On Monday we received an excellent piece from the China analyst who outshines all others we read -- Jonathan Anderson of Emerging Advisors Group.

Mr. Anderson points out very succinctly why the relentless news coverage of “capital flight” from China is fundamentally mistaken, and why the litany of negative coverage of the Chinese economy is often based on simple misinformation and misunderstanding of economics and finance.

The Reality of Capital Outflows

Coverage of China’s financial system in the popular press usually refers to “money fleeing China” -- with the implication being that all the phenomena being described are similar to the rush of corrupt officials to get their ill-gotten gains out of the country before they get caught up in President Xi Jinping’s anti-corruption net. But that implication is profoundly inaccurate.

As we have told readers before, these “capital outflows” have nothing to do with money leaving China. What they represent is Chinese people selling yuan and buying dollars -- they say nothing about where those dollars are held.

Anderson provides the following chart to illustrate the process, showing changes in foreign exchange reserves held by the People’s Bank of China and by the commercial Chinese banking system: here are risks in such a lack of transparency. But there are obviously also benefits, or market participants wouldn’t use dark pools. They’re growing in significance, now accounting for about 40 percent of all trading activity. What’s the attraction?

Source: Emerging Advisors Group

In 2015, he points out, the PBOC sold 250 billion in U.S. dollars… and commercial banks accumulated 250 billion U.S. dollars. Chinese people bought dollars, and then deposited those dollars in Chinese banks. Even accounting for other flows, he estimates 60 percent of implied “outflows” remained in the country.

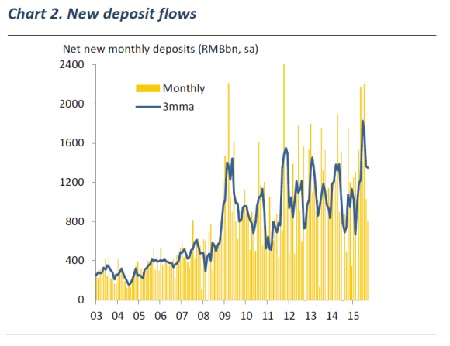

The following chart seals the deal:

Aggregate deposit growth increased over the summer, during all the talk of “capital flight.”

Selling yuan and buying dollars is very different from taking your cash out of the country. For us this is yet another data point that market participants’ still-palpable fear of a China-borne “global financial pathogen” is not based on reality.

Investment implications: Despite reporting in the mainstream financial press, money is not “fleeing China” -- it is remaining in China, but as dollars rather than yuan. Investors should bear this fact in mind as they shape their view of the world -- especially when the press seems eager to paint a view of the Chinese economy that may be more negative than the data warrant.