Expedia, Inc. (NASDAQ:EXPE) is set to report second-quarter 2017 results on Jul 27 after the bell.

The company has a Zacks Rank #2 (Buy) and an Earnings ESP of +16.67%, a combination that increases the likelihood of a positive surprise. This is because, per our proven model, a stock needs to have both a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 or 3 (Hold) to beat estimates. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

We don’t recommend Sell-rated stocks (Zacks Rank #4 or 5) going into the earnings announcement.

Notably, Expedia’s surprise history has been decent. The company beat estimates in one of the last four quarters, missed it twice and matched the same on one occasion. It delivered an average positive surprise of 7.1% over the time frame.

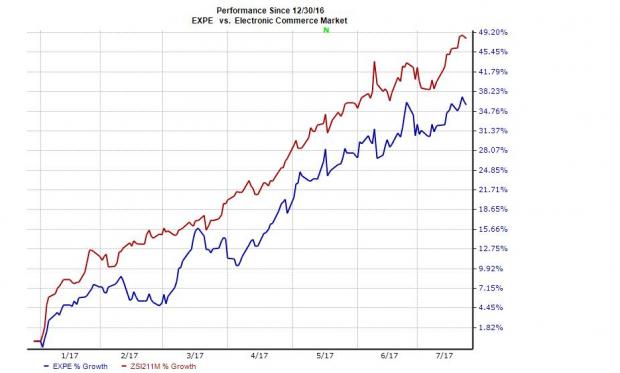

Year to date, the stock has underperformed its industry, gaining 35.9% compared with the industry’s rise of 48.1%.

First Quarter Snapshot

Reported loss was narrower than the Zacks Consensus Estimate and down 13.3% year over year. Revenues surpassed the consensus mark and were up 15% year over year. Gross bookings increased 14.1% for the same time frame.

On a year-over-year basis, Merchant, Agency, Advertising & Media and Home Away grew 9.2%, 10.4%, 47.7% and 30.3%, respectively. Domestic and international businesses grew a respective 12% and 19.1% respectively.

Second Quarter Expectations

Expedia expects adjusted EBITDA growth of 10–15% through the year. The company estimates total cloud costs to be $110 million. Excluding cloud expenses, growth is estimated to be 14–19%. Expedia’s plan to ramp-up sales organization in the Egencia business is expected to impact margin in the near term.

The company projects depreciation expense to grow in the mid-20% range with the pace of growth decelerating from the first quarter through the end of the year.

Expedia, Inc. Price and EPS Surprise

Total selling and marketing costs are expected to grow faster than revenues for the remainder of the year. Technology and content expenses are expected to follow the same track in the second quarter and accelerate further in second-half 2017.

Moreover, Expedia now expects capital expenditure excluding cost related to its headquarters project to decline on a year-over-year basis.

Stocks that Warrant Look

Here are some stocks that you may want to consider as our model shows these have the right combination of elements to post a positive earnings surprise:

Cypress Semiconductor Corporation (NASDAQ:CY) , with an Earnings ESP of +11.11% and Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

Lam Research Corporation (NASDAQ:LRCX) , with an Earnings ESP of +1.33% and a Zacks Rank #1.

The Priceline Group Inc. (NASDAQ:PCLN) , with an Earnings ESP of +2.31% and a Zacks Rank #3.

More Stock News: This Is Bigger than the iPhone!

It could become the mother of all technological revolutions. Apple (NASDAQ:AAPL) sold a mere 1 billion iPhones in 10 years but a new breakthrough is expected to generate more than 27 billion devices in just 3 years, creating a $1.7 trillion market.

Zacks has just released a Special Report that spotlights this fast-emerging phenomenon and 6 tickers for taking advantage of it. If you don't buy now, you may kick yourself in 2020. Click here for the 6 trades >>

Expedia, Inc. (EXPE): Free Stock Analysis Report

The Priceline Group Inc. (PCLN): Free Stock Analysis Report

Cypress Semiconductor Corporation (CY): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Original post