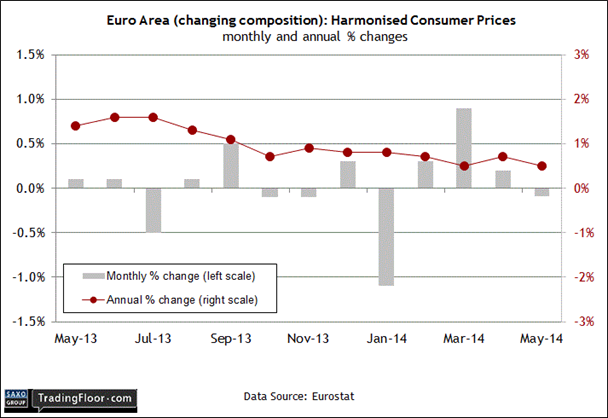

- Prices data lower than expected

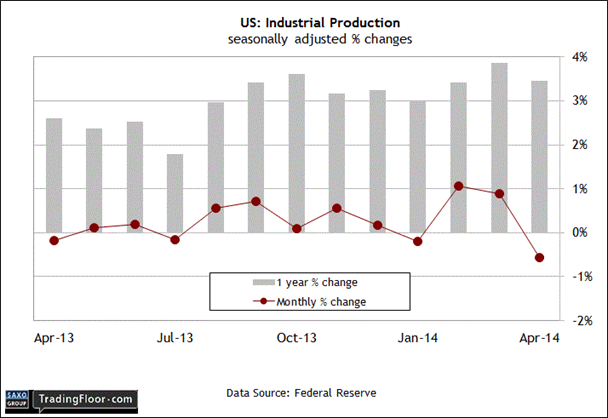

- US Industrial numbers show rebound

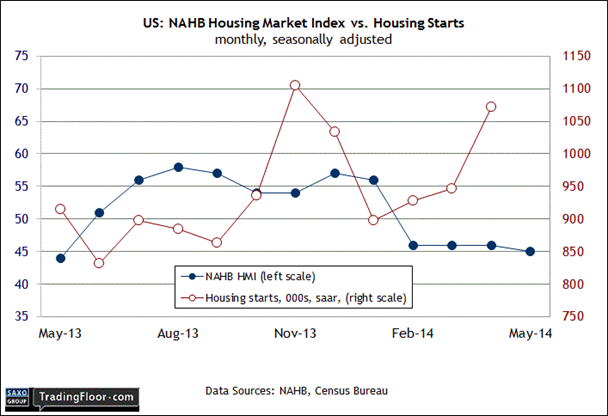

- US housing shows slow but steady rise

Monday tends to be a slow day for economic reports, although the revised numbers on consumer inflation for Europe will draw a crowd. The update for May gives the market a new excuse to reconsider the outlook for deflation risk and the European Central Bank’s new round of monetary stimulus. Later, we’ll see two US numbers that offer a fresh look at the macro trend in the world’s largest economy via the monthly report on industrial production and an update on sentiment in the home building industry.

Eurozone: Consumer Price Inflation (09:00 GMT) Last week’s news that industrial activity rose more than expected in April for the Eurozone boosted confidence that the recovery in Europe will endure after all. In turn, that’s a signal for thinking that the recent run of disinflation isn’t a prelude to outright deflation. Nonetheless, recent updates on consumer prices still look worrisome, if not yet fatal. The annual rate of change slipped to 0.5 percent on a year-over-year basis in the flash estimate of the consumer price index (CPI) for May. That’s well below the European Central Bank’s roughly 2 percent target and so the news sends a strong warning that deeper macro troubles await if growth doesn't accelerate or at least stabilise.

The central bank responded earlier this month with another phase of monetary stimulus. The upbeat figures on industrial production suggest that the worst may have passed for Europe’s macro trend overall. That’s also the message in the May update of the Markit Eurozone Composite Purchasing Managers Index (PMI). Although this benchmark ticked down to 53.5 last month - comfortably above the neutral 50 level - that’s only slightly below April’s three-year high. The retail PMI data for the Eurozone is still more or less flat, but at least it’s steady. Germany, however, is still the primary source of support and so there's still an open debate about the trend with consumer demand beyond Europe’s main economy.

Today’s revised inflation numbers for May aren’t expected to change relative to the flash estimate. The real test will come next month, with the June CPI data, by which time we’ll have more macro reports to consider. For now, Europe still faces plenty of risks, but the first hurdle is deciding if inflation is stabilising. The answer will take time, but it starts with today’s revision.

US: Industrial Production (13:15 GMT) Industrial activity suffered an unexpected slide in April, but today’s report for May is expected to reflect a rebound. It all looks noise when viewed through the prism of the year-over-year trend. Industrial production advanced 3.5 percent in April against a year ago. That’s down from March’s 3.9 percent rise, although the increase is still is more or less average for the 12-month changes we've seen since last summer. In other words, industrial activity is rising at a moderate rate, which is in line with recent history.

The consensus forecast calls for more of the same: economists project a 0.5 percent rise for industrial output in May against the previous month, which translates into a respectable 3.9 percent increase for the year-over-year rate. Recent updates from other corners of the economy offer no reason to question the prediction. Notably, the labour market is still growing at a healthy 2 percent rate, which is also in line with recent history and strong enough to keep forward momentum intact. The rise in payrolls implies macro growth of 2-3 percent generally. That’s not exciting, and it falls short of arguing that the US is poised for a strong phase of expansion. But the growth has been steady, and that’s encouraging. Today’s news on the industrial sector isn’t likely to tell us otherwise.

US: NAHB Housing Market Index (14:00 GMT) The real estate market still looks wobbly, but there are growing signs that it’s stabilising. Exhibit A is the mood in the home building industry. The National Association of Home Builders/Wells Fargo Housing Market Index (HMI) has been treading water lately, at just below the neutral 50 level.

“After four months in which the HMI has shown little signs of fluctuation, it is clear that builder sentiment is becoming more in line with the market reality of a continuing but modest recovery,” noted NAHB’s chairman in last month’s update. He added that “builders expressed some optimism that sales will pick up in the coming months” in the May survey.

There’s a good case for expecting improvement in demand for housing when you consider the relatively steady annual growth in payrolls and the latest improvement in the net worth of households. For the 12 months through this year’s first quarter, household net worth jumped more than 10 percent. Meantime, household debt remained flat, as it has since the end of the Great Recession. At the same time, residential property values have climbed. Reviewing the per capita data also shows improvement, with levels climbing above the previous high in 2006.

Combined with the ongoing annual increase in payrolls, it all adds up to a favorable backdrop for housing. Today’s HMI update may still reflect a cautious outlook among home builders, but the generally favorable macro wind for the real estate market will probably keep this sentiment index from falling any further. In fact, the crowd's looking for a slight improvement: the consensus forecast sees HMI inching higher to 47, or up slightly from 45 in the previous release.