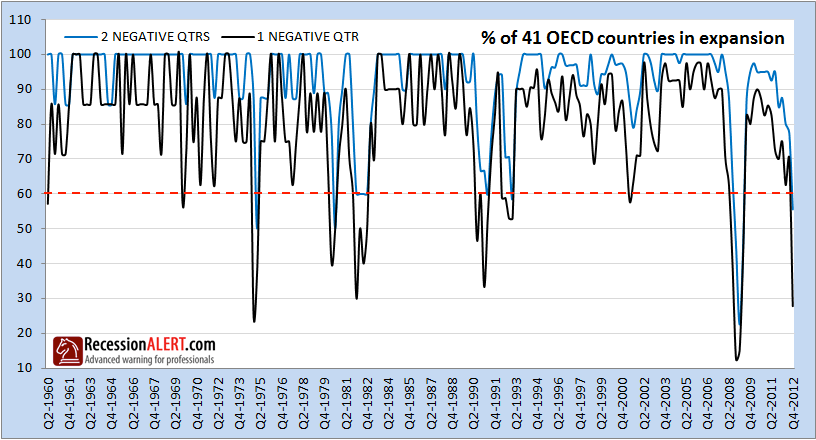

With the disappointing initial GDP releases for Q4 2012 from Europe just out, the “world” as defined by 41 OECD countries across the globe has plunged into recession. We define “recession” through two alternative definitions for our comparison: either the presence of a single negative quarter-on-quarter growth or the more traditional two consecutive negative quarterly growths. Whichever way you look at it, the number of countries in expansion plunged dramatically between Q3 2013 and Q4 2012 as shown below:

Now this is a diffusion index, with each country receiving equal weighting, and so it appears that 60% seems to be a viable threshold for the definition of “global recession” using the single-quarter definition (black) as 70% is probably the appropriate threshold for the second-quarter definition (blue).

Countries in “recession” for the 18 countries we have data for so far in Q4 are:

- Austria

- Belgium*

- Czech Republic*

- France, Germany

- Hungary*

- Italy*

- Japan*

- Netherlands*

- Portugal*

- Spain*

- Greece*

- U.S

- UK.

A Few Caveats

We should add that Q4 2012 GDP figures are preliminary releases, subject to revisions -- we expect the U.S. to revise upward -- and we only have data for 18 countries for the fourth quarter so far, and a heavy sprinkling of EU-based entities to boot, which could be skewing the numbers to the downside. As the figures roll in during the course of the month/s we will update clients accordingly.

It's clear the U.S is faring far better than most, but one has to question how long she can remain above water with the drag of her economic peers weighing upon her economy. While most long-leading indicators for the U.S. are pointing strongly up, the co-incident U.S. data is on the brink. We will be watching the two co-incident stalwarts --the NBER Recession Model and the GDP/GDI Recession Models -- very closely indeed.