Summary: Growth slows in the developed nations due to several factors, as debt levels rise. Have we entered the “coffin corner” where we cannot growth sufficiently fast to service our debt? This is the follow-up to The dilemma of the US economy: can’t take off & too close to the brink.

In the absence of effective and comprehensible economic theory, economists often rely on analogies. Such as comparisons with aerodynamics. Flying complex vehicles at high speed under variable conditions, often with inadequate or old information — the role of pilot has similarities with that of central banker.

A common mistake of bankers is raising rates to curb inflation while the economy is in fact on the brink of recession. That’s similar to a “graveyard spiral“, in the past a frequent cause of crashes. From Wikipedia, slightly edited:

Graveyard spirals occur in nighttime or poor weather conditions with no horizon visible to provide visual correction for misleading inner-ear cues. … The pilot mistakenly believes the wings to be level, but with a descent indicated on the instruments, so the pilot attempts to climb. In a banking turn, however, the plane is at an angle and flying in a large circle. This tightens that circle, causing the plane to fall at an increasing rate.

This flying by “the seat of the pants” and failing to recognize instrument readings is the most common source of “controlled flight into terrain”.

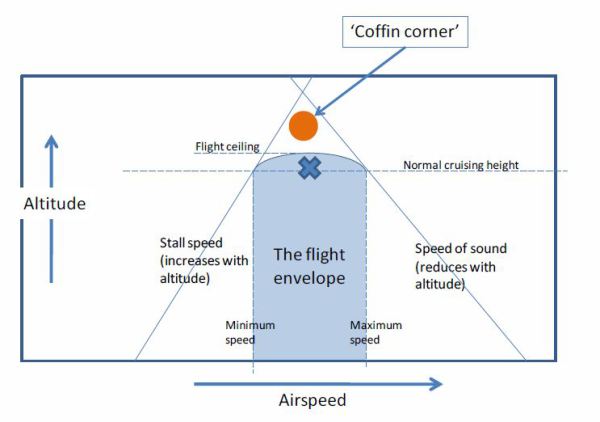

Today the US economy might have flown into conditions similar to another perilous aerodynamic situation — the coffin corner. From the Sky-brary (slightly edited):

The coffin corner (aka Q Corner) is the altitude near which a fast aircraft’s stall speed equals its critical Mach number. As an aircraft climbs towards the altitude that defines its coffin corner, the margin between stall speed and critical Mach number becomes smaller and smaller until the Flight Envelope boundaries intersect. At this point any change in speed creates serious problems. Turning the aircraft could result in exceeding both limits simultaneously, as the inside wing slows down and the outside wing increases speed. Encountering turbulence can push the aircraft outside its flight envelope.

Is the US economy at the “coffin corner”?

From “In a debt ‘coffin corner”“, Andrea Cicione, Lombard Street Research, May 2014 — LSR is a top-quality macroeconomic forecasting consultancy.

.

Lombard Street Research, May 2014

Lombard Street Research, May 2014Aviation metaphors are a familiar staple of the financial and economic commentary: growth reaches stall speed; economies experience hard landings; markets encounter severe turbulence; corporate earnings reach escape velocity; and so on. Everyone understands these.

… Airplanes can fly safely only as long as their airspeed remains within certain limits. If speed falls below the so-called stall speed, the wings aren’t able to generate enough lift and the aircraft falls out of the sky. Similarly, if an aircraft (at least one not designed for supersonic flight) gets too close to the speed of sound, flow separation occurs, leading to loss of lift or even structural failure. At “normal” altitudes the difference between stall speed and overspeed is large, allowing planes to fly safely at a broad range of speeds.

However, things get more dangerous as altitude increases: stall speed goes up, as the air gets thinner and thus less able to support the weight of the airplane; and the overspeed limit goes down, as the speed of sound decreases with lower air temperature. As a result, at high altitudes the range of speeds at which an aircraft can function becomes so narrow that even the best pilots become unable to keep the plane on level flight.

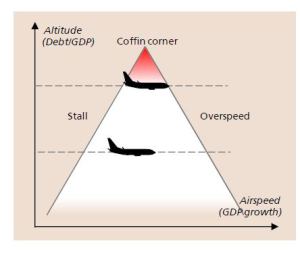

Why does this matter? Well, replace “airspeed” with “GDP growth”, and “altitude” with “debt-to-GDP”, and you can probably start to see where we’re heading with this. According to the OECD, the government debt-to-GDP ratio for 10 large economies (Australia, Canada, France, Germany, Italy, Japan, Korea, Spain, the UK and the US) has surpassed the previous peak recorded at the end of WWII. … the overall debt burden for the 34 OECD member countries will continue to climb in coming years. While there has been selective deleveraging in certain sectors of the global economy (e.g. US households and DM banks), debt, rather than having been reduced, has mostly been transferred from the private to the public sector.

The question is whether advanced economies, in an effort of trying to limit the damage caused by the Global Financial Crisis, have put themselves into a debt coffin corner. With debt-to-GDP (altitude) as high as it is, they can’t allow growth (airspeed) to slow too much, or debt risks becoming unsustainable. At the same time, high debt levels are likely to be a material drag, making growth hit an insurmountable economic “sound barrier” much earlier. This is because without the boost provided by credit growth, it is difficult to achieve the kind of GDP growth that was possible when debt-to-GDP was lower.

But there’s more. High levels of debt-to-GDP ratios make it difficult for governments and central banks to steer the economy – just as excessively high altitude makes it difficult for a pilot to keep control of the aircraft. Central banks have successfully employed Zero interest rates policy (ZIRP) to keep debt sustainable but, as the economy continues to recover, they may now find themselves cornered: keeping rates as low as they are may lead to overheating (or even bubbles) in certain sectors of the economy; but raising them may stall others by making the existing debt impossible to service.

Now for a bad scenario

What if the economy’s long-term growth rate continues to decline? What if our aggregate debt continues to increase so that the economy’s “stall speed” increases (i.e., a higher minimum speed is needed to keep the economy aloft)? What if the two lines cross?

Who knows what the future holds? There is relatively little research on these matters, and little agreement among economists.

About Lombard Street Research

LSR is a leading provider of independent macroeconomic research, founded in 1989. They provide economic forecasts that improve the investment thinking and strategic decisions of financial institutions, banks and corporations worldwide. Their research is based on monetary dynamics: analysis of trends in money and credit, banking systems provide unique insights into economic developments and movements of financial asset prices.

For more information see their About Page.