Ultra Electronics’ results highlighted that despite the current challenging defence environment, the group has a robust position from which to identify and pursue growth. However, with sequestration now a reality, the question is how budget cuts can be implemented and the potential impact that may have on such growth prospects. Importantly, Ultra has several strands of business that will remain largely unaffected by sequestration and we believe the U.S. government will eventually find a solution to allow more targeted cuts to occur, providing protection for strategic priorities. In that case, we believe Ultra’s positioning in areas of preferential spend and its agile business model will allow it to mitigate macro level challenges.

2012 Results Slightly Ahead Of Forecasts

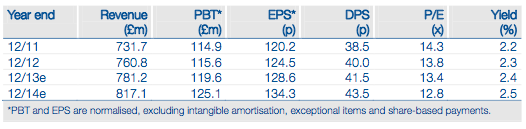

Ultra was able to achieve a solid set of results, with revenue up 4% to £761m, driven by growth in markets outside defence (transport, energy, security and cyber). A 1% currency benefit and the 7% acquisition contribution more than offset a 4% organic decline. Margins were broadly maintained above 16%, despite a step-up in R&D investment, while PBT grew by 1% to £115.6m and EPS was up 4% to 124.5p as a result of lower finance and tax charges. Operating cash flow conversion reduced to 73% as working capital built up during an increased capex phase, while the balance sheet remained strong, with net debt to EBITDA of just 0.32x providing ample headroom for further investment. DPS tracked earnings and was up 4% to 40.0p.

Focus On Sequestration And Non-Defence Markets

With sequestration now a reality, the question turns to how the cuts will be implemented. In our view, the US government will be compelled to act to allow a more targeted reduction to spare priority areas of spend, consistent with the priorities set out in the 21st Century defence document, ie the pivot to Asia, focus on cyber and a drive towards upgradability. Ultra has capabilities in each of these areas and we believe it is therefore as well positioned as any to ride out the coming storm. In addition, non-defence markets account for 44% of revenues and contracts and drivers continue to support an increasing contribution over the near term.

Valuation: Robust Results Point To Value Opportunity

Given the robust results, slightly ahead of our, and consensus, expectations, we feel that Ultra yet again provides a value opportunity. Having rolled forward our valuation onto 2013 forecasts and updated for positive market movements, our sum-of-the- parts fair value increases to 1,803p/share. This equates to a rating of 14.0x CY13 EPS, still at a discount to the 14.9x through-cycle average since flotation, highlighting there is further to go once clarity on the exact nature of sequestration becomes clear.

To Read the Entire Report Please Click on the pdf File Below.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Ultra Electronics: Preliminary Results

Published 03/12/2013, 03:43 PM

Updated 07/09/2023, 06:31 AM

Ultra Electronics: Preliminary Results

Solid Position To Face Sequestration

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.