Following the rocky end to 2011, the start of the current year has seen a relief rally across the spectrum in the EMEA FX universe, while the implied option volatilities have eased considerably. Below, we look at three particular EMEA currencies: the Turkish lira, the Polish zloty and the Russian rouble, where we believe there is good potential for further gains.

Czech and Romanian central banks taking the stage next week

We have two rate decisions coming up next week – in the Czech Republic and in Romania. Growth in the Czech economy remains very subdued and in our view it is impossible to see any inflationary pressures from the demand side of the economy. In fact, our own measure of “demand inflation” (the inflation resulting from monetary conditions) has remained deflationary since 2009. As a consequence we would argue that monetary easing is more warranted than monetary tightening.

Romania, on the other hand, has been somewhat of a star performer in terms of fulfilling the conditions for the country’s standby agreement with the IMF and in terms of fundamentals there clearly have been improvements over the past couple of years.

However, the economy is basically not growing and the combination of austerity

measures and the European crisis is certainly not helping in that sense.

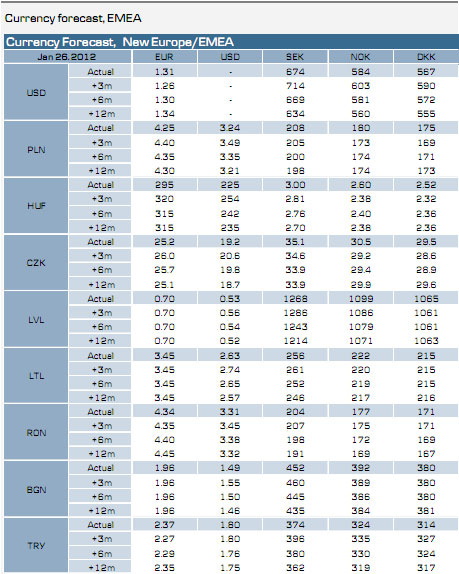

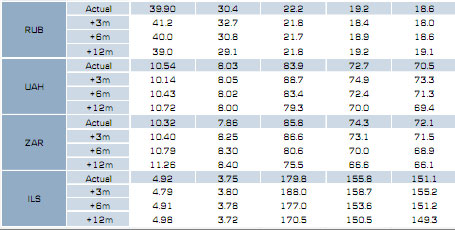

EMEA FX : Where to put your money

Following the rocky end to 2011, the start of the current year has seen a relief rally across the spectrum in the EMEA FX universe, while the implied option volatilities have eased considerably. Below, we look at three particular EMEA currencies: the Turkish lira, the Polish zloty and the Russian rouble, where we believe there is good potential for further gains.

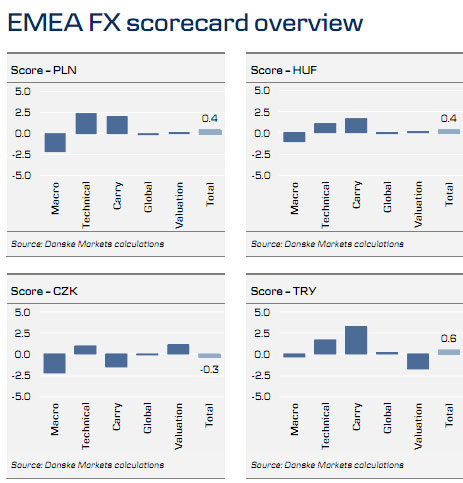

Going into 2012 we had highlighted the upside potential of both the lira as well as the zloty in our FX Top Trades 2012 published on 14 December 2011. While both of these trades have so far performed very well – in particular with the zloty advancing around 7% over sterling since the inception of the strategy– we continue to believe that there is further scope for additional gains.

USD/TRY is already down by around 7% from the all-time record highs hit at the very end of 2011, while the lira has advanced against the euro since the start of the year also in the same range. On the monetary policy front, the Turkish central bank’s (TCMB) latest rate decision delivered no surprises. While the TCMB remains cautious in its stance and looks to retain a good dose of flexibility, the overall bias is still hawkish as headline inflation is now in double-digit territory and looks set to remain elevated in Q1 12. While

we expect lira trading conditions to remain volatile and for this volatility to be

particularly high on the rates markets, our base scenario of Turkey avoiding a hard landing concurrently with external imbalances gradually correcting paints an overall lira supportive picture in 2012.

The Polish zloty has rallied over 7% since mid-December against the union currency, with EUR/PLN recently breaking below the key 4.30 mark. Given its comparatively good growth dynamics and the determined fiscally tighter stance of the Polish government post the elections in October, the zloty has been hit surprisingly and perhaps disproportionately hard by the ongoing European crisis.

While the latest rally has taken the zloty closer to levels we would consider

fundamentally fair, we believe there remains good scope for further appreciation. A slightly less dovish stance from the NBP going forward combined with a decent growth outlook bode well for the zloty. Furthermore, the cautious return of investor confidence to the Hungarian markets with growing signs of the Hungarian government relenting on key issues that had led to the downgrade debt rating to junk status by all three major rating agencies, is also having a positive spill over effect on the Polish markets. We remain somewhat critical of these developments and await more concrete signs of a decisive

turnaround in Hungarian interventionist policies. But given the encouraging

developments, we would look to play them out in the zloty markets, rather than directly in forint crossings.

The rouble, for its part, has depreciated during the past months mostly due to the increase in global risk aversion. In addition to that, political risks have risen in Russia starting from the December parliamentary elections and during Q1 12 political uncertainty is likely to keep the rouble under pressure. However, the political risks are currently overemphasised, in our view and strong economic fundamentals in Russia are being ignored. Thus, we expect the rouble to strengthen during the last three quarters of 2012.

In particular, we expect oil prices to remain elevated and even rise during 2012. In addition to that, capital outflows are likely to moderate starting in Q2 due to expected results from the presidential elections in March and the finalised WTO membership.

Moreover, domestic demand is likely to remain strong in Russia while inflation is

historically low. The main risk for the rouble obviously lies in the oil price, as Russia’s strong current account is fully dependent on energy exports.

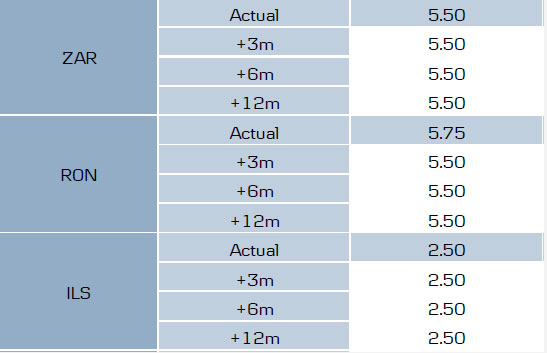

EMEA Fixed Income Update

We have two rate decisions coming up next week – in the Czech Republic and in Romania.

Growth in the Czech economy remains very subdued and in our view it is impossible to see any inflationary pressures from the demand side of the economy. In fact our own measure of “demand inflation” (the inflation resulting from monetary conditions) has remained deflationary since 2009. As a consequence we would argue that monetary easing is more warranted than monetary tightening.

However, a number of Czech monetary policy makers seem to think that there is a need for monetary tightening rather than easing. We are quite puzzled by this – even more so when taking into account that headline inflation remains just around the Czech central bank’s inflation target of 2%. Despite some policy makers calling for rate hikes we expect the majority of the CNB board to remain in favour of unchanged interest rates at next week’s rate setting meeting. This is also the consensus expectation.

Romania has been somewhat of a star performer in terms of fulfilling the conditions for the country’s standby agreement with the IMF and in terms of fundamentals there clearly have been improvements over the past couple of years. However, the economy is basically not growing and the combination of austerity measures and the European crisis is certainly not helping in that sense.

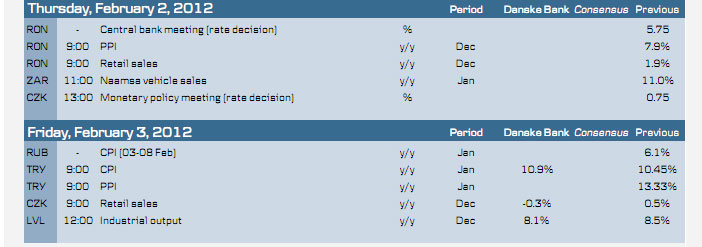

Lately we have seen demonstrations against the government across Romania, which have occasionally turned rather violent. There is no doubt that the Romanian central bank is well aware of the very weak growth in the Romanian economy and at the last rate decision in early January the central bank decided to cut its key policy rate by 25bp. We expect an additional 25bp cut at next week’s rate setting meeting.

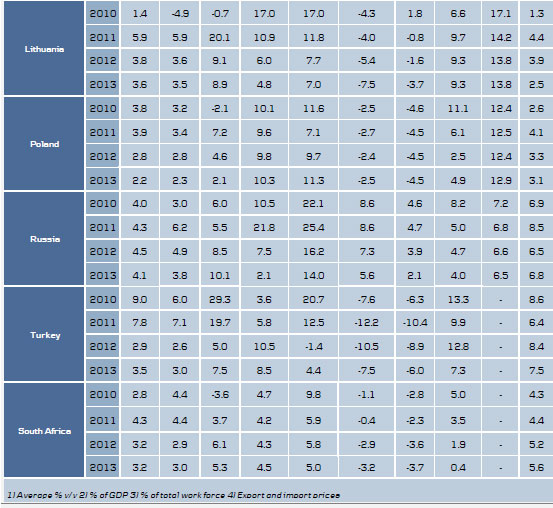

Baltic macro update

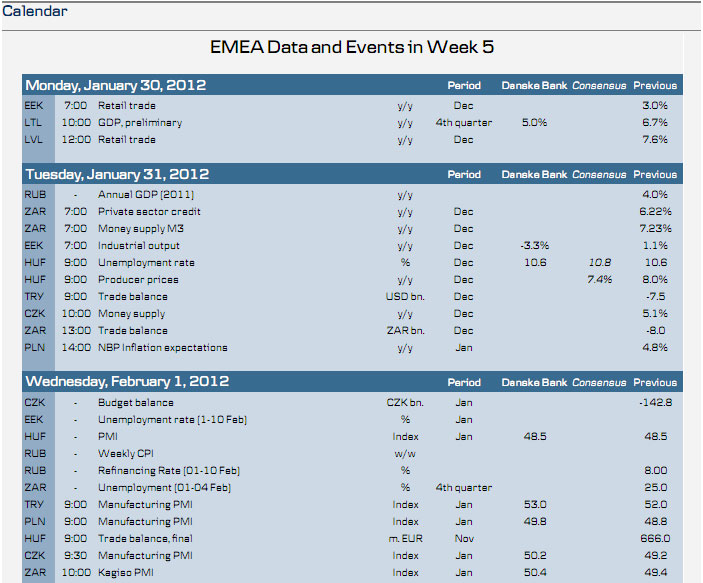

Next week we will be seeing the GDP flash estimate from Lithuania and industrial production for the other two Baltic countries. Below we cover each of the Baltic countries and their respective indicators. We expect Lithuanian GDP growth in Q4 11 to have decelerated only marginally to 5% y/y, down from 6.7% y/y in Q3 11. This would constitute 6% growth on average for the whole year. Due to a less favourable assessment of global trends and the increased risk in financial markets, Lithuanian economic development could slow to 2.7 % y/y on average this year.

We expect that the rise in Estonian industrial production (IP) will have slowed further and that December 2011 IP will have entered negative territory with a decline of 3.3% y/y.

These trends are determined by a negative base effect and slowdown in key Estonian export markets. We also expect Latvian IP growth in December to have slowed but not so significantly, to 8.1% y/y down from 8.5% in November.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Emerging Markets FX Ship Opens its Sails

Published 01/30/2012, 08:43 AM

Updated 05/14/2017, 06:45 AM

Emerging Markets FX Ship Opens its Sails

EMEA FX: Where to put your money

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.