We issued an updated research report on Xylem Inc. (NYSE:XYL) on Aug 23.

The water solutions provider currently carries a Zacks Rank #3 (Hold) and has a market capitalization of approximately $14.7 billion.

Below we discussed why it will be prudent for investors to hold on to this stock for now.

Factors Favoring Xylem

Top-Line Strength: The company serves customers in various end markets — including industrial, commercial, residential and utilities. This diversification helps Xylem to deal with weakness in some markets, with strength in others. For 2019, organic sales in the utility end market are predicted to increase in a mid to high-single digit, higher than the previously mentioned mid-single-digit growth. Also, strength in emerging markets, wastewater and the water market in the United States, and growth prospects in infrastructure analytics and smart meter will be beneficial. In the commercial end market, organic sales are predicted to grow in a mid-single digit.

Notably, the company’s organic revenues grew 5% on strengthening end markets, especially utilities, in the second quarter of 2019. Also, healthy performances were recorded in China, India and the United States.

In the past three months, the company’s share price has gained 2.2% compared with the industry’s growth of 0.6%.

Shareholder-Friendly Policies: Xylem effectively uses capital for rewarding shareholders handsomely through dividend payments and share buybacks. It is worth mentioning here that the company hiked the quarterly dividend rate by 14% in January 2019. In the first half of 2019, it paid out dividends amounting to $87 million and bought back shares worth $39 million.

For 2019, Xylem anticipates rewarding shareholders with dividend payouts of $175 million. Share count at the end of the year is expected to be approximately 181 million.

Long-Term Growth Prospects: Rising demand, spurred by the water sector’s digitization and investments in technological capabilities, are tailwinds for Xylem. Backed by these and other factors, the company is on track to achieve most of its long-term targets.

As discussed at its investor day in 2017, Xylem targets organic growth of 4-6% and adjusted operating margins of 17-18% by 2020. Adjusted earnings per share are likely to be in mid-teens and capital that can be used for deployment is expected to total $3.5 billion.

Factors Working Against Xylem

Over-Valued Stock and Earnings Estimates: The company’s shares currently seem overvalued compared with the industry, using the P/E (TTM) valuation method. The stock’s three-month P/E multiple is 25.53x, higher than the industry’s multiple of 20.03x. Also, the stock is currently trading higher than the industry’s three-month multiple of 20.50x. This makes us cautious about the stock.

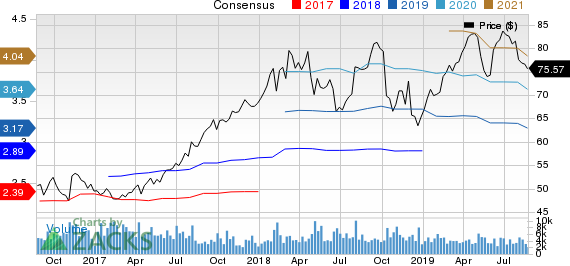

In addition, the company’s earnings estimates have been declined in the past 30 days. Currently, the Zacks Consensus Estimate for its earnings is pegged at $3.17 for 2019 and $3.64 for 2020, reflecting declines of 1.6% and 2.2% from the respective 30-day-ago figures.

Xylem Inc. Price and Consensus

Xylem Inc. price-consensus-chart | Xylem Inc. Quote

Lowered Projections: For 2019, Xylem’s organic sales in the industrial end market are predicted to be adversely impacted by weak business in the Middle East and Europe, softness in China, and moderation in the U.S. general industry. Also, businesses will be soft in the oil and gas/mining market. Industrial organic sales will likely grow in a low-single digit, down from previously mentioned low to mid-single-digit range.

In addition, the residential market will likely suffer from softness in European markets and the dwindling U.S. housing market. Residential organic sales are predicted to be flat to up in a low-single digit, down from the previously stated low-single-digit growth.

For 2019, Xylem predicts revenues of $5.29-$5.38 billion versus the previously stated $5.3-$5.4 billion. Also, adjusted earnings per share are predicted to be down from $3.12-$3.32 mentioned earlier to $3.12-$3.22, with the mid-point declining from $3.22 to $3.17.

Forex & Cost Woes: Geographical diversification is reflective of a flourishing business of the company. However, this diversity exposed it to headwinds arising from geopolitical issues and unfavorable movements in foreign currencies. In the second quarter of 2019, forex woes adversely impacted the company’s sales growth by 3% and earnings by one cent per share. Persistence of such headwinds will continue impacting its top-line results.

Also, cost inflation and investments adversely impacted Xylem’s operating margin in the second quarter of 2019. We believe that rising costs and expenses, if unchecked, will continue to hurt the company’s margins in the quarters ahead.

Stocks to Consider

Some better-ranked stocks in the industry are Graham Corporation (NYSE:GHM) , DXP Enterprises, Inc. (NASDAQ:DXPE) and Roper Technologies, Inc. (NYSE:ROP) . All these stocks currently carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In the past 30 days, earnings estimates for these stocks have improved for the current year. Further, earnings surprise for the last reported quarter was 100% for Graham, 4.29% for DXP Enterprises and 0.99% for Roper.

Wall Street’s Next Amazon (NASDAQ:AMZN)

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Roper Technologies, Inc. (ROP): Free Stock Analysis Report

DXP Enterprises, Inc. (DXPE): Free Stock Analysis Report

Graham Corporation (GHM): Free Stock Analysis Report

Xylem Inc. (XYL): Free Stock Analysis Report

Original post

Zacks Investment Research