Thursday brings the latest updates for several purchasing managers indices (PMI) throughout Europe, although the hard-data report for August retail sales in the Eurozone may be the day’s most revealing number. Meanwhile, amid the ongoing shutdown of the federal government in the US, the available economic data will receive more attention than usual in search of fresh clues on how the economy is holding up. Two of today’s key numbers to watch for the US include the weekly update on initial jobless claims and the Bloomberg Consumer Comfort Index.

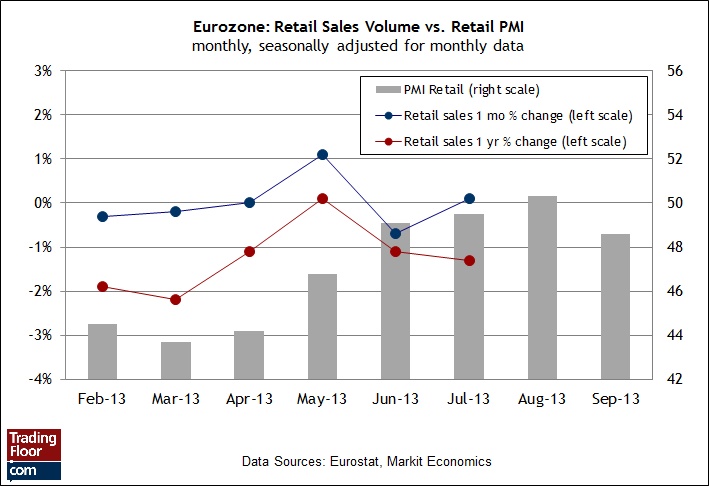

Eurozone Retail Sales (09:00 GMT): Consumer spending picked up a bit in the July report on retail sales in Europe, but the softer numbers in the September Eurozone PMI update suggests that the trend could weaken again. But not today, or so we're told. Analysts say that today’s August report on retail sales will improve relative to the previous release. The consensus forecast sees a 0.2 percent rise for August, up slightly from July’s 0.1 percent advance. Even so, economists still anticipate that the red ink in the year-over-year comparison for retail consumption will slip a bit more, falling 1.4 percent over the 12 months through August versus a 1.3 percent decline in the previous report.

Commenting on last week’s Eurozone Retail PMI report for September, a senior economist at Markit Economics advised in a press release (pdf) that “Eurozone retail sales failed to build on August’s growth, largely due to a reverse in France. But viewed in context the recent data are encouraging, with the underlying upward trajectory of the PMI since April corroborated by official data showing a 0.2 percent rise in consumer spending in Q2.” He added that "German retail growth slowed further in September, but may pick up again following the election result.” Meantime, the market will look to today’s hard data on retail spending for deciding just how much optimism is credible at the moment when it comes to looking ahead for the Eurozone.

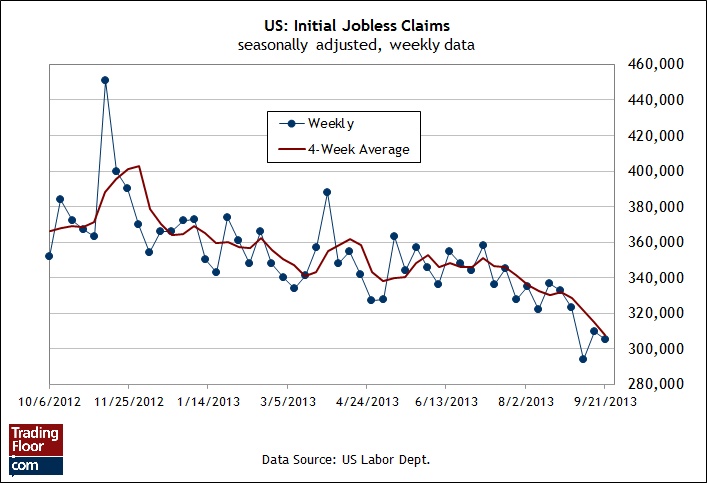

US Jobless Claims (12:30 GMT): Today’s weekly report on jobless claims (assuming it's released) will be especially prized for assessing the labour market if the standoff in Congress over the budget rolls on and non-essential parts of the federal government remain closed. One of the victims of the political war over fiscal matters will be Friday’s monthly payrolls report, which has been postponed until the battle in Washington ends. Meanwhile, yesterday’s ADP Employment Report provides some insight into last month’s payrolls data. September’s private payrolls increased a modest 166,000, up a bit from August’s 159,000 rise, but the latest number still looks sluggish by recent standards. Then again, the year-over-year trend continues to perk up a bit, as I noted yesterday.

In any case, with tomorrow’s official payrolls report on hiatus until further notice, today’s jobless claims update may be the last official data point for gauging the employment trend. The weekly data release is still scheduled for publication, according to one report, although at this stage it's best to assume nothing with US economic news from the government until you have the numbers in hand. Data blackouts aside, the main issue for today’s claims release continues to be one of deciding if the recent sharp drop in new filings for unemployment benefits was largely if not completely due to computer glitches. The last two updates suggest that the decline of late for this series is genuine, but today’s number will be closely watched for any evidence to the contrary. The consensus forecast anticipates that claims will slip to 305,000 on a seasonally adjusted basis versus the previous report's 313,000. If that prediction holds, we’ll have a bullish report that shows layoffs dipping close to the lowest level in six years.

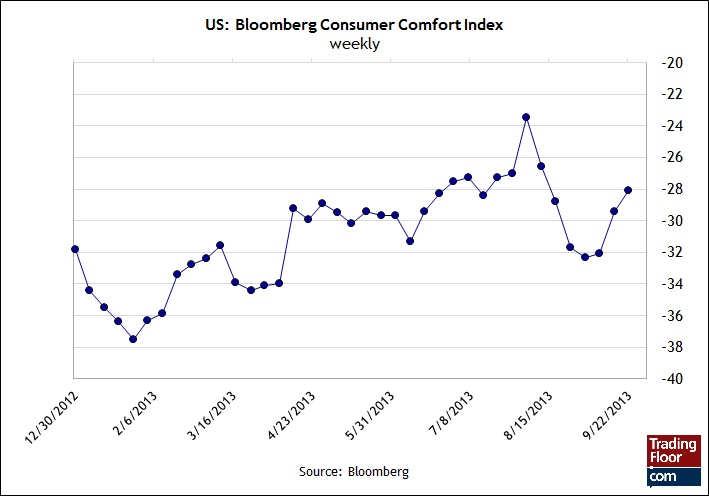

US Bloomberg Consumer Comfort (13:45 GMT): With anxiety on the rise about the macro implications of the government shutdown, today’s weekly release on the state of consumer confidence via Bloomberg's estimates will be of greater import than usual. The longer the budget war in Congress runs, the greater the market’s search for guidance on how the political stalemate is affecting perceptions on Main Street.

According to this Bloomberg index, the mood has been recovering recently after an August setback. But with the arrival of the fiscal logjam in Washington this week, investors will be watching today’s number for any sign that consumers are having second thoughts on thinking positively. It wouldn’t be surprising to learn that pessimism is on the rise again. Indeed, there’s a real cost to the shuttering of the federal government. According to an estimate from IHS Global Insight, the price tag for the shutdown is USD 300 million a day (or USD 12.5 million an hour). Today’s weekly update will reveal if there’s also a price to pay in consumer expectations.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

3 Numbers To Watch: EU Retail Sales, US Jobs & Consumer Comfort

Published 10/03/2013, 06:56 AM

Updated 03/19/2019, 04:00 AM

3 Numbers To Watch: EU Retail Sales, US Jobs & Consumer Comfort

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.