Ferro Corporation (NYSE:FOE) logged a profit of $16.1 million or 19 cents per share in third-quarter 2018, down roughly 29.6% from a profit of $22.8 million or 27 cents per share a year ago.

Barring one-time items, earnings were 37 cents for the reported quarter, which trailed the Zacks Consensus Estimate of 40 cents.

Ferro’s revenues went up roughly 12.9% year over year to $395.2 million in the quarter, but missed the Zacks Consensus Estimate of $399.8 million.

The top line in the reported quarter was supported by organic and inorganic growth and strong demand in end-markets. Organic sales rose around 7.3% in the quarter on a constant currency basis.

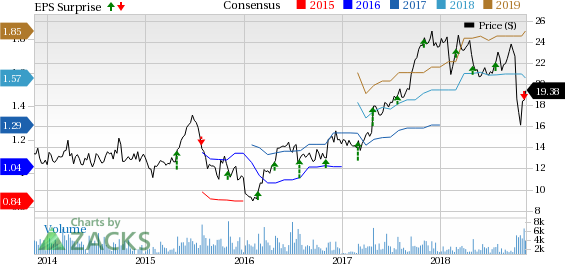

Ferro Corporation Price, Consensus and EPS Surprise

Ferro Corporation Price, Consensus and EPS Surprise | Ferro Corporation Quote

Segment Highlights

Revenues from the Performance Coatings segment rose 20.3% year over year to $175.9 million in the reported quarter. Gross profit for the unit expanded 2.2% year over year to $36.3 million.

The Performance Colors and Glass division raked in sales of $123.3 million, up around 11.5% year over year. Gross profit rose 5.8% year over year to $40.1 million.

Revenues from the Color Solutions unit came in at $95.9 million, up roughly 3% year over year. Gross profit fell 2.8% year over year to $30.2 million.

Financials

Ferro ended the quarter with cash and cash equivalents of around $126.3 million, a more than two-fold year over year increase. Long-term debt was around $923.6 million, up around 37% year over year.

Cash flows from operating activities increased to around $73.4 million in the reported quarter from roughly $20 million a year ago.

The company repurchased shares worth $11 million during the third quarter. Ferro’s board approved a new share buyback program, authorizing the company to repurchase up to an additional $50 million of its outstanding common stock.

Outlook

Moving ahead, Ferro envisions strong demand across its end-markets to continue in the fourth quarter. The company expects adjusted earnings per share and adjusted EBITDA for 2018 to be at the lower end of the guidance ranges of $1.55-$1.60 and $270-$275 million, respectively. Adjusted free cash flow conversion has been forecast at the upper end of the guidance range of 40-45%.

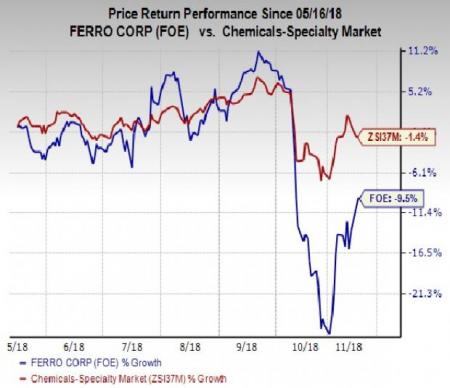

Price Performance

Ferro has underperformed the industry it belongs to over the past six months. The company’s shares have lost around 9.5% over this period compared with the industry’s decline of 1.4% over the same period.

Zacks Rank & Stocks to Consider

Ferro currently carries a Zacks Rank #3 (Hold).

Better-ranked stocks worth considering in the basic materials space include The Mosaic Company (NYSE:MOS) , CF Industries Holdings, Inc. (NYSE:CF) and KMG Chemicals, Inc. (NYSE:KMG) .

Mosaic has expected long-term earnings growth rate of 7% and sports a Zacks Rank #1 (Strong Buy). Its shares have surged 60% in the past year. You can see the complete list of today’s Zacks #1 Rank stocks here.

CF Industries has expected long-term earnings growth rate of 6% and carries a Zacks Rank #1. Its shares have rallied 27% in a year.

KMG Chemicals has expected long-term earnings growth rate of 28.5% and carries a Zacks Rank #2 (Buy). Its shares have shot up 50% in the past year.

Wall Street’s Next Amazon (NASDAQ:AMZN)

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Click for details >>

Ferro Corporation (FOE): Free Stock Analysis Report

KMG Chemicals, Inc. (KMG): Free Stock Analysis Report

The Mosaic Company (MOS): Free Stock Analysis Report

CF Industries Holdings, Inc. (CF): Free Stock Analysis Report

Original post

Zacks Investment Research