After asset allocation and rebalancing, one of the tasks on the short list of strategic-minded portfolio design and management is developing reasonable assumptions about risk premiums. In fact, all three are intimately linked. You can hardly make informed decisions about any one without spending some time analyzing the other two. Forecasting is challenging, of course, to say the least. But it’s also necessary and inevitable. Investing by nature is a process of making decisions about the future, and so the price of doing business in the money game is developing assumptions.

There are, of course, many ways to proceed. My preference is to begin by estimating equilibrium-based risk premia for all the major asset classes and my Global Market Index, or GMI (a passively weighted mix of all these asset classes). As I’ve written before, both on The Capital Spectator and in my book Dynamic Asset Allocation, this is a sound methodology for generating benchmarks for expectations. It’s not perfect, but nothing is. In any case, every thousand-mile journey starts with a first step, and this is a prudent way to put your foot forward while minimizing the potential for stumbling.

Step One

The basic idea is to reverse engineer expected risk premia by making assumptions about the overall market’s price of risk, the volatility of each asset class and the correlation matrix for all of the above(1). With that data in hand, we can estimate the implied risk premia.

The critical issue, of course, is developing respectable estimates for each of the inputs. Once again, there are numerous methodologies to consider. It seems prudent, however, to start with a basic, transparent approach, if only as a baseline.

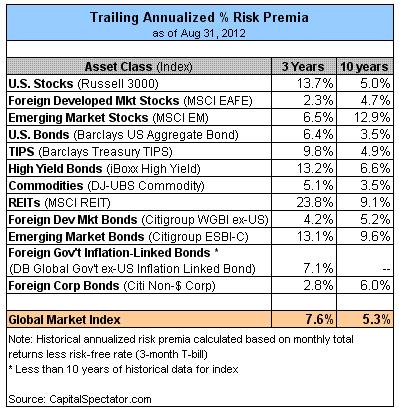

For instance, let’s allow the data to “speak” to us for estimating the inputs in a rather intuitive way. For the market price of risk overall, I calculate the rolling three-year annualized Sharpe ratio for GMI and then take the average of the annualized data as a long-term estimate for the future. I do the same to estimate volatility and correlation for each of the asset classes. Before we review what the numbers tell us, let’s take a brief tour of where we’ve been for some perspective. First, here’s how GMI and the major asset classes stack up in terms of realized risk premia over the past three- and 10-year periods (remember, here and throughout we’re referring to risk premia, or returns before adding in a “risk-free” rate, such as the yield on a three-month T-bill):

Compute Ratios

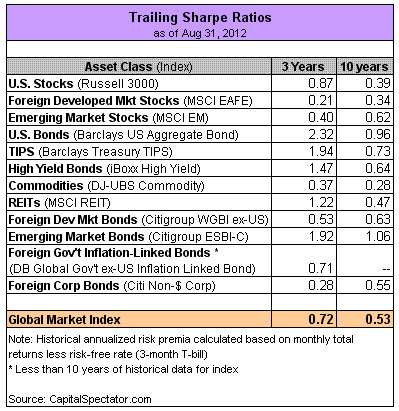

Next, let’s compute realized Sharpe ratios in recent history for a simple comparison of risk-adjusted performance:

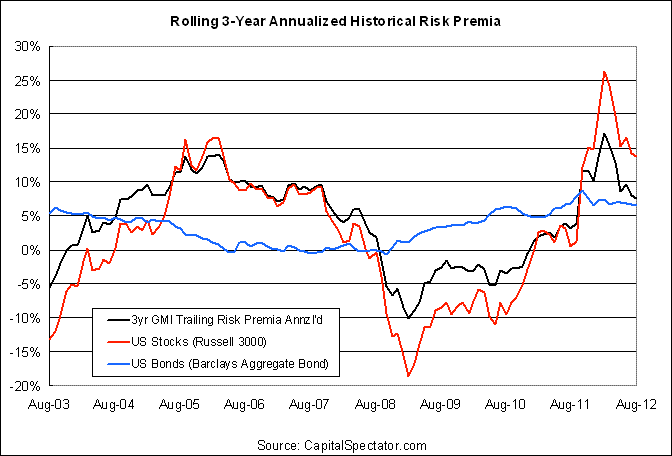

For a richer view of how risk premia have fluctuated, consider the graph below, which compares rolling three-year annualized risk premia for GMI and U.S. stocks and bonds:

Estimate Risk

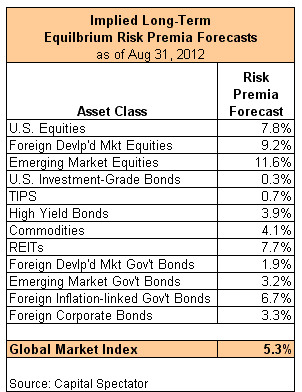

Now let’s look ahead by estimating equilibrium risk premia for the long-run future, which is computed for each asset class as follows:

GMI’s expected Sharpe ratio * expected volatility of each asset class * expected correlation of each asset class with GMI

Plugging in estimates based on the methodology outlined above dispenses the following:

Weighing The Risk

What can you do with the information in the table above? You might start by considering if the expected risk premia are satisfactory or not. For instance, if GMI’s expected risk premia of 5.3% strikes you as insufficient for your financial objectives, you might consider how to engineer a higher rate of performance. One possibility: reweighting the major asset classes. GMI’s implied risk premia is based on a market-value weighted mix of the major asset classes. In theory, that’s the optimal asset allocation for the average investor with an infinite time horizon. Unless you’re a foundation or pension fund, that’s wildly impractical, of course, and so there’s a reasonable case for modifying Mr. Market’s asset allocation to suit your particular needs.

Along those lines, you might decide to leave off one or more asset classes. You might also estimate risk premia with alternative methodologies for additional insight about the near-term future. For instance, let’s say that you have a lot of confidence in the dividend-discount model (DDM) for predicting equity market performance over the next 3 to 5 years. After crunching the numbers, you find that DDM tells you that the stock market’s expected performance will be considerably higher than the equilibrium-based estimate for the long run. In that case, you have some tactical information. As such, you may decide to overweight equities relative to the market weight as a device to raise your portfolio’s expected return.

What you can’t do is get blood out of a stone. No one really knows what risk premia will be in the months and years ahead, which is why relying on forecasting alone (particularly for the short-term future) is asking for trouble. In other words, you should deviate from Mr. Market’s asset allocation carefully, thoughtfully and for reasons other than assuming that you’re smarter than everyone else (i.e., the market).

Make Risk Assumptions

That said, looking ahead by making assumptions about risk (as opposed to forecasting return directly) is a reasonable framework for developing intuition about the future. Forecasting risk isn't easy, but there's quite a lot of theoretical and empirical support for thinking that we can generate a better read on this data vs. trying to figure what performance will be. The real value here is less about any one round of estimating. A better approach is to routinely forecast risk premia and track how your expectations change through time. This will provide an additional layer of insight in the delicate art of formulating expectations for designing and managing portfolios.

It’s also important to keep in mind that relatively few investors end up adding value over GMI (or comparable portfolios) without taking on substantially more risk. Remember too that it's easy to assume more risk, but it doesn't easily translate into higher return. Even the pros tend to fall short overall vs. a simple multi-asset allocation strategy, as I discussed a few months ago. That’s not terribly surprising, but it offers essential guidance that should keep us wary in the matter of overconfidence.

Nonetheless, it’s important to run the numbers regularly and make a habit of looking forward in a systematic way using various methods. Mr. Market’s asset allocation isn’t likely to be ideal for many, if any, investors, which is why estimating risk premia is crucial. Indeed, everyone needs context for deciding how to customize the portfolio. But there are limits to our capacity to improve on a passive mix due to the one constant you can count on: uncertainty about the future. As a result, too much of a good thing on the analytical front can and does bite back at times.

(1). The original methodology for generating equilibrium expected returns was outlined by William Sharpe in “Imputing Expected Returns From Portfolio Composition,” Journal of Financial and Quantitative Analysis, June 1974. For a more recent treatment, see the "Reverse Optimization" section in Thomas Idzorek’s monograph via Morningstar.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

How Much Do You Know About Risk?

Published 09/21/2012, 02:28 PM

Updated 07/09/2023, 06:31 AM

How Much Do You Know About Risk?

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.