There are three reasons why people have made the mistake of thinking that private real estate is less volatile.

(1) Comparing unlevered private returns to levered public returns: The most commonly used measures of private real estate are the NCREIF Property Index (NPI) and the NCREIF ODCE; the NPI measures unlevered returns on institutional core property investments even if the investments were made with leverage, while the ODCE measures returns from open-end diversified core private equity real estate funds, which typically use leverage in the range of 20%-30%. Public equity real estate (equity REITs listed on stock exchanges) typically use leverage in the 35%-45% range. If the underlying assets have the same volatility—and they do—then the differences in leverage will cause differences in return volatility. That means if you make a private real estate investment that uses more leverage than listed REITs (say, a value added or opportunistic fund) then your actual returns will actually be more volatile.

(2) Comparing appraisal-based returns with transaction-based returns: The biggest problem is that returns on private real estate are typically measured using appraised values rather than actual market values, and appraised values are radically smoothed relative to actual market values. To see this, compare the NPI with the NCREIF Transaction Based Index (NTBI), which is computed from actual transaction values on those properties from the NPI data base that actually transacted in each quarter. Over the available historical period 1984Q2-2014Q3 the appraisal-based NPI showed volatility of just 4.4% (and the appraisal-based ODCE just 5.7%) while the transaction-based NTBI showed nearly three times as much volatility at 12.3%. In fact, the biggest benefit to investors of private equity real estate—I would say the only benefit—is that it is legal, and considered ethical, to report appraisal-based returns that disguise the true volatility of the investments.

(3) Comparing end-to-end returns with averaged returns: Private real estate simply doesn’t transact frequently enough to compute a daily index based on actual market transaction prices, and appraisals are too expensive to perform every day (and too inaccurate to make the exercise worthwhile!). Because of that, returns on private real estate investments are typically measured by aggregating all transactions or appraisals over a given quarter (or month) so there’s enough data to compute the index. This results in “aggregation bias”: while the mathematical details vary for different indexes, in effect each index tells us the average transaction price or appraised value over the quarter. In contrast, returns on liquid real estate investments (listed equity REITs) are measured using the last stock transaction for each REIT on the last day of each quarter, rather than using the average stock transaction for each REIT over the entire quarter.

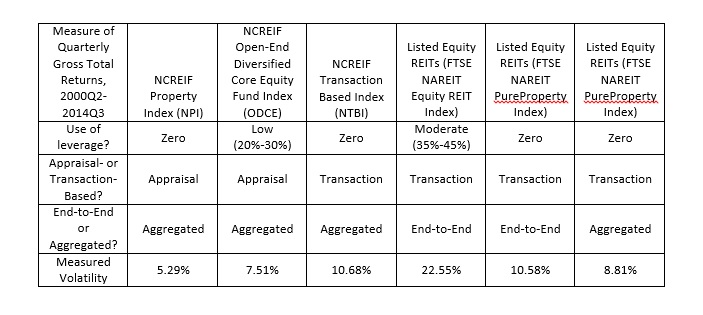

Here’s a comparison that makes all three points:

As you can see, if we use listed equity REIT returns but eliminate the use of leverage and average over all trading days in the quarter—thereby making it as comparable as possible to the NCREIF Transaction Based Index—public real estate is actually 17½% LESS volatile than private real estate! (That’s comparing 8.81% with 10.68%.) In other words, while using leverage adds volatility, being traded on the stock exchange does not.

Is it believable that public real estate is actually less volatile than private real estate? It’s not just believable, it’s to be expected. Volatility is a measured of uncertainty regarding asset values. Think of a crisis: people trade assets at lots of different values because they have so much uncertainty regarding the factors that determine the asset values: the future stream of earnings, and the appropriate discount rate. A market in which more transactions give investors greater information about those underlying factors—that is, a market that is liquid and information-efficient, such as the stock market in which listed equity REIT stocks trade—SHOULD be less volatile than an illiquid, information-inefficient market such as the market for properties or (worst!) the market for private equity fund shares.

What are the true volatilities of public and private real estate? The best measure of public real estate returns, on an unlevered basis, comes from the FTSE NAREIT PureProperty® Index, so the best estimate of public real estate volatility over the period 2000Q2-2014Q3, using quarterly returns measured end-to-end, is 10.58%. Perhaps the best way to measure private real estate returns on a comparable basis would be to adjust that by 17%, which would give 12.82%.

The key takeaway is not that public real estate is less volatile than private real estate: it’s that private real estate is NOT less volatile than public real estate. Independent research supports this, including this 2013 academic paper by Hoesli & Oikarinen (“We also find that volatilities generally do not differ significantly between REIT and direct real estate regardless of sector and investment horizon”) and this 2012 paper by Pedersen et al. of PIMCO (“the volatility of private real estate is generally comparable to the risk of public REIT investments”).

A version of the slide shown above, drilling down to different property types and different regions is updated every quarter.