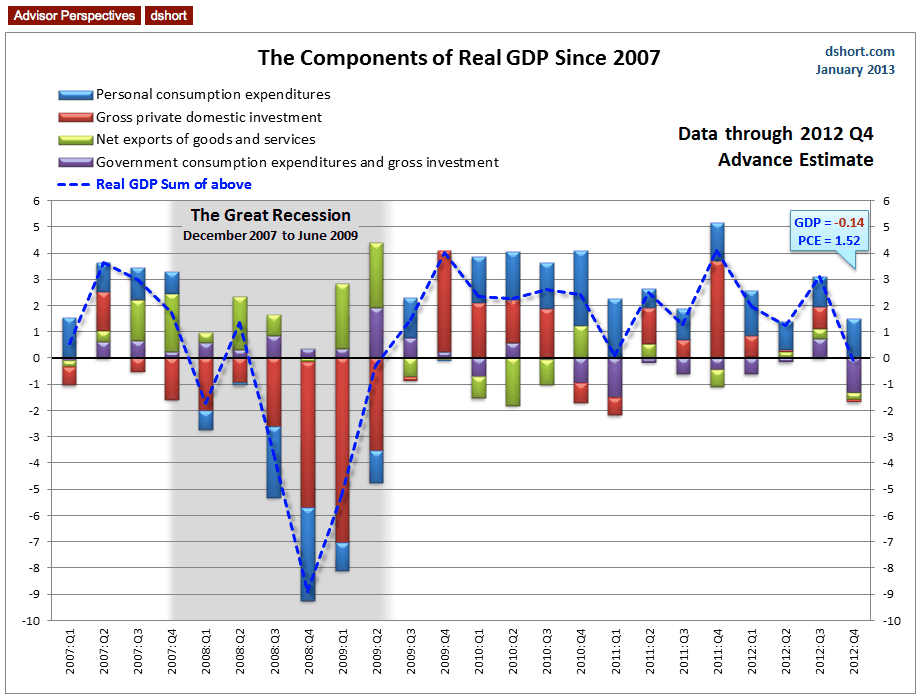

The chart below is my way to visualize real GDP change since 2007. I've used a stacked column chart to segment the four major components of GDP with a dashed line overlay to show the sum of the four, which is real GDP itself. The major changes that contributed to today's minus 0.1% Advance Estimate from the 3.1% Q3 were primarily seen in the general decline in private inventories, a sharp decline in exported goods, and a substantial drop in national defense spending.

My data source for this chart is the Excel file accompanying the BEA's latest GDP news release (see the links in the right column). Specifically, I used Table 2: Contributions to Percent Change in Real Gross Domestic Product.

Over the time frame of this chart, the Personal Consumption Expenditures (PCE) component has shown the most consistent correlation with real GDP itself. When PCE has been positive, GDP has been positive, and vice versa. In the latest GDP data, the contribution of PCE came at 1.52 of the -0.1 real GDP. This is an increase from the 1.12 PCE of the 3.1 GDP in the Third Estimate for Q3.

Note: The conventional practice is to round GDP to one decimal place, the latest at -0.1. The -0.14 GDP in the chart above is the real GDP calculated to two decimal places based on the BEA chained 2005 dollar data series.

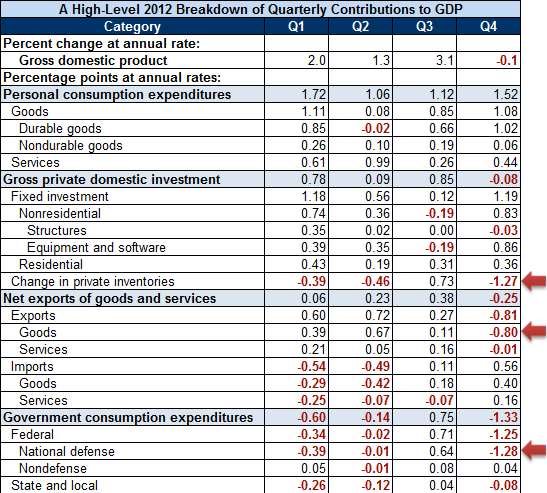

Here is a more detailed look at the contribution changes across the four quarters of 2012.

As for the negative 1.27 contribution from private inventories, let's look at this component over the last twelve quarters. It is highly volatile and, in my view, not very useful in forecasting GDP trends:![]()

The decline in defense spending, no doubt a disturbing development for militant conservatives, was not surprising given the war drawdown. This trend will likely continue with the probable beginning of sequestration in Q1.

The falloff in goods exports (a minus 0.80 contribution) is a definite anomaly resulting primarily from the drought in the US. It is the first negative contribution of goods exports since the end of the last recession.

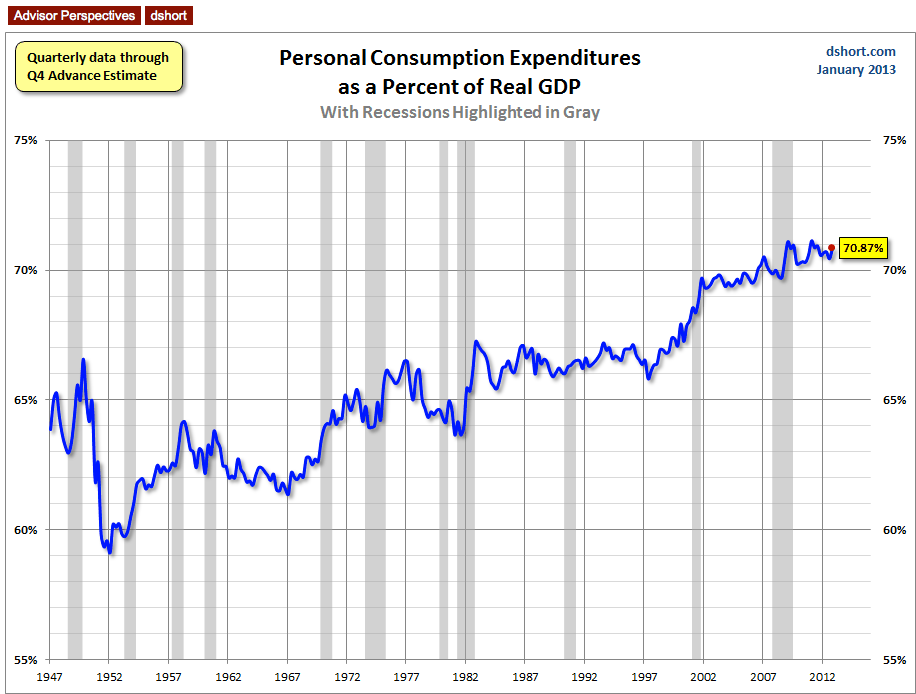

As for the role of Personal Consumption Expenditures (PCE) in GDP and how it has increased over time, here is a snapshot of the PCE-to-GDP ratio since the inception of quarterly GDP in 1947. The Q4 2012 ratio is 70.87%, fractionally off the all-time high of 71.15% in Q1 2011 but fractionally higher than last quarter's 70.46%. From a theoretical perspective, there is a point at which personal consumption as a percent of GDP can't really go any higher. At the low 70 percents, we may be approaching that level.

The one caution I have regarding today's strong 1.52% contribution of PCE to GDP is the likelihood that tax planning strategies to avoid the expected 2013 tax hike were a key factor in the end-of-year spending increase. Q1 2013 will probably show the opposite effect, a phenomenon I've highlighted before in my graphs of personal income.

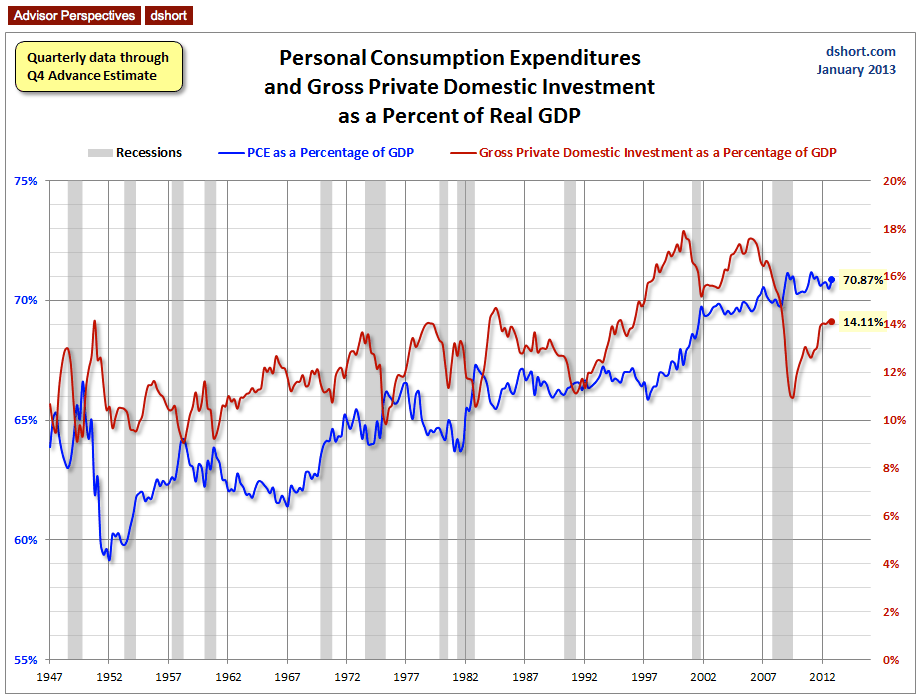

Let's close with a look at the inverse behavior of PCE and Gross Private Investment (GPDI) during recessions (note my use of different vertical scales to facilitate the overlay). PCE generally increases as a percent of GDP whereas Private Investment declines. That is not what we're seeing in the current data. I've plotted the two with different vertical axes (PCE on left, GPDI on the right) to highlight the frequent inverse correlation.

Final Thoughts

The recession crowd, with ECRI as their cheerleader, will no doubt view the Advance Q4 GDP estimate as a "see, I told you so" moment. But a few minutes studying the underlying components shows minimal evidence to support the recession forecast. Of course we have a couple more Q4 GDP revisions before we get the first look at Q1 2013 GDP, in late April. The key question is the impact of the expiration of the 2% FICA holiday on households, which could have a significant impact on the key component of GDP, Personal Consumption Expenditures.

I'll update these charts when the Q4 Second Estimate is released next month.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Visualizing GDP: Anomalies In The Q4 Advance

Published 01/30/2013, 12:43 PM

Updated 07/09/2023, 06:31 AM

Visualizing GDP: Anomalies In The Q4 Advance

Note from dshort: The charts in this commentary have been updated to include the Q4 2012 Advance Estimate.

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.