Including this yesterday’s reports, we now have Q4 results from 356 S&P 500 members that combined account for 80.7% of the index’s total market capitalization. Total earnings for these 356 companies are up +6.5% from the same period last year, with 71.3% beating earnings estimates. Total revenues are up +1.5%, with 55.6% beating top-line estimates.

Comparing the results thus far with what we have been seeing from the same group of companies in other recent quarters in terms of growth rates, beat ratios, and guidance presents a mixed picture.

The charts below show the comparison of the results thus far with what we have seen from this same group of companies in other recent quarters.

We have discussed the Apple Inc (NASDAQ:AAPL) effect in this space before and the effect is very pronounced.

The charts below provide a side-by-side comparison of the Q4 earnings and revenue growth rates for the 356 S&P 500 companies that have reported results, with and without Apple in the numbers (the left side is with Apple and the right side is excluding Apple). The comparisons are with what we have seen from the same group of companies in 2014 Q3 and the average of the preceding four quarters.

We should keep in mind however that Apple isn’t the only ‘unusual’ factor this earnings season. Results from the Finance sector, particularly tough comparisons at Citigroup Inc (NYSE:C) and JPMorgan Chase & Co (NYSE:JPM), have been a drag on the aggregate growth picture. And then we have the whole oil situation, with profitability of the Energy sector companies following what has been happening to oil.

The chart below shows the results thus far excluding the effect of Apple and the Energy sector. As you can see, the earnings growth picture is broadly comparable with historical levels on this basis.

But irrespective of whether we look at the results as a whole or piecemeal, the weakness on the revenue side comes through – revenue growth rate is tracking below other recent quarters whether we look at the results with or without Apple, Finance or Oil.

Another common theme in the reports thus far is the impact of a strong dollar and sharp fall in oil prices. The oil price impact hasn’t been restricted to the Energy sector alone, even companies like Caterpillar Inc (NYSE:CAT) have been affected. Estimates for Q4 had fallen more than normal due to the oil development and we are seeing the trend play out in a big way in estimate revisions for the current and following quarters.

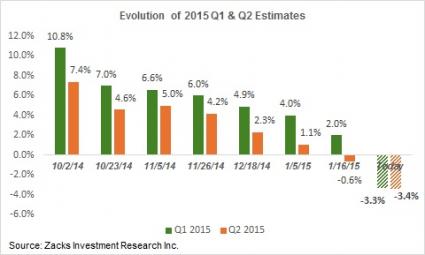

In fact, the magnitude of energy-driven negative revisions for 2015 Q1 and Q2 is so severe that the first half 2015 earnings growth rate for the S&P 500 index as a whole has almost evaporated. The chart below shows what is happening to 2015 Q1 and Q2 earnings estimates for S&P 500 companies.

Energy is obviously the biggest drag on estimates for the first half of the year, but estimates beyond the Energy sector are also coming down. The hope is that over time we will start seeing the savings from lower energy prices show up in other sectors, particularly the retail and discretionary sectors. Those stocks have been showing these favorable expectations, though we have yet to see that show up in estimates.