Macro- and flow-oriented arguments are expected to push EUR/SEK higher in December. The cyclical outlook has deteriorated sharply. The Riksbank is likely to make a U-turn on 20 December by delivering a 25 basis points cut – a bigger cut cannot be ruled out. December is also accompanied by recurrent flow stories. New Swedish pension money (PPM) is disbursed on 13 December. We estimate SEK10bn to SEK15bn will hit the Swedish krona with temporary headwinds for the krona ahead of that date. Hence, EUR/SEK is expected to edge higher near-term. However, the cyclical slowdown (SEK negative) is balanced by better fundamentals (SEK positive), which together with a further exclusive euro sell-off could take the krona back into overvalued territory in relation to the euro – below 9.00 during 2012.

Cyclical outlook deteriorates - the Riksbank makes a U-turn

The strong uptrend in EUR/SEK in November did not only push EUR/SEK towards 9.30 but also RSI into overbought territory. As such the GDP figure, which on the headline was much stronger than projected but in the details was less rosy, could have been a good excuse to sell the pair, take profit. The uptrend has been seriously challenged and a 50% retracement of the November rally would take EUR/SEK to 9.15. That said we see macro- and market-oriented arguments pushing the pair higher yet again in December.

Our short-term model has pulled the spot rate gradually higher and with fair value around 9.30 the weakening of the krona is fully justified. The Riksbank has been re-priced for more aggressive rate cuts and the euro crisis has dented risk appetite, sending stock markets lower and leaving the VIX index at somewhat elevated levels. Since we: 1) sincerely doubt that there will be a near-term resolution to the crisis and since we still lack a circuit breaker for the low/no confidence environment and since we 2) fully buy in to the view that the Riksbank will embark on an easing cycle in December, we prefer to buying EUR/SEK on dips.

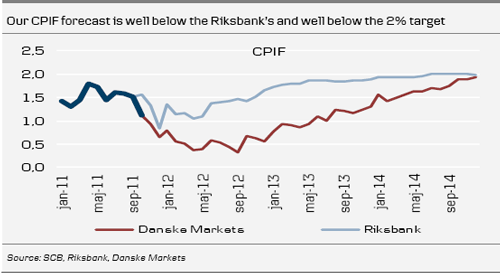

The cyclical outlook in Sweden and abroad has deteriorated further. Sweden, a highly export-dependent economy, will be hit hard by sharp global slowdown. We have recently cut our GDP forecast and expect negative growth in 2012. The fourth quarter may actually be the first quarter in a series printing negative consecutive growth. In fact the stronger-than-expected Q3 reading even raised the risk for negative growth in Q4, since the positive surprise was due to involuntary build up of inventories, something that is likely to be reversed in Q4 with heavy sales, not least in the retail sector, pushing inflation even lower. We project CPIF inflation (excluding mortgages) of below 1% during most of 2012 and even as low as 0.5%. It’s not hard to find downside risks to this forecast.

Swedish monetary policy is expected to make a U-turn on 20 December by delivering a 25bp cut, much in line with market pricing. If the ECB slashes rates again next week, 50bp from the Riksbank cannot be ruled out (acknowledging that the GDP figure could be viewed as a counter argument). If it unexpectedly cuts 50bp, EUR/SEK will surely spike significantly higher as neither the money nor the foreign exchange market would be prepared. We believe the Riksbank will follow up with a series of rate cuts in 2012 taking the repo rate to 0.5% by H2 12, which is marginally lower than the market is currently pricing in. Relative yields might not be a very strong argument for a weaker krona, since both the Riksbank and the ECB are expected to cut more than is priced in. But with lower Swedish rates the rate advantage disappears which could reverse previous carry-related krona demand.

PPM flows: Buy the rumour sell the fact

December is also accompanied by recurrent flow stories. New Swedish pension money is disbursed on 13 December. The Swedish Pension Agency (PPM) just reported that the total amount this year is SEK32.1bn, which is slightly (about SEK2bn) more than in the previous two years. We estimate that SEK10bn to SEK15bn will hit the Swedish krona. On the one hand, appetite for global equities may be dampened due to the debt crisis (less krona outflows than previous years), but on the other hand, the stronger krona exchange rate compared with last year may render smaller hedge ratios on any given foreign investment (more krona outflows).

We draw the following conclusions:

Conclusion

The technical picture is less clear-cut following the late correction, and we could see EUR/SEK completing its 50% retracement of the November rally before it’s ready to test 9.30 again and potentially challenge the 9.3950 peak. From a macro/flow perspective we are bullish about EUR/SEK going into the final month of the year as political uncertainty weighs on sentiment, PPM and as the Riksbank embarks an easing cycle on 20 December.

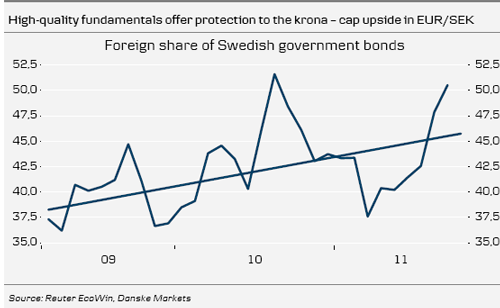

That said we don’t expect EUR/SEK to explode on the upside as it did in 2008/09. The upside is capped by strong fundamentals, savings surplus, low public debt, low default risk (CDSs), stable AAA rating and low valuation. Foreign demand for Swedish quality is intact, as illustrated in foreign holdings of Swedish government bonds, now more than 50%. In addition, we expect a rebound in appetite for riskier assets later on, which combined with fundamentals and valuation should lend medium-term support to the krona. Unlike 2008 the Swedish exporters are not over-hedged, which limits the downside in the krona this time around.

There is still a good chance that these factors and a further exclusive euro sell off, will take the krona back into overvalued territory vs the euro – that is below 9.00 during 2012.

Cyclical outlook deteriorates - the Riksbank makes a U-turn

The strong uptrend in EUR/SEK in November did not only push EUR/SEK towards 9.30 but also RSI into overbought territory. As such the GDP figure, which on the headline was much stronger than projected but in the details was less rosy, could have been a good excuse to sell the pair, take profit. The uptrend has been seriously challenged and a 50% retracement of the November rally would take EUR/SEK to 9.15. That said we see macro- and market-oriented arguments pushing the pair higher yet again in December.

Our short-term model has pulled the spot rate gradually higher and with fair value around 9.30 the weakening of the krona is fully justified. The Riksbank has been re-priced for more aggressive rate cuts and the euro crisis has dented risk appetite, sending stock markets lower and leaving the VIX index at somewhat elevated levels. Since we: 1) sincerely doubt that there will be a near-term resolution to the crisis and since we still lack a circuit breaker for the low/no confidence environment and since we 2) fully buy in to the view that the Riksbank will embark on an easing cycle in December, we prefer to buying EUR/SEK on dips.

The cyclical outlook in Sweden and abroad has deteriorated further. Sweden, a highly export-dependent economy, will be hit hard by sharp global slowdown. We have recently cut our GDP forecast and expect negative growth in 2012. The fourth quarter may actually be the first quarter in a series printing negative consecutive growth. In fact the stronger-than-expected Q3 reading even raised the risk for negative growth in Q4, since the positive surprise was due to involuntary build up of inventories, something that is likely to be reversed in Q4 with heavy sales, not least in the retail sector, pushing inflation even lower. We project CPIF inflation (excluding mortgages) of below 1% during most of 2012 and even as low as 0.5%. It’s not hard to find downside risks to this forecast.

Swedish monetary policy is expected to make a U-turn on 20 December by delivering a 25bp cut, much in line with market pricing. If the ECB slashes rates again next week, 50bp from the Riksbank cannot be ruled out (acknowledging that the GDP figure could be viewed as a counter argument). If it unexpectedly cuts 50bp, EUR/SEK will surely spike significantly higher as neither the money nor the foreign exchange market would be prepared. We believe the Riksbank will follow up with a series of rate cuts in 2012 taking the repo rate to 0.5% by H2 12, which is marginally lower than the market is currently pricing in. Relative yields might not be a very strong argument for a weaker krona, since both the Riksbank and the ECB are expected to cut more than is priced in. But with lower Swedish rates the rate advantage disappears which could reverse previous carry-related krona demand.

PPM flows: Buy the rumour sell the fact

December is also accompanied by recurrent flow stories. New Swedish pension money is disbursed on 13 December. The Swedish Pension Agency (PPM) just reported that the total amount this year is SEK32.1bn, which is slightly (about SEK2bn) more than in the previous two years. We estimate that SEK10bn to SEK15bn will hit the Swedish krona. On the one hand, appetite for global equities may be dampened due to the debt crisis (less krona outflows than previous years), but on the other hand, the stronger krona exchange rate compared with last year may render smaller hedge ratios on any given foreign investment (more krona outflows).

We draw the following conclusions:

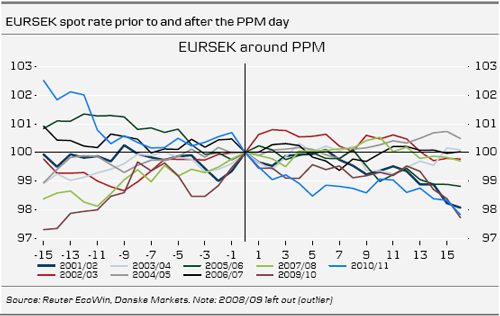

- We have learned that EURSEK, on average, rises before the PPM date (in seven years out of 10 to be exact).

- PPM has no persistent effects on EURSEK – the pair falls once the PPM date has passed (six-seven years out of 10).

- EUR/SEK tends to fluctuate significantly on the transaction day.

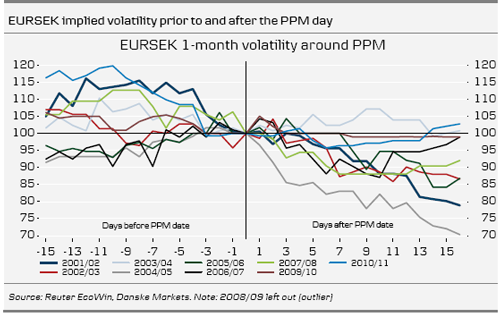

- Implied volatility tends to fall in the period after PPM has passed (eight years out of 10).

Conclusion

The technical picture is less clear-cut following the late correction, and we could see EUR/SEK completing its 50% retracement of the November rally before it’s ready to test 9.30 again and potentially challenge the 9.3950 peak. From a macro/flow perspective we are bullish about EUR/SEK going into the final month of the year as political uncertainty weighs on sentiment, PPM and as the Riksbank embarks an easing cycle on 20 December.

That said we don’t expect EUR/SEK to explode on the upside as it did in 2008/09. The upside is capped by strong fundamentals, savings surplus, low public debt, low default risk (CDSs), stable AAA rating and low valuation. Foreign demand for Swedish quality is intact, as illustrated in foreign holdings of Swedish government bonds, now more than 50%. In addition, we expect a rebound in appetite for riskier assets later on, which combined with fundamentals and valuation should lend medium-term support to the krona. Unlike 2008 the Swedish exporters are not over-hedged, which limits the downside in the krona this time around.

There is still a good chance that these factors and a further exclusive euro sell off, will take the krona back into overvalued territory vs the euro – that is below 9.00 during 2012.