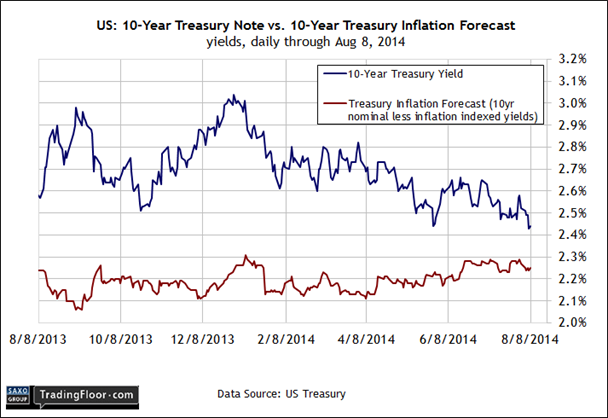

There are no economic releases of substance scheduled today for the US or Europe, which leaves a large gap between demand for new macro insight and the existing supply. Geopolitical risk was on the march last week and demand has increased for liquidity and safety. The revival in the risk-off trade has pushed the yield on the 10-year Treasury close to a 13-month low.

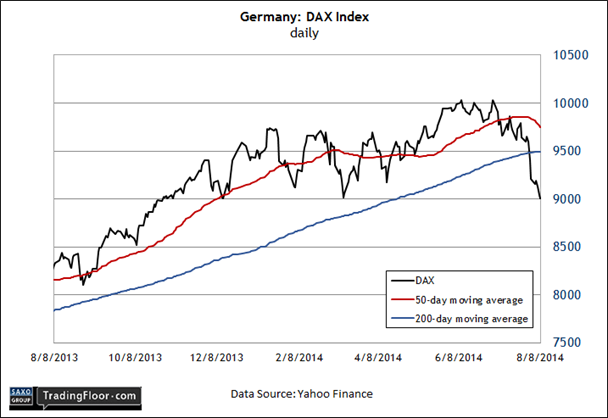

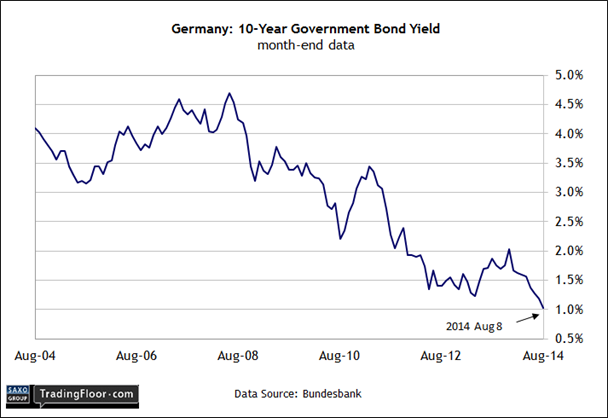

Germany’s 10-year government bond yield also declined, settling last week at just over one percent, which is near a record low. Both rates will be of keen interest today, particularly in the absence of economic releases. Stock markets around the world will also be crucial proxies for evaluating the crowd’s risk tolerance as the week kicks off. With that in mind, early trading in Germany’s DAX Index today will provide the first major clue on sentiment from Europe’s perspective.

US: 10-year Treasury Yield The resumption of US military activity in Iraq late last week was part of a mix of events that shifted the overall tone in markets to a risk-off bias. The canary in this coal mine is the benchmark 10-year Treasury yield, which briefly traded under 2.40 percent on Friday for the first time since June 2013 before settling at 2.44 percent at the close for the week.

The decline in yield is striking because it contrasts with the generally upbeat macro trend for the US economy, including last week’s news that the four-week average of initial jobless claims dropped to an eight-year low. If the Treasury market reflected economic data exclusively, yields would almost certainly be higher, perhaps much higher. Indeed, the data for a range of indicators look encouraging – considerably better, in fact, compared with the numbers earlier in the year, when the harsh winter was taking a toll. But the improvement in macro isn’t showing up in the 10-year yield at the moment, which is lower by nearly 60 basis points since the start of the year.

Note too, that the market's inflation outlook remains stable in the low-2 percent range, or roughly in line with the Federal Reserve Bank's target. The fact that the risk of disinflation/deflation appears low is another reason to think the decline in yield lately is a reflection of geopolitical risk rather than worries about the macro trend in the US.

US stocks, on the other hand, seem to be focused on the encouraging fundamentals. The S&P 500, after a rough start, managed to eke out a small gain, advancing 0.3 percent last week. “What is going on here is right now these geopolitical events are kind of limited to these regions and haven't really spread materially to the US or other major markets, but there is the potential for that to happen," Jeff Kravetz, regional investment director at US Bank Wealth Management in Phoenix, told Reuters on Friday. “It kind of defies logic that we've got the stock market rallying today and going into the weekend that we don't have traders making more conservative moves.”

Logical or not, the question is whether geopolitical risk and other factors will continue to weigh on rates. The answer will, of course, align closely with the headlines in the hours and days to come. But for good or ill, the 10-year yield will be on everyone’s short list of indicators to watch this week as the markets sort out what the dangerous summer has in store for the economic trend in the US and elsewhere.

Germany: 10-Year Bond Yield Like its Treasury counterpart, Germany’s 10-year government bond yield slumped last week. What’s different about Germany’s benchmark: 1) yields are significantly lower compared with the US; 2) the current market rate is near a record low; 3) the meagre payout rate reflects a mix of heightened geopolitical risk and bearish sentiment on the economic outlook for the Eurozone.

European Central Bank president Mario Draghi last week advised that plans were underway to roll out a new round of monetary stimulus. “We have intensified preparatory work related to outright purchases in the asset-backed securities market to enhance the functioning of the monetary policy transmission mechanism,” he said. Even so, the ECB left its policy rate unchanged. But he wasn’t shy about outlining the risks that lurk. "The recovery remains weak, fragile and uneven,” Draghi explained. “In recent weeks, the data shows growth momentum is slowing down. It is quite clear that if geopolitical risks materialise, the next two quarters will show lower growth."

Draghi and company may be poised to introduce yet another phase of monetary stimulus, but the market was in no mood to wait. The yield for what is effectively Europe’s market benchmark slipped towards the psychologically potent one-percent mark. Keep a close eye on this yield today (and in the days ahead) for context on how the market is pricing/repricing geopolitical risk. With Monday’s blank slate for new macro data, all eyes will be on market indicators for gauging where the economy goes from here and what to expect for this Thursday’s flash estimate on second-quarter gross domestic product for the Eurozone.

“Geopolitical tensions have been a driver of lower bond yields,” a fixed-income strategist at Nordea Bank in Helsinki explained via Bloomberg. “We’ve also seen more signs that the Eurozone economy is seeing weaker development going forward. No inflation and weaker activity data adds to expectations of a broad-based ECB asset-purchase program. In the near term, bond yields can go lower still.”

Germany: DAX Index In addition to watching government bond yields today, keep an eye on equity markets for monitoring risk tolerance as investors reassess the outlook this week. Companies in Europe’s biggest economy are an obvious place to start. The DAX is especially valuable (and vulnerable) at this point because the index holds a number of companies that are closely linked with Russian energy. As a result, the benchmark will be closely watched for assessing risk vis-à-vis the Ukraine crisis.

A report on Friday that Russia is seeking to de-escalate the crisis offers a glimmer of hope for a calmer week ahead. But the head of the Eurasia Group, a consultancy, warned that the potential for a deeper level of trouble may be lurking. Noting that Russian troops are massing on the border, “I think frankly Russia-Ukraine is tending negative,” Ian Bremmer told CNBC. “There's a greater likelihood of direct Russian intervention now than it has been at any point in this crisis. I would not be faked by this [de-escalation] news now.”

For now, the German equity market seems inclined to embrace Bremmer’s view. The DAX has fallen sharply over the past week and is now trading below its 200-day moving average for the first time in over a year. The selling is partly related to Russia, but there’s an economic factor to consider too. Last week’s news that Italy’s economy unexpectedly contracted in the second quarter, while German factory orders took a surprisingly big dive in June, raised new concerns that the macro trend in Europe was deteriorating.

But the latest business survey data for Germany suggests that Europe’s biggest economy was still expanding at a moderate pace. In fact, the final Markit Germany Composite Output Index for June rose to 55.7 from 54.0 in the previous month, marking a faster rate of growth in private sector output. But in the wake of recent events, is Markit’s survey data suddenly out of date? The search for an answer today begins by monitoring the collective wisdom of the crowd via the DAX.