We have issued an updated research report on Ingersoll-Rand plc (NYSE:IR) on Aug 9.

This industrial machinery maker currently carries a Zacks Rank #3 (Hold). Its market capitalization is approximately $28.8 billion.

Below we discussed why it will be prudent for investors to hold on to this stock for now.

Factors Favoring Ingersoll-Rand

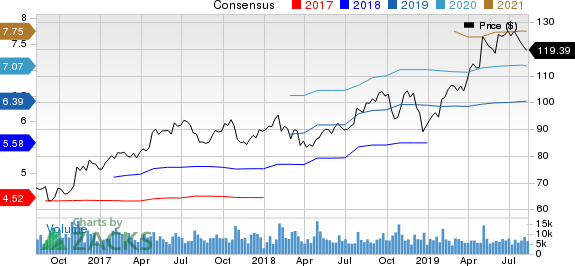

Share Price Performance, Earnings Projections: Market sentiments seem to be working in favor of the company over time. In the past six months, its share price has gained 14.2%, higher than the industry’s growth of 4.7%.

We believe that impressive financial results helped in driving sentiments for the stock. The company recorded positive earnings surprise of 2% in the second quarter of 2019. On a year-over-year basis, earnings expanded 13% on solid revenue growth, margin expansion and lower taxes.

For 2019, Ingersoll-Rand anticipates gaining from strengthening revenue performance, effective operating system and execution capabilities. Also, investments toward innovation, technology and footprint-optimization initiatives to trim costs will be beneficial. It projects adjusted earnings per share of roughly $6.40 in 2019, higher from the previously stated $6.35.

Further, the company’s earnings estimates have been raised in the past 30 days. The Zacks Consensus Estimate for its earnings is pegged at $6.39 for 2019, reflecting 0.2% growth from the 30-day-ago figure.

Ingersoll-Rand PLC (Ireland) Price and Consensus

Ingersoll-Rand PLC (Ireland) price-consensus-chart | Ingersoll-Rand PLC (Ireland) Quote

Top-Line Strength: The company provides services through two business segments — Climate Solutions and Industrial Technologies. These segments have operations in various end-markets, especially non-residential HVAC (heating, ventilation and air conditioning), residential HVAC, electric vehicles & industrial products, and transport markets.

For 2019, Ingersoll-Rand believes that healthy growth in non-residential HVAC markets in China, North America and Europe will be beneficial. Also, solid backlog, orders rates and pipeline will likely support performance in the second half of 2019. The residential HVAC market will gain from business in North America. Small electric vehicle & industrial product markets will be advantageous too. Transport business will be healthy in North America but weakness might be seen in Europe.

For 2019, the company anticipates revenues to increase 5.5-6.5%, higher than 4-5% mentioned earlier. Organic sales growth is maintained at 5-6%.

Capital-Allocation Policies: The company effectively uses capital for making acquisitions and growth investments as well as rewarding shareholders handsomely through dividend payments.

For instance, the company acquired ICS Cool Energy in January 2018 while entered a joint venture with Mitsubishi Electric Corporation — with equal partnership in Mitsubishi Electric Trane HVAC — in May. In addition, Precision Flow Systems was acquired in May 2019. This particular buyout, predicted to support the company’s existing fluid management business, is likely to boost sales by 1.5% (or $250 million) in 2019.

With regard to shareholders’ reward, the company distributed $259.4 million as dividend payouts and repurchased shares worth $250 million in the first half of 2019. It is worth noting here that Ingersoll-Rand announced an 18% hike in the quarterly dividend rate in June 2018. Also, it received approval for $1.5 billion worth share buyback program in October 2018. The company anticipates repurchasing shares worth $500 million in 2019.

Factors Working Against Ingersoll-Rand

Over-Valued Stock: Ingersoll-Rand’s shares currently seem overvalued compared with the industry, using the EV/EBITDA (TTM) valuation method. The stock’s six-month EV/EBITDA multiple is 14.06x, higher than the industry’s multiple of 12.28x. Also, the stock is currently trading higher than the industry’s six-month multiple of 12.97x. This makes us cautious about the stock.

Higher Costs and Expenses: Ingersoll-Rand’s cost of sales, and selling and administrative expenses grew 4.4% and 4%, respectively, in the second quarter of 2019. Operating margin in the quarter suffered from adverse impacts of material inflation resulting from business investments, tariffs and other inflationary pressures.

For 2019, the company noted that tariff-related headwinds, including the recent List 3 tariffs applied on China imports, and material-related inflationary pressure will be concerning. However, effective pricing and productivity measures will be boon. Corporate expenses in the year are predicted to be $250 million.

Long-Term Debt: Ingersoll-Rand’s long-term debts were $4,920.6 million at the end of the second quarter of 2019, reflecting an increase of 31.5% from 2018 end. In March 2019, the company raised funds through the issuance of senior notes. With relation to this offering, it predicts interest expenses to be $60 million, with roughly $47 million likely to be incurred in 2019.

We believe that the company’s highly leveraged balance sheet might be detrimental as it increases financial obligations and hurt profitability.

Stocks to Consider

Some better-ranked stocks in the industry are Graham Corporation (NYSE:GHM) , DXP Enterprises, Inc. (NASDAQ:DXPE) and Dover Corporation (NYSE:DOV) . All these stocks currently carry a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In the past 60 days, earnings estimates for these stocks improved for the current year. Further, earnings surprise for the last reported quarter was 100% for Graham, 4.29% for DXP Enterprises and 0.65% for Dover.

Today's Best Stocks from Zacks

Would you like to see the updated picks from our best market-beating strategies? From 2017 through 2018, while the S&P 500 gained +15.8%, five of our screens returned +38.0%, +61.3%, +61.6%, +68.1%, and +98.3%.

This outperformance has not just been a recent phenomenon. From 2000 – 2018, while the S&P averaged +4.8% per year, our top strategies averaged up to +56.2% per year.

See their latest picks free >>

Ingersoll-Rand PLC (Ireland) (IR): Free Stock Analysis Report

DXP Enterprises, Inc. (DXPE): Free Stock Analysis Report

Graham Corporation (GHM): Free Stock Analysis Report

Dover Corporation (DOV): Free Stock Analysis Report

Original post

Zacks Investment Research