US midterms

A mid-cycle election in the United States on Tuesday will serve as an appetizer ahead of Thursday’s critical inflation report. This election won’t be a game-changer for financial markets grappling with inflation and recession threats, but it could spark some relief moves in the dollar and stocks.

In a nutshell, the Democrats are likely to lose control of Congress. The party currently holds a slim majority in the House of Representatives, while the Senate is split 50-50, with Vice President Harris’s tiebreaker vote giving the Democrats control of this chamber too.

Opinion polls and betting markets suggest the Republicans will take back the House, with prediction websites putting the probability of this outcome around 85%. The Senate race is too close to call, with both opinion surveys and bookmakers viewing it essentially as a coin toss.

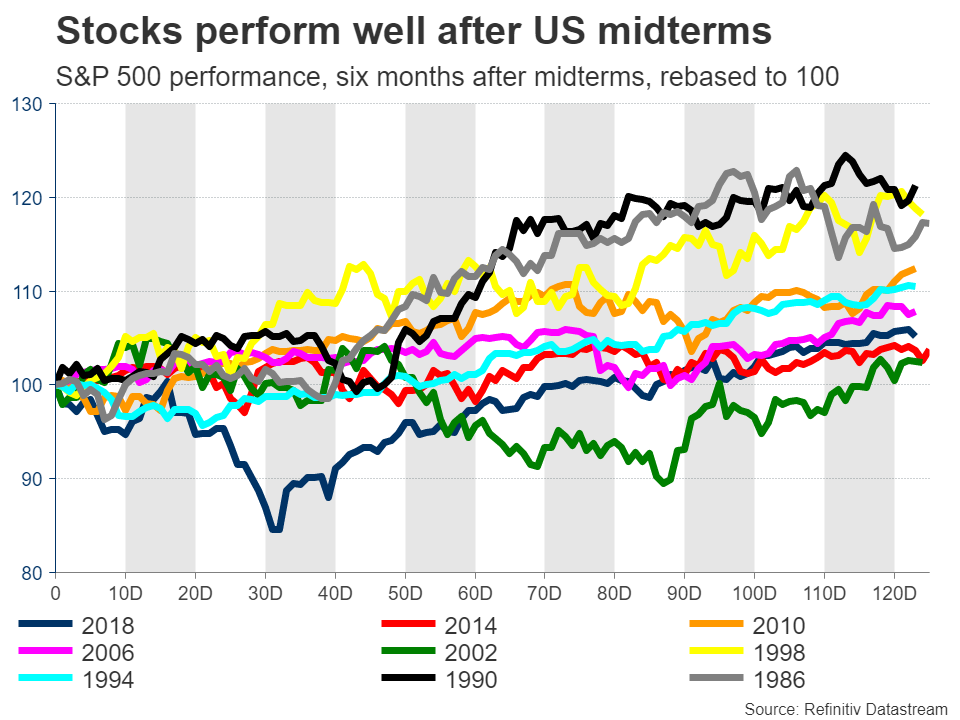

Historically speaking, a divided Congress tends to benefit stock markets since it limits the scope for passing anti-business legislation, such as tighter regulations or higher corporate taxes. Over the last seven decades, stocks have always been higher six months after a midterm election.

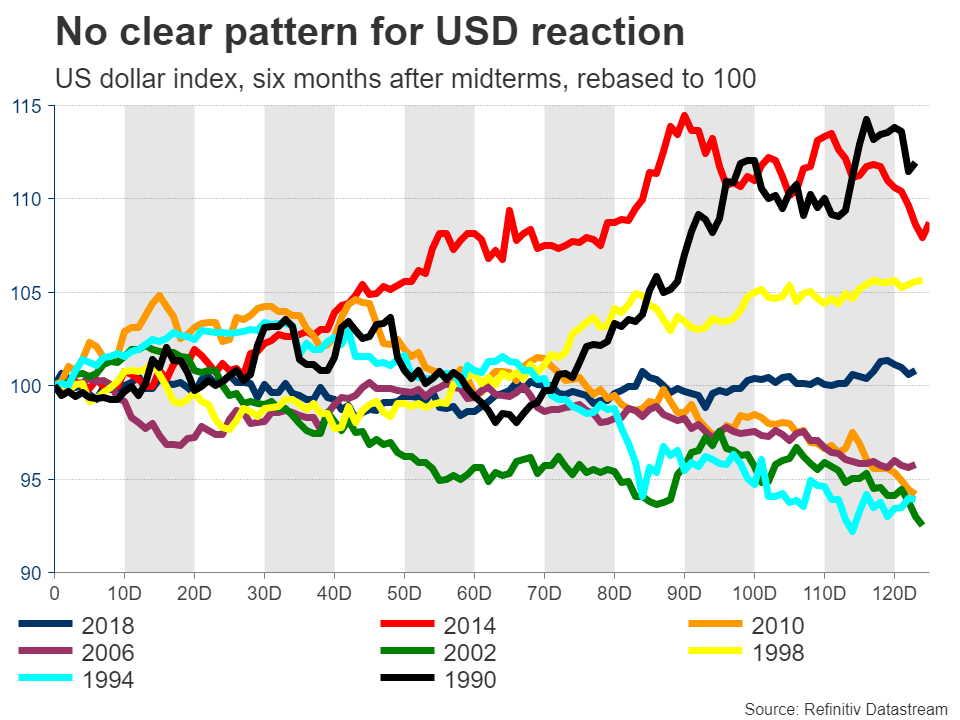

In the FX arena, there’s no clear historic pattern, so the market reaction might boil down to how the election affects the trajectory of Fed policy. In this sense, a split Congress would limit the government’s ability to roll out new spending, which argues for slower growth and softer inflation.

This could spark a pullback in the dollar as traders second-guess whether rates will truly reach the 5.2% peak that’s currently baked into the cake. To be clear though, these reactions are likely to be minor. A divided Congress is already the market’s baseline scenario - it wouldn’t be any surprise.

Similar to 2020, investors might need to wait a few days before the election results are finalized, as ballots that were sent by mail are counted.

US inflation winding down?

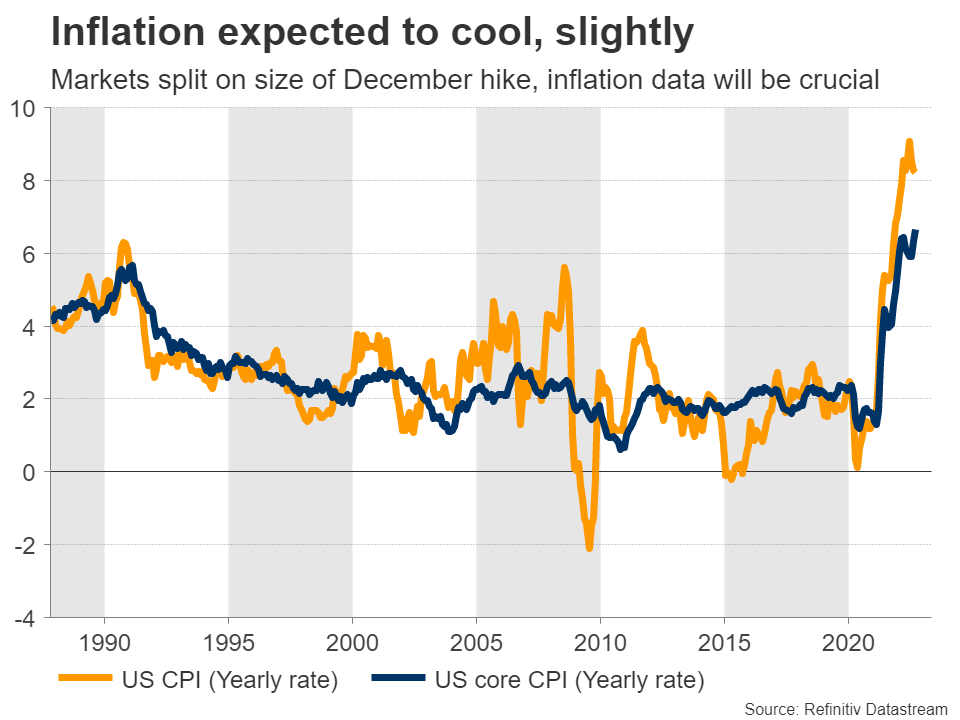

In the battle against inflation, the Fed might finally receive some good news. Forecasts suggest that both the headline and core CPI rates retreated in October, albeit only slightly.

Most of the expected cooldown in price pressures is linked to the decline in transportation and fuel costs. The uncertainty revolves around the bigger and ‘stickier’ categories, such as rents and medical care, which combined account for roughly 40% of the entire CPI basket.

Traders are currently split on how much the Fed will raise rates next month. Market pricing is currently leaning towards another 75 basis point hike, but it’s a close call with investors also assigning decent chances to a smaller 50bps move. This inflation report will inevitably tip the scales in one direction, driving the US dollar accordingly.

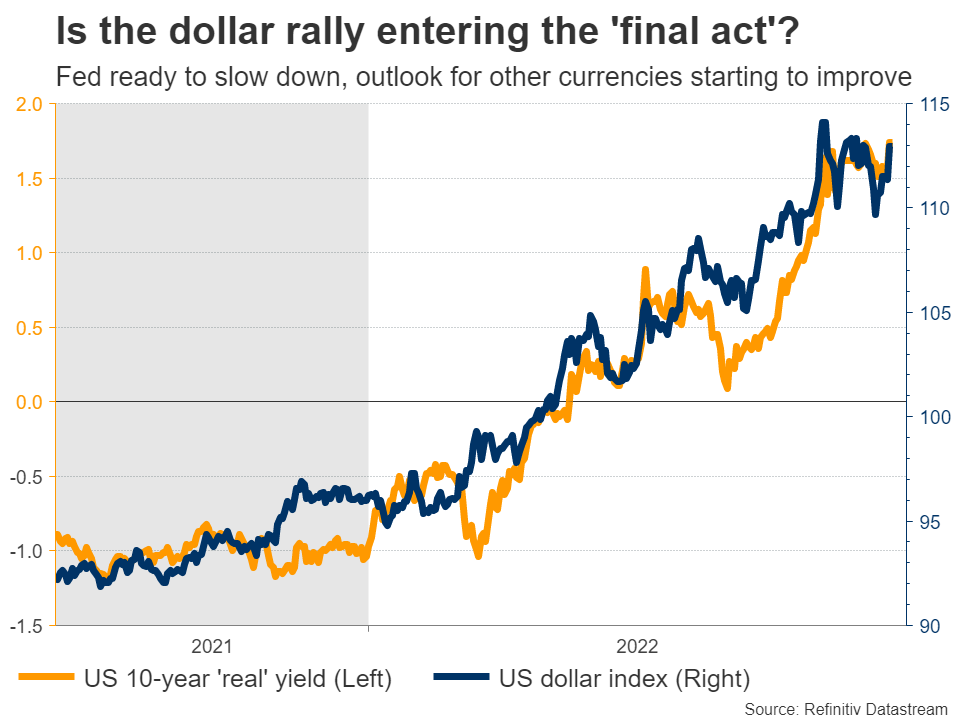

Overall, the outlook for the dollar remains positive, but we might be entering the ‘final act’ of this stunning rally. The Fed has opened the door for smaller rate increases moving forward, the market is already flush with long-dollar bets, and the fundamentals of other major currencies have finally started to improve.

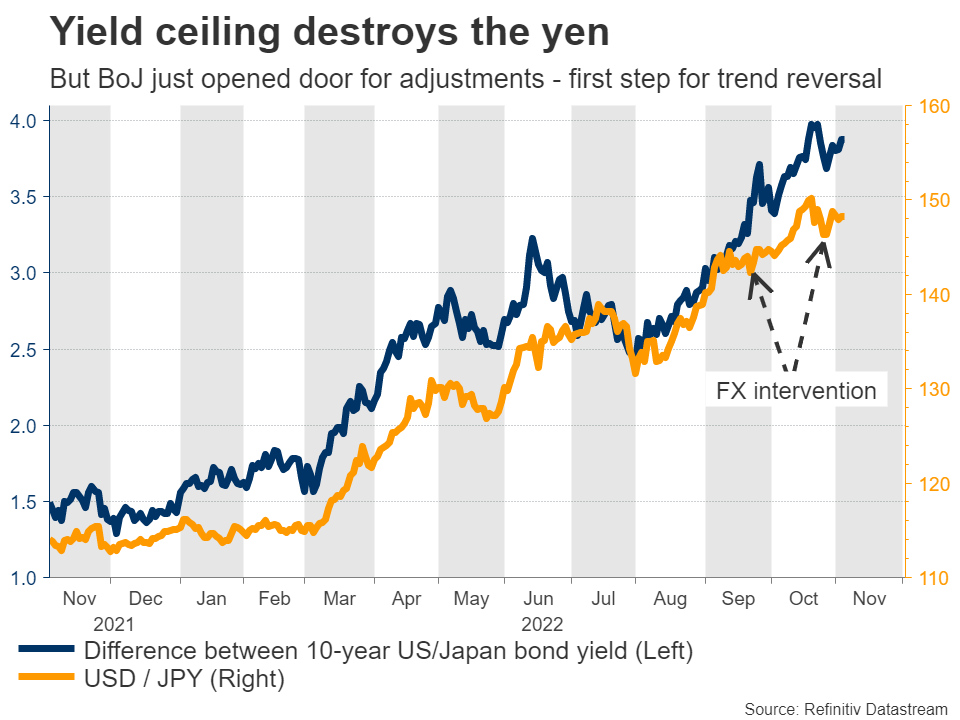

In Europe, the recent decline in energy prices suggests that any winter recession might not be brutal after all. In the UK, the budget crisis is now in the rear-view mirror, while the Bank of Japan chief just signaled he is willing to adjust the yield ceiling that has devastated the yen.

It’s still too early to call for a proper trend reversal, and the dollar could hit new highs in case the global outlook continues to deteriorate, but the scope for further gains seems limited from here. The risk-to-reward profile of chasing further dollar strength just doesn’t seem attractive at this stage.

Japanese and British releases

The biggest piece of news that flew under the radar this week was a shift in tone by the Bank of Japan. Governor Kuroda said his central bank could make its yield curve control strategy “more flexible” in the future, setting the stage for an eventual normalization of policy.

Yield curve control is a policy that essentially caps longer-dated Japanese rates. Since Japanese yields cannot rise beyond a certain level, interest rate differentials automatically widen against the yen as foreign central banks raise rates.

Adjusting this strategy would be the first step towards a trend reversal in the yen. Such a shift would likely require an acceleration in wage growth, which isn’t evident yet. Nevertheless, the wind of change is blowing, and investors will keep an eye on the BoJ’s summary of opinions on Tuesday for more clues on this subject.

Finally, UK economic growth data for the third quarter will be released Friday. Sterling took a serious beating this week, after the Bank of England pushed back against market pricing for aggressive rate increases and reaffirmed its forecasts for a prolonged recession next year.

With interest rate expectations having adjusted to reality and the political scene stabilizing, global risk sentiment could reestablish itself as the main driver for the pound moving forward.