The Sherwin-Williams Company's (NYSE:SHW) shares have shot up 37.7% over the past six months. The company has also outperformed its industry’s rise of 36.7% to over the same time frame. The stock is also up 14% over the past three months.

Sherwin-Williams, a Zacks Rank #3 (Hold) stock, has a market cap of roughly $55 billion and average volume of shares traded in the last three months is around 475.6.7K. The company has an expected long-term earnings per share growth of 11.9%.

Let’s take a look into the factors that are driving this paints and coatings giant.

What’s Going in SHW’s Favor?

Forecast-topping earnings performance in the third quarter and upbeat prospects have contributed to the rally in Sherwin-Williams' shares.

Sherwin-Williams’ adjusted earnings of $6.65 per share for the third quarter topped the Zacks Consensus Estimate of $6.46. Its revenues rose around 3% year over year to $4,867.7 million and beat the Zacks Consensus Estimate of $4,819.8 million. The company gained from sustained strength in architectural paint markets in North America.

Sales in the quarter were driven by increased paint sales volume in North American stores and higher selling prices that more than offset weak demand across certain end-markets outside the United States.

The company also raised its adjusted earnings per share guidance for 2019 to the range of $20.90-$21.30. For the full year, Sherwin-Williams expects low single digit percentage increase in net sales from 2018.

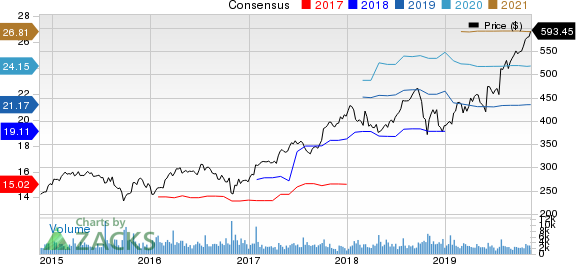

Earnings estimates for Sherwin-Williams for 2019 have moved up over the past month. Over this period, the Zacks Consensus Estimate for 2019 has increased by 0.3% to $21.17. The Zacks Consensus Estimate for earnings for 2019 reflects an expected year-over-year growth of 14.3%.

The company is witnessing favorable demand in its domestic end-use markets and remains committed to expand its retail operations. It is focused on capturing a larger share of its end-markets, as reflected by an increasing number of retail stores. The company added 31 net new stores in the first nine months of 2019. Plans are in place to add around 80-100 net new stores in North America by the end of 2019.

Sherwin-Williams’ cost control initiatives, working capital reductions, supply chain optimization and productivity improvement are also yielding margin benefits. Working capital management and efforts to cut operating costs are also helping the company to generate strong cash flows. The company is also taking appropriate pricing actions, which is lending support to its margins.

The company is also gaining from synergies of the Valspar acquisition. It expects to achieve total annual run rate synergies of around $415 million at the end of 2019.

The Sherwin-Williams Company Price and Consensus

The Sherwin-Williams Company price-consensus-chart | The Sherwin-Williams Company Quote

Stocks Worth a Look

A few better-ranked stocks in the construction space include Orion Group Holdings, Inc. (NYSE:ORN) , North American Construction Group Ltd. (TSX:NOA) and MasTec, Inc. (NYSE:MTZ) .

Orion Group Holdings has an expected earnings growth rate of 54.1% for the current year and sports a Zacks Rank #1 (Strong Buy). The company’s shares have gained around 21% over the past year. You can see the complete list of today’s Zacks #1 Rank stocks here.

North American Construction has an expected earnings growth rate of 238.1% for the current year and carries a Zacks Rank #2 (Buy). Its shares have gained roughly 15% in the past year.

MasTec has an expected earnings growth rate of 36.1% for the current year and carries a Zacks Rank #2. Its shares have surged around 53% in the past year.

Free: Zacks’ Single Best Stock Set to Double

Today you are invited to download our just-released Special Report that reveals 5 stocks with the most potential to gain +100% or more in 2020. From those 5, Zacks Director of Research, Sheraz Mian hand-picks one to have the most explosive upside of all.

This pioneering tech ticker had soared to all-time highs and then subsided to a price that is irresistible. Now a pending acquisition could super-charge the company’s drive past competitors in the development of true Artificial Intelligence. The earlier you get in to this stock, the greater your potential gain.

Download Free Report Now >>

MasTec, Inc. (MTZ): Free Stock Analysis Report

Orion Group Holdings, Inc. (ORN): Free Stock Analysis Report

North American Construction Group Ltd. (NOA): Free Stock Analysis Report

The Sherwin-Williams Company (SHW): Free Stock Analysis Report

Original post

Zacks Investment Research