We begin with the United States where the latest PPI report surprised to the downside. Below is PPI and Core PPI change from previous year -- both materially below consensus.

Does this look like an environment to raise rates? Nevertheless the majority of economists still predict a September liftoff.

The futures markets on the other hand are no longer pricing in a rate hike this year, as the mean timing expectation moves to January 2016.

Should the Federal Reserve decide to act this year, the market reaction could be severe. In that sense the markets are telling the Fed - "don't do it".

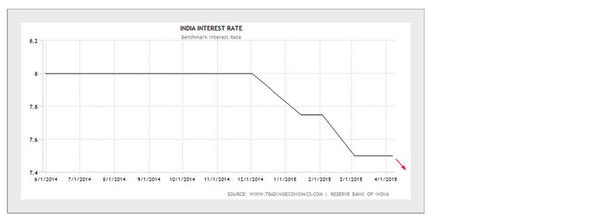

Since we are on the topic of inflation, India had a surprisingly low wholesale inflation print (WPI).

The Reserve Bank of India is likely to cut rates again, particularly if the Fed is on hold for a while. Cutting rates in India while the Fed is hiking could put severe pressure on the rupee - something the RBI would rather avoid.

Bunds selloff continued Thursday morning, with the 10-year rising above 75 basis points.

But global sovereign bond markets stabilised as treasuries rallied on the back of weak PPI results in the US. Moreover, Mario Draghi assured the markets the European Central Bank will stay the course.

Back in the US, the initial jobless claims four-week average touched a new low not seen since 2000. It seems that those who can't find work have already used up their benefits, while layoffs (outside the energy sector) remain low.

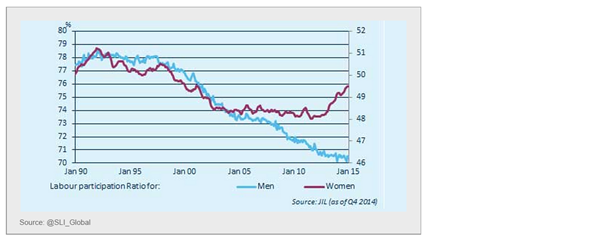

Now some food for thought: Labour shortages in Japan are bringing more women into the workforce. If the trend continues, Japan's economy could benefit tremendously.

Disclosure: Originally published at Saxo Bank TradingFloor.com