The euro zone is struggling with recession, but the news isn’t weighing on the euro these days. Stalemate over budget negotiations in Washington comes to mind as one of the likely if temporary sources of support. It's all about the numbers eventually, but rumor and rhetoric cast long shadows in these strange and troubled times.

The outlook is more complicated for EUR/GBP's ascent, especially with competing ECB and BoE monetary announcements scheduled for Thursday. But it's all about relativity generally, more so than ever until deeper clarity arrives. A clue for deciding what could change, or not, may be slip out in today's update on EU producer price inflation for October.

EU PPI (10:00 GMT) ECB chief Mario Draghi on Friday tried to put a positive spin on the economic outlook with a forecast that "the recovery for the entire euro zone will no doubt begin in the second half of 2013." But the central banker's preference to look down the road was forced to compete with some of the darker news du jour, including a jobless rate for the the core 17 EU nations that pushed higher into record territory: 11.7% in October, up slightly from 11.6% the month before.

Eurostat on Friday also announced in its flash estimate of euro area inflation that pricing pressures are expected to decline to a 2.2% annual rate for November, down from 2.5% in October. Disinflation apparently has some momentum again, a sign the recession across much of Europe isn't easing.

Will today's PPI update show inflation is fading in the industrial sector too? The previous PPI report advised that producer price inflation slowed sharply in September: 0.2% vs. 0.9% for August. But much of the drop was due to lower energy prices. Nonetheless, October's profile is expected to remain flat to down for PPI. Would such news be enough to create headwinds for the euro rally? Not if the reckless game of brinkmanship with the fiscal cliff negotiations in Washington rolls on.

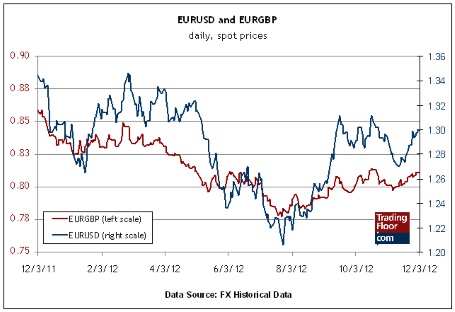

EUR/USD levels: The euro’s rally to the 1.30 mark recently is a run of strength that many analysts thought unlikely just a week ago. The diminished state of eurozone economics relative to the US, after all, looks rather telling. But EUR/USD managed to confound the conventional wisdom. The revival of the euro rests on shaky ground, however, relying in part on the self-destructive sport that passes for politics as usual in the US. News that the pols have agreed on a plan to steer away from the fiscal cliff may still look like a long shot, at least for the immediate future. But if and when a new breed of headline crosses the wires, EUR/USD will have new hurdle (and the same old macro data).

Another catalyst that might change the calculus is the ECB meeting on Thursday. The possibility of a rate cut is considered unlikely, but a surprise revolt by the doves could reshuffle assumptions. True, analysts say Draghi and company will leave the target rate at 0.75%, which looks rich compared with its equivalents at the Federal Reserve (0.25%) and the Bank of England (0.50%). But with the economy under the ECB still reeling as the weakest of the bunch, the case for lower rates in the eurozone isn’t easily dismissed.

Of course, marginal changes in relativity can mean a lot these days. Yesterday’s news that the ISM Manufacturing Index for the US was unexpectedly weak (it fell below the neutral 50 mark in November) reminds that America’s macro edge may not be as strong as it appeared to be in the recent past. EUR/USD & EUR/GBP" title="EUR/USD & EUR/GBP" width="455" height="312">

EUR/USD & EUR/GBP" title="EUR/USD & EUR/GBP" width="455" height="312">

EUR/GBP levels: When Britain broke free of recession recently, courtesy of a rebound in GDP growth in the third quarter, there was a burst of speculation about when, not if, BoE would suspend its bond-buying quantitative easing program that's intent on juicing the economy. The doves, it seems, were given their walking papers. But UK economic news of late has been shaky in spots, which suggests to some that economic activity will weaken in Q4. The numbers to date still aren't enough to inspire thoughts of a new rate cut, but a hike is off the table too.

There’s a thin line between a slower-than-expected recovery vs. another slide into cyclical darkness. Deciding where the UK’s headed will take time. For now, the doves remain on the defensive, if only slightly, when it comes to monetary policy. Adam Posen, a former BoE board member, predicted on Friday that quantitative easing will be put on ice "indefinitely." The reasoning, he explained, has less to do with convincing signs of robust growth in Britain and more about questioning the BoE’s bond-buying program’s efficacy.

Does that still amount to a victory for the hawks? Perhaps, but the BoE will likely leave its target rate unchanged for now, mostly because of inflationary concerns still trump expectations for slower growth in Q4. Keep in mind, too, that EUR/GBP’s rally lacks the zing of the fiscal follies that animates quite a bit of EUR/USD’s recent run. And last we checked, the UK economy was still in better shape than the eurozone. The EUR/GBP’s bulls, it seems, are the more vulnerable of the lot until Washington straightens out its budgetary mess.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Euro Rises Despite Eurozone Recession

Published 12/04/2012, 04:57 AM

Updated 03/19/2019, 04:00 AM

Euro Rises Despite Eurozone Recession

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.