Tuesday April 5: Five things the markets are talking about

Trading volumes across the various asset classes are lower than usual, volatility is non descript, but brewing, while the ‘mighty’ dollar remains somewhat contained for now after Fed Yellen’s overtly ‘dovish’ stance in late March.

With investors continuing to chase a clear directional play perhaps they will have to wait for the Fed (Wednesday) and ECB (Thursday) to respectively publish their minutes from their most recent policy meetings for a stronger conviction?

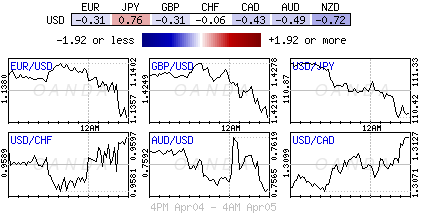

Currently, global equities are having trouble finding traction, crude prices remain suspect ahead of Doha meeting (April 17), global yields are giving back end of last week gains (U.S 10’s +1.775%) while the rise of ‘risk aversion’ sees the yen trade at its strongest level this year – JPY’s ¥110 handle has not been breached since the BoJ’s surprise easing in Oct 2014 which expanded the annual monetary base to +¥80T.

1. Investors be warned

Boston Fed President Rosengren struck a somewhat more ‘hawkish’ tone than usual yesterday. Rosengren highlighted that the gulf between the Fed’s outlook and market expectations has widened considerably, and he believes that the market has got it wrong.

The market has been interpreting Yellen’s remarks from last week as overtly ‘dovish,’ suppressing the more hawkish comments of other recent Fed speaker’s year to date. This continues to penalize the ‘mighty’ U.S dollar as investors unwind the currency’s rate differential premium, while flattening the U.S yield curve (market is pricing in one, maybe two rate hikes for this year. Back in December, the Fed’s “dot plot” had suggested four rate hike in 2016).

Rosengren – a 2016 FOMC voter – believes “that financial markets may have reacted too strongly.” His assessment is that the US economy is continuing to improve despite the headwinds from abroad. “If my forecast is right, it may imply more increases in short-term interest rates than are currently priced into futures markets.”

Fed-funds currently show +26% odds of a June rate hike and +66% for December – which suggests that many expect the Fed to tighten once in 2016, if at all (U.S 10’s yield is now at +1.783%).

2. Reserve Bank of Australia (RBA) keeps rates on hold

As expected, the RBA kept interest rates on hold Tuesday (+2%), but returns to jawboning the Aussie dollar down (A$0.7557).

Governor Stevens again has indicated that the AUD’s recent rise (up +7% in March) could complicate a recovery in their economy. Steven’s suggests that decisions by other central bankers to lower interest rates have contributed to the rise of the AUD, as too has the increase in commodity prices.

Aside from the RBA removing the previous statement’s reference to “financial turbulence threatening weaker global and domestic demand,” this morning’s statement was largely unchanged; reiterating that China’s growth rate has continued to moderate and that Aussie inflation would remain low over the next year or two.

3. Yen on the move

Overnight, Japan saw surprisingly strong demand in the their 10-Year JGB auction, and this despite the negative yields for the second straight month.

Also, as speculated, government officials announced the details of frontloading their FY2016/17 budget, with +80% of infrastructure spending expected in the April-Sept period.

The BoJ’s Kuroda continues to defend QQE (Quantitative and Qualitative Monetary Easing), pointing to oil price decline as the key reason for low inflation and adding that technically “it is possible to push interest rates further into negative territory.” Note however, traders have been paring their expectations of deeper cuts to rates on reserves, and Kuroda’s testimony does not seem to have influenced that view as JPY continues to rally (¥110.42).

Many are now speculating that the BoJ may be forced to once again downgrade their inflation expectations later this month after yesterday’s Tankan survey cut its inflation forecasts for the next 1-, 3-, and 5-years.

4. Reserve Bank of India (RBI) cuts rates as expected

As expected, the Reserve Bank of India announced its widely expected easing of monetary policy. The -0.25% cut had been predicted by many, since conditions have been met for additional stimulus by the central bank.

Analysts note that Modi’s government have exercised “fiscal prudence in its latest budget review, while consumer inflation levels have come down recently.”

Both the currency (USD/INR 66.07) and domestic stock market seemed unimpressed by the marginal easing of borrowing costs, likely because the magnitude of the rate-cut was already priced-in.

5. Euro area weaker than indicated last month

Earlier this morning, Euro services PMI’s missed expectations to highlight the continued fragility of the regions recovery.

Last months preliminary estimate of activity in both manufacturing and services pointed to a revival as Q1 drew to a close. But the final Markit composite PMI released this morning paints a different picture – Euro Q1 activity has increased at its slowest pace since Q4, 2014.

The survey also confirms that ECB’s Draghi continues to face an uphill battle to raise the rate of inflation towards the CB’s desired +2% level – March CPI was -0.1% lower than a year earlier, and this despite Euro businesses slashing prices for the sixth consecutive month.

Not all things are bad for the region. Other data released showed that retail sales rose for the fourth straight month in February (+0.2%) – many had been projecting a slight decline m/m.