- Eurozone retail numbers remain sluggish

- US jobless data remains upbeat

- Fifth straight rise for private payrolls expected

Today’s hard data on retail sales for the Eurozone will probably remind the markets that growth is still sluggish. Later, US updates on the labour market - initial jobless claims and non-farm payrolls - are likely to boost confidence for the economic outlook in this year’s second half. Keep in mind too that the European Central Bank's monthly interest rate announcement is scheduled for today (11:45 GMT), along with a follow-up press conference 45 minutes later. But most analysts think that today's ECB news will be a non-event in the wake of last month's relatively dramatic announcement of a new phase of monetary stimulus.

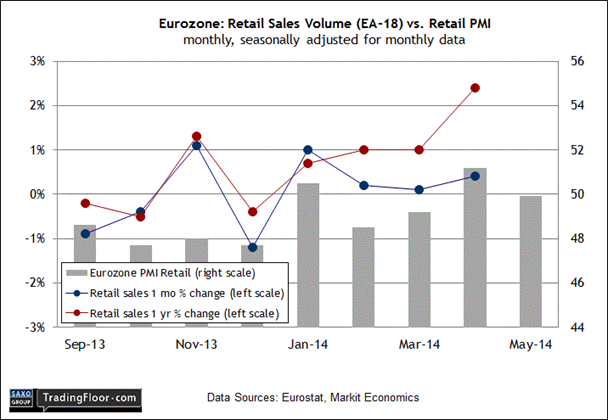

EU: Retail Sales (09:00 GMT) By some accounts there’s an economic recovery in Europe, but if that’s an accurate profile, it’s still reasonable to qualify the observation by recognising that growth remains wobbly at best. This week’s data releases certainly don’t offer any reason to think otherwise. Money supply growth continued to slow in May while private sector bank lending contracted at a faster rate. The jobless rate for Europe ticked down in May, although it remains painfully high at 11.6 percent - nearly twice the level of the US. The cyclically sensitive manufacturing sector in Europe is still expanding, although Markit’s business survey report for June revealed that the growth rate slipped to the slowest pace since last September.

Today’s update on retail spending in the Eurozone for May doesn’t look poised to break free of the sluggish numbers we’ve seen lately. It’s tempting to think otherwise, based on the April report on retail sales, which looked unusually strong. Spending jumped 2.4 percent on a year-on-year basis, or more than twice as much as March’s gain. The improvement was anticipated by the healthy rise in Markit’s Eurozone Retail PMI in April to 51.2 - the first reading above the neutral 50 mark since January. But the subsequent PMI release suggests that the party reversed itself: the Retail PMI slipped below 50 again in May, albeit just barely. That’s not horrible, although it suggests that retail spending is stable at best. That’s a strong clue for projecting that today’s hard data on consumer spending in Europe will soften in May against the previous month.

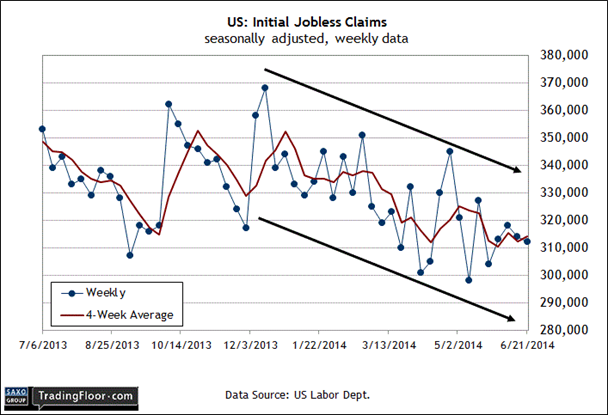

US: Initial Jobless Claims (12:30 GMT) Today’s weekly release on new filings for unemployment benefits will be overshadowed by today’s payrolls report, but both numbers deserve close attention. Indeed, today’s payrolls news is expected to deliver another upbeat profile of the jobs market. One of the factors driving the optimism: the downtrend in new claims.

Applications for jobless benefits have been drifting lower for much of this year. Although the week-to-week changes are noisy, the generally falling trend is distinct, which is a sign that the labour market continues to heal.

In last week’s update, claims fell incrementally, settling at 312,000 on a seasonally adjusted basis. That’s near the recent seven-year low for the week through this year's May 10. The consensus forecast sees a small uptick to 314,000, but if that’s accurate it’s no threat to the widely held view that private payrolls are on track to deliver their fifth straight month of 200,000-plus growth in today’s June release that’s published simultaneously with the claims report.

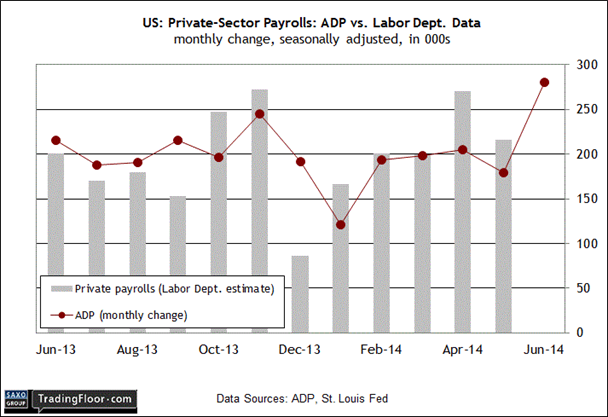

US: Non-farm Payrolls (12:30 GMT) Yesterday’s better-than-expected ADP Employment Report for June suggests that today’s official jobs report from Washington will deliver encouraging news as well. The first round of attention, as usual, goes to the headline number that combines private and government jobs. A slightly better metric is the private-only trend, which does a better job of tracking the business cycle. (Government jobs can rise or fall for non-economic reasons).

With that in mind, what’s the likelihood that today’s private payrolls number will post a substantial improvement in line with ADP’s private sector estimate? The consensus forecast sees a slightly lower increase for June (+213,000) against the previous month (+216,000), according to Econoday.com. The median projection via my econometric modeling anticipates a modestly better gain (+235,000).

All the usual caveats apply, however, in part because the monthly changes in the government’s private payrolls data are twice as volatile versus the ADP figures. That’s a reminder that forecasting tomorrow’s data is even tougher than anticipating the ADP report. That said, economic reports have generally been upbeat lately for the US. At the very least, the odds look good for expecting that we’ll see the fifth straight monthly rise of 200,000 or more for private payrolls. It may still be premature to say that economic growth is accelerating, but today’s release will likely confirm that the spring revival in the macro trend is genuine.