- Strong US retail sales and softer inflation expectations lift Wall Street

- Dollar knocked off highs as 100-bps Fed rate hike bets pared back

- Euro tries to distance itself from parity but Italy and gas supply risks cap gains

- WTI oil tests $100 on summer demand after Biden’s Saudi trip bears no fruit

Stocks set for positive start to week

Equity markets got off to a buoyant start on Monday as recession panic continued to subside following some encouraging data out of the United States on Friday. Retail sales jumped by 1.0% m/m in June, easing concerns that rising borrowing costs and soaring prices would squeeze spending. But more significantly for investors, signs that consumer inflation expectations are levelling off dealt a further blow to bets that the Federal Reserve would hike interest rates by one percentage point in just over a weeks’ time.

Both one- and five-year inflation expectations in the University of Michigan’s consumer sentiment survey dipped slightly in July, while consumer confidence recovered from record lows. The data came hot on the heels of another stronger-than-expected CPI reading for June, which doesn’t appear to have alarmed Fed officials, who suggested that a 75-bps increase was still their base case in remarks made just before the blackout period began.

The S&P 500 rallied by 1.9% on Friday and the Nasdaq Composite by 1.8%. E-mini futures were indicating gains of around 1% as European trading got underway. The Euro Stoxx 50 index climbed to a 2½-week high and Asian bourses closed in positive territory too, boosted by more pledges of economic support by China’s central bank.

The earnings season is expected to heat up this week, with Bank of America (NYSE:BAC) and Goldman Sachs (NYSE:GS) being the next major US banks to report today following very mixed numbers from their rivals last week. The two will announce their results before the market open and IBM (NYSE:IBM) will report its results after the closing bell.

Oil extends rebound as market tightens further

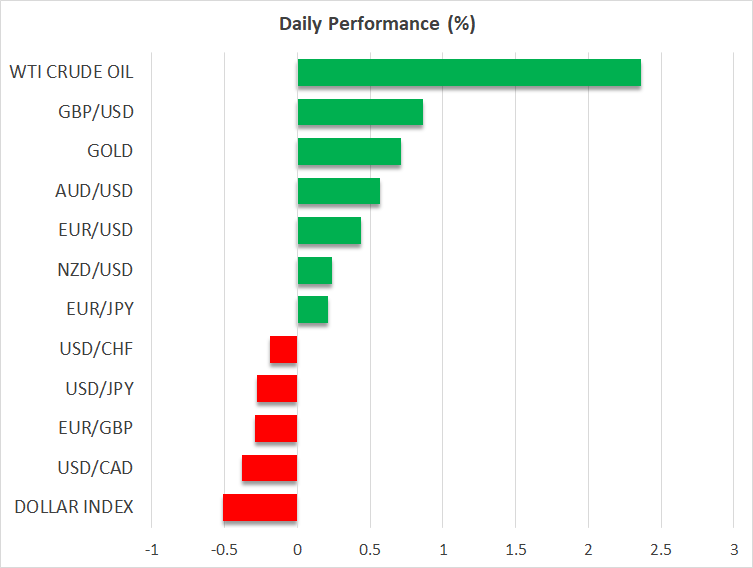

The improved risk appetite also boosted commodities, though it’s too early to say whether the month-long downtrend across all the commodity classes is over. Oil prices were last up more than 2.5% as strong summer demand is offsetting worries about the deteriorating growth outlook.

Heatwaves in America, Europe and China are driving demand for electricity to record levels even as oil supply is expected to remain tight.

US President Joe Biden failed to secure higher output from OPEC’s biggest oil producer, Saudi Arabia, on his trip to the country over the weekend. Although there is some possibility that Saudi Arabia will push for higher production quotas when OPEC meets in August, that prospect looks slim for now and WTI futures are back above $100 a barrel today.

Euro in anxious wait for Nord Stream 1 reopening

European gas futures were rising too on Monday, though they remained off their recent highs. There is a lot of nervousness about the reopening of the Nord Stream 1 pipeline, which is currently undergoing maintenance – due to be completed on July 21. The pipeline is Germany’s main source of Russian gas and there are fears that if Russia were to decide to cut off supplies indefinitely, it would force power rationing, potentially crippling German industries.

Even if the Russians aren’t planning on cutting off the taps just yet but the maintenance overruns by several days or more because it’s taking longer to carry out the repairs, there is a risk that markets could overreact.

This is keeping the euro on edge and limiting the advances as it recovers above the $1.01 level today. But the energy crunch isn’t the euro’s only woes as Italy is facing a fresh political crisis after the breakup of the coalition government. Prime Minister Mario Draghi has to decide by Wednesday whether to resign, triggering a snap election, or to try and put together a new coalition.

Moreover, the European Central Bank is widely anticipated to kick off a series of rate hikes on Thursday to contain surging inflation just as economic growth is stalling.

Pound shines as dollar pulls back

Meanwhile, in the UK, Conservative MPs will vote in the third round on Monday to narrow down the list of candidates vying to take over Boris Johnson as party leader and prime minister. With former finance minister Rishi Sunak still the favourite to win the leadership race after the weekend’s televised debates, sterling isn’t feeling much pressure and is the best performer so far in the day, surging past the $1.19 level.

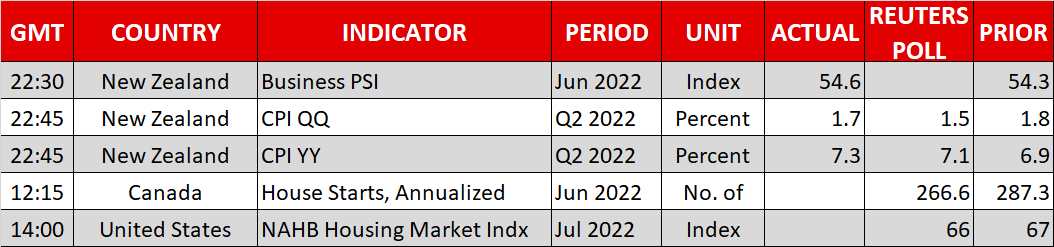

The New Zealand dollar, however, eased back from earlier highs when it briefly touched $0.62 on the back of hotter-than-expected CPI figures for the second quarter.

As for the US dollar, it is broadly weaker, even against the Japanese yen, and its index against a basket of currencies is trading about 0.5% lower.