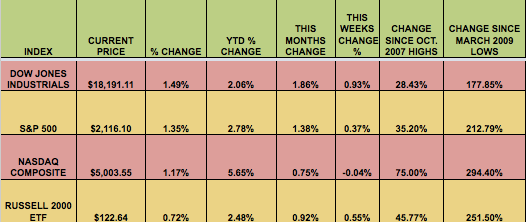

Markets: 3 out of 4 Indexes were up this week, with the Dow leading, as markets bounced back on Friday, after a middle of the road April jobs report eased fears of a June Fed rate hike. Fed chief Yellen spooked markets earlier in the week, with a comment that she thought stocks and bonds were both overvalued.

Earnings beats trended downward over the past days-the peak for Earnings estimates beats came on 4/27, when 66.6% of companies that had reported between 4/8 and 4/27 had beaten EPS estimates. Following a huge batch of misses on 4/28, the beat rate fell to 64.8%, and by the end of this week, the beat rate dropped another 2.3 percentage points down to its current level of 60.3%. (Source: B.I.G.)

Volatility rose as high as 16.86, and fell back down to 12.86 to end the week, up just over 1% again for the week. The US dollar fell vs. most major currencies, except the New Zealand dollar:

Market Breadth: This week, 24 out of 30 DOW stocks rose, vs. 13 last week. 59% of the S&P 500 rose, vs. 40% last week.

US Economic News: Non-Farm Payrolls rose considerably in April, to 223K, but March’s 126K figure was revised downward, to 85K. Job gains occurred in professional and business services, health care, and construction. Mining employment continued to decline.

The unemployment rate dropped to a near seven-year low of 5.4%, while average hourly earnings rose three cents in April, a year-on-year gain of 2.2%.

Unemployment Claims’ 4-week avg. continues to hover around 15 year-lows.

Week Ahead Highlights: Reuters reports that “Labor expenses will be a key focus during retailers’ earnings conference calls in the coming weeks, with many companies under pressure to boost workers’ wages at a time when low U.S. unemployment levels have given workers more leverage”. Macy`s Inc (NYSE:M), Nordstrom (NYSE:JWN), and Kohl`s Corporation (NYSE:KSS) will all report next week.

Next Week’s US Economic Reports:

Sectors & Commodities:

Financials led this week:

Commodity Futures: