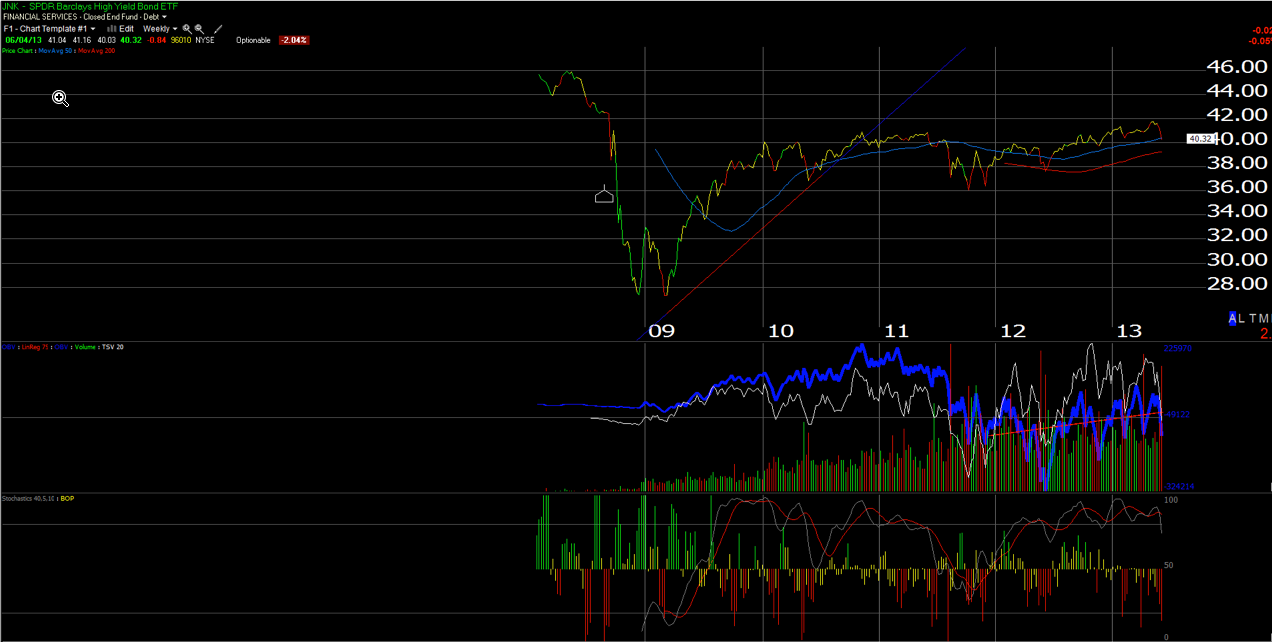

We put two weekly charts up this morning: the two corporate high-yield ETF’s, which show the junk bond market is in correction mode.

Both ETF’s are sitting right on top their respective 50-week moving averages. For both ETF’s to drop to their 200-week moving averages would require another 2% decline.

The corporate high yield (i.e. junk bond market) is considered an early warning canary for the stock market, so it pays to watch what is happening with high yield spreads.

Cheap Risk

Despite the very low level of nominal yields and interest rates, “credit risk” is still thought to be cheap to Treasuries, which means (in English) that the spreads at which corporate credits still trade relative to the equivalent-maturity Treasury security, is still wider than what is considered “normal” or average spreads over time.

The point is that it still pays to be overweight credit risk in terms of portfolio management.

The “average weighting” for corporate high-yield bonds in benchmarks like the AGG and other widely-held, fixed-income benchmarks, is 10% – 15%.

The HYG ETF has a 12-month yield of 6.5% and an SEC yield (according to Morningstar) of 4.6%.

The JNK ETF has a 12-month yield of 6.5% but Morningstar doesn’t provide an SEC yield for the ETF.

Today's Conditions

High-yield tends to outperform when the economy is gaining steam, and corporations are flush with cash, as S&P 500 companies are today. The high yield market tends to be positively correlated with the stock market, in that spreads tend to widen when the SP 500 corrects, and spreads tend to narrow when the SP 500 rises (when looked at over longer-time frames).

Corporate high yield also tends to hold its value better in markets where interest rates rise, if the rate rise is driven by stronger economic growth, as opposed to inflation.

Outlook

We remain overweight corporate high-yield in client accounts as we believe that the U.S. economy is more likely to strengthen over the next 12–18 months, than to enter a recession or near recession.

We like ETF’s vis-a-vis open-ended mutual funds given that it gives us more flexibility to adjust exposure in client accounts.

If you think the U.S. economy will continue to slowly gain strength and continue to work off the poor Washington fiscal policies, then continue to hold high-yield in your portfolio.

Brian Gilmartin, CFA Portfolio

Trinity Asset Management, Inc.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Junk Bond Correction

Published 06/05/2013, 10:47 AM

Updated 07/09/2023, 06:31 AM

Junk Bond Correction

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.