Last week, I discussed the primary issue that has led to the “Unavoidable Pension Crisis” in America. To wit:

“Using faulty assumptions is the lynchpin to the inability to meet future obligations. By over-estimating returns, it has artificially inflated future pension values and reduced the required contribution amounts by individuals and governments paying into the pension system.”

This is a critically important point to understand. Why? Because you may well be in the same “quicksand” as pension funds and just don’t realize it.

For years, Wall Street has continued to espouse the “myth of compounded average returns.” This is the same myth which has not only infected pension funds, but has led to the same false sense of future financial security in personal retirement planning nationwide. An article from IBD last week further perpetuates this myth:

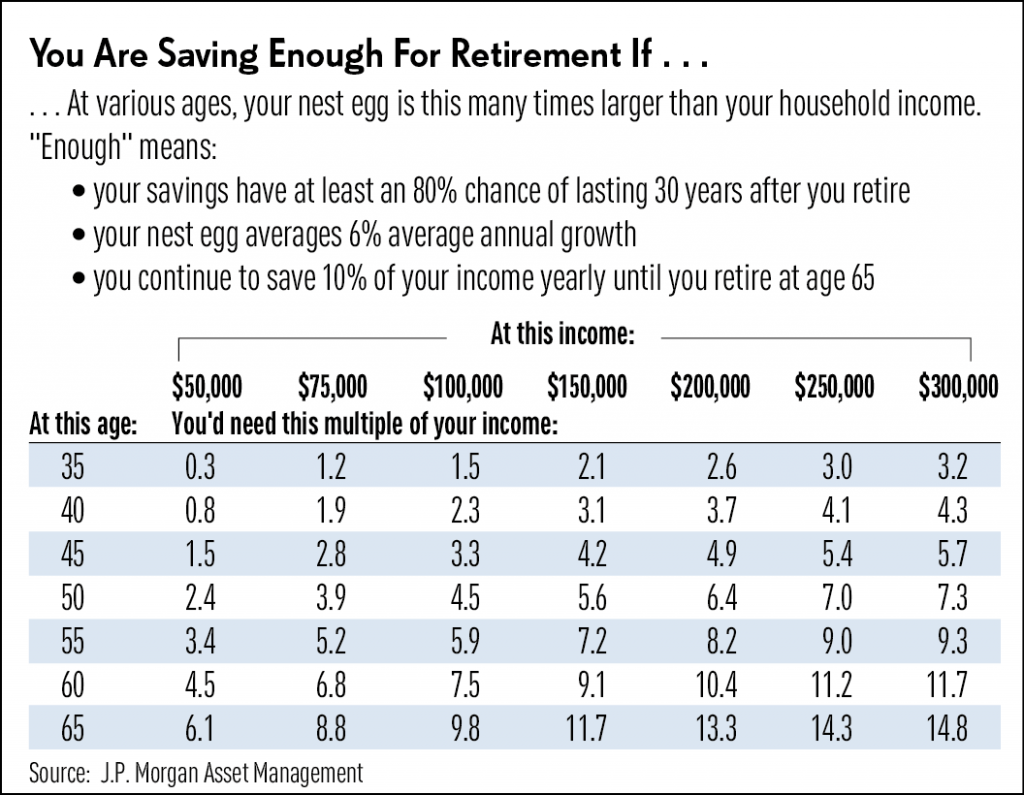

“What determines how much savings is enough by a certain age, with a particular income?

J.P. Morgan says ‘enough’ means the nest egg is big enough to have at least an 80% chance of surviving 30 years in retirement.’ So, 20% of the time you’d need to course correct — by boosting something like your savings rate or cutting your retirement spending — to avoid running out of money in the long run. But 80% of the time, you would not need to make any changes to avoid running out of money.’

The financial firm’s number crunchers also assume that, before retirement, you keep kicking in 10% of your income each year to your nest egg. In addition, they assume that your retirement portfolio grows an average of 6% a year before retirement and 5% a year in retirement.“

And there it is. The biggest mistake you are making in your retirement planning by buying into the “myth” that markets “compound returns” over time.

They don’t. They never have. They never will.

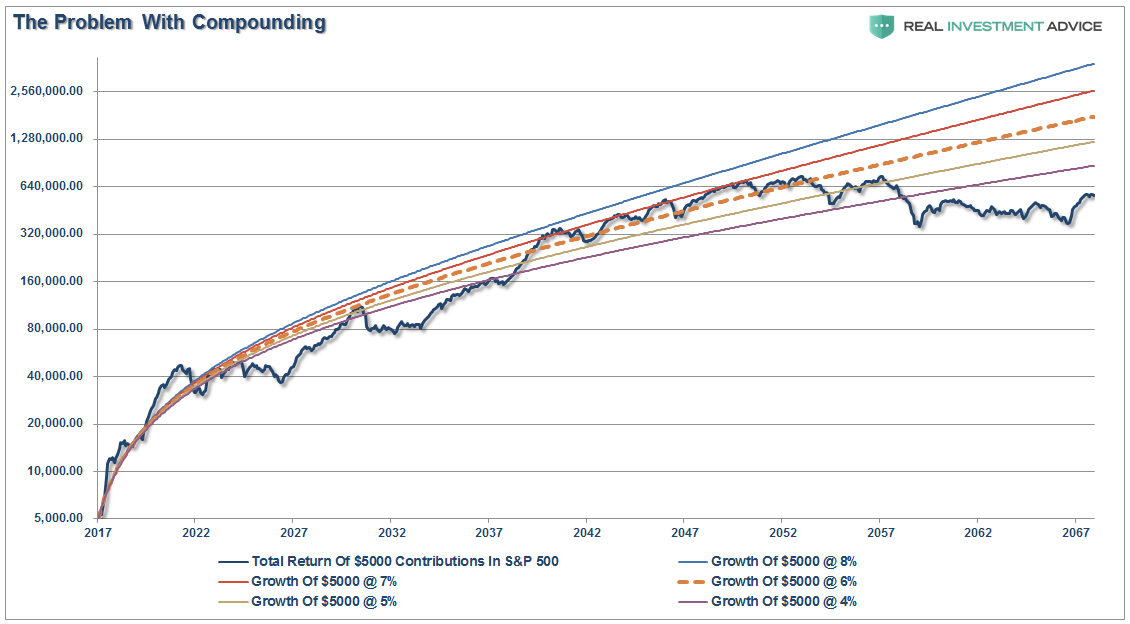

I have adjusted the chart I showed you last week to show a compound return rate of 6%, $5000 annual, made monthly, contributions (10% of $50,000 which is roughly the median wage) and using variable rates of return from current valuation levels. (Chart assumes 35 years of age to start saving and expiring at 85)

As you can see, markets do not compound average returns over time.

Most importantly, just as with “pension funds,” the issue of using above average rates of return into the future suggests one can “save less” today because the “growth” will make up for the difference.

Unfortunately, it just doesn’t work that way.

But there is more to this equation that is not being discussed.

The Missing Ingredients

But there is another problem that is overlooked by IBD in their analysis above. The impact of taxes and fees during the drawdown period (not to mention fees.)

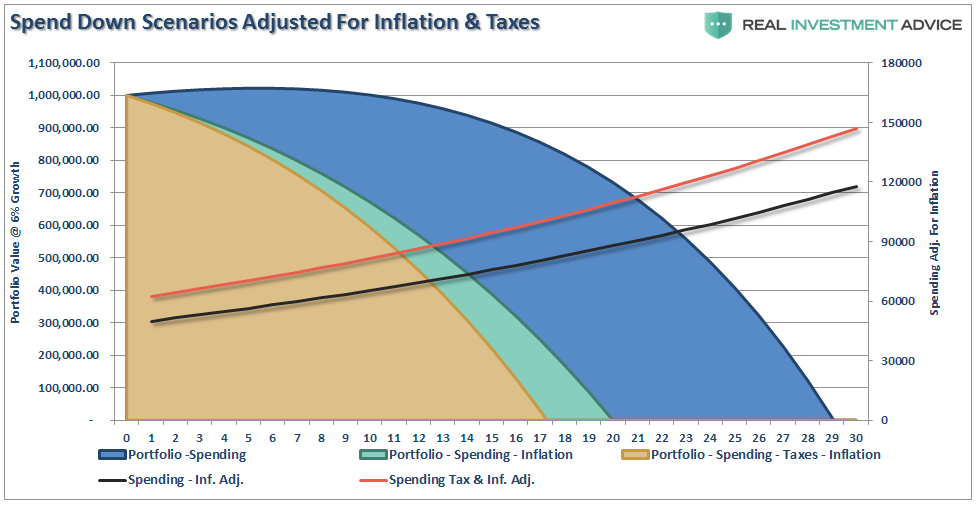

In a report entitled “Retiree’s May Have A Spend Down Problem” I used the follow example:

“For instance, imagine a retiree who has a $1,000,000 balanced portfolio, and wants to plan for a 30-year retirement, where inflation averages 3% and the balanced portfolio averages 8% in the long run. To make the money last for the entire time horizon, the retiree would start out by spending $61,000 initially, and then adjust each subsequent year for inflation, spending down the retirement account balance by the end of the 30th year.”

I have taken that example and adjusted it for a 6% average return and then included scenarios a $50,000 annual withdraw rate adjusted for inflation and taxes.

Unfortunately, once you account for taxes and inflations, the time to depletion accelerates rapidly.

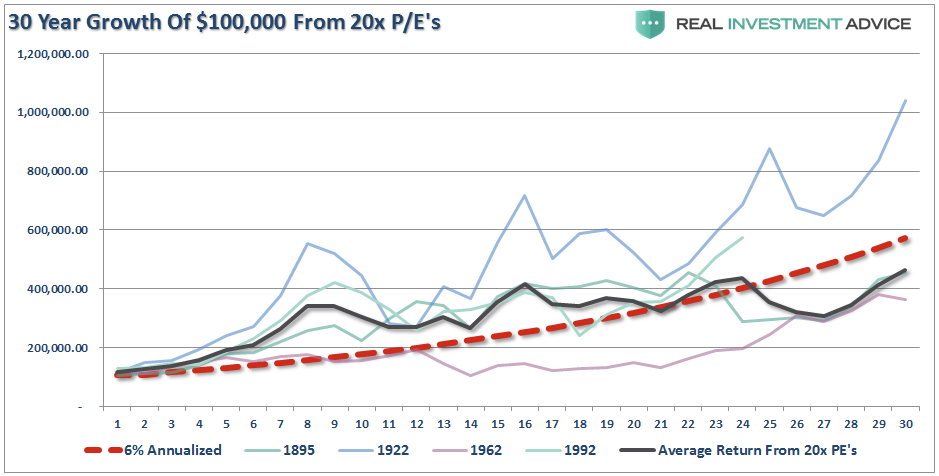

But hold on. It actually gets worse.

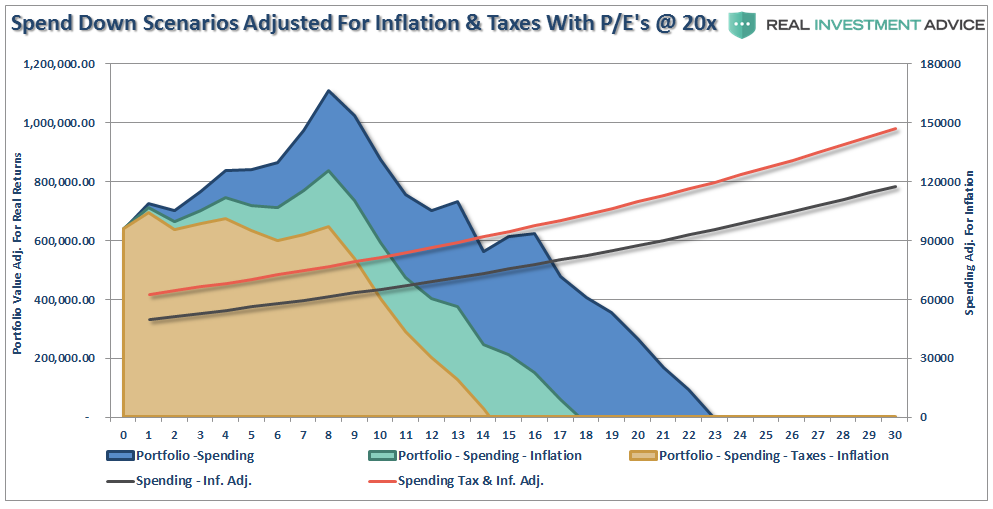

The above example uses the “pension fund” model of 6% compounded annual average returns. Let’s remodel forward returns using the average returns of the markets historically over the subsequent 30-year period from where the index hit 20x valuations. This is shown in the chart below.

If we take the average returns of those years and apply them to our spend down model, as shown above, the depletion rate of retirement savings grows sharply.

The analysis above reveals the important points individuals should consider given current valuation levels and a Fed-driven bull market advance over the last 8-years:

- Expectations for future returns and withdrawal rates should be downwardly adjusted.

- The potential for front-loaded returns going forward is unlikely.

- The impact of taxation must be considered in the planned withdrawal rate.

- Future inflation expectations must be carefully considered.

- Drawdowns from portfolios during declining market environments accelerates the principal bleed. Plans should be made during rising market years to harbor capital for reduced portfolio withdrawals during adverse market conditions.

- The yield chase over the last 8-years, and low interest rate environment, has created an extremely risky environment for retirement income planning. Caution is advised.

- Expectations for compounded annual rates of returns should be dismissed in lieu of plans for variable rates of future returns.

Financial Insecurity – Or, “You Aren’t Saving Enough”

I get it.

Asking people to save “more” really isn’t an option given the recent study published by MarketWatch:

“Some 50% of people is woefully unprepared for a financial emergency, new research finds. Nearly 1 in 5 (19%) Americans have nothing set aside to cover an unexpected emergency, while nearly 1 in 3 (31%) Americans don’t have at least $500 set aside to cover an unexpected emergency expense, according to a survey released Tuesday by HomeServe USA, a home repair service. A separate survey released Monday by insurance company MetLife (NYSE:MET) found that 49% of employees are “concerned, anxious or fearful about their current financial well-being.”

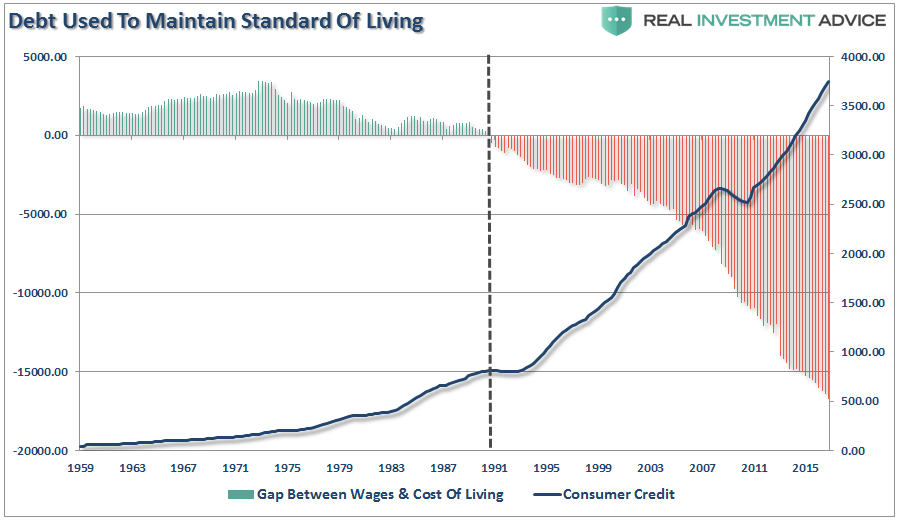

The lack of savings, of course, is directly related to the rising cost of living versus the lack of wage growth over the last 35-years which led to a massive surge in debt to maintain the standard of living.

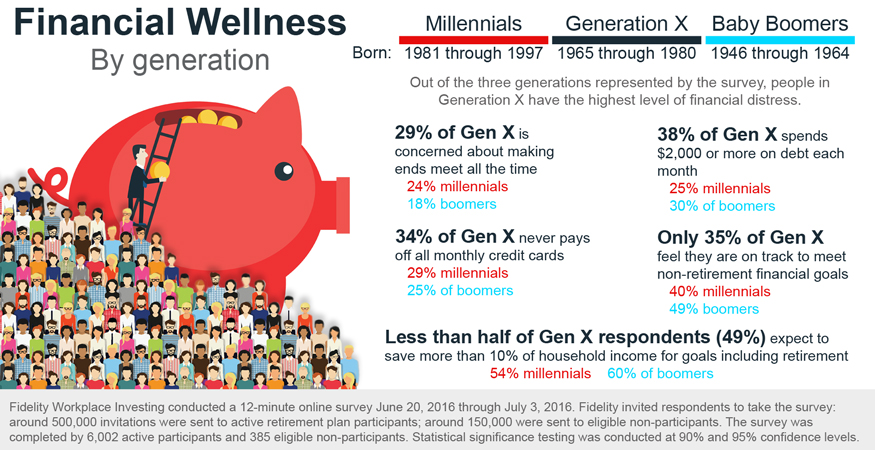

Fidelity provided some further insights into the savings problem for Generation X’ers and Millennials in a recent publication:

“Generation X is squarely in middle age and beset on all sides by bills. Many in Generation X have dependents at home—84% in the survey said they have at least one. They may also still be paying off their own student debts—just more than one in four survey respondents from Generation X says he or she is still paying for his or her own education.

There are all kinds of money problems, but the solutions are generally the same: Save more, spend less, or find a higher-paying job—or maybe all three. But this is easier said than done.”

The massive shortfall in “savings” is going to be a problem in the future given the shortfall that currently exists for a large number of Americans.

You cannot INVEST your way to your retirement goal. As the last decade should have taught you by now, the stock market is not a “get wealthy for retirement” scheme. You cannot continue to under save for your retirement hoping the stock market will make up the difference. As stated, this exactly the same trap that pension funds all across this country have fallen into and are now paying the price for.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you most likely want. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME that was needed to prepare properly for retirement.

Investing for retirement, no matter what age you are, should be done conservatively and cautiously with the goal of outpacing inflation over time. This doesn’t mean that you should never invest in the stock market, it just means that your portfolio should be constructed to deliver a rate of return sufficient to meet your long-term goals with as little risk as possible.

- The only way to ensure you will be adequately prepared for retirement is to “save more and spend less.” It ain’t sexy, but it will absolutely work.

- You Will Be WRONG. The markets cycle, just like the economy, and what goes up will eventually come down. More importantly, the further the markets rise, the bigger the correction will be. RISK does NOT equal return. RISK = How much you will lose when you are wrong, and you will be wrong more often than you think.

- Don’t worry about paying off your house. A paid off house is great, but if you are going into retirement house rich and cash poor you will be in trouble. You don’t pay off your house UNTIL your retirement savings are fully in place and secure.

- In regards to retirement savings – have a large CASH cushion going into retirement. You do not want to be forced to draw OUT of a pool of investments during years where the market is declining. This compounds the losses in the portfolio and destroys principal which cannot be replaced.

- Plan for the worst. You should want a happy and secure retirement – so plan for the worst. If you are banking solely on Social Security and a pension plans, what would happen if the pension was cut? Corporate bankruptcies happen all the time and to companies that most never expected. By planning for the worst, anything other outcome means you are in great shape.

Most likely what ever retirement planning you have done, is wrong. Change your assumptions, ask questions and plan for the worst. There is no one more concerned about YOUR money than you and if you don’t take an active interest in your money – why should anyone else?