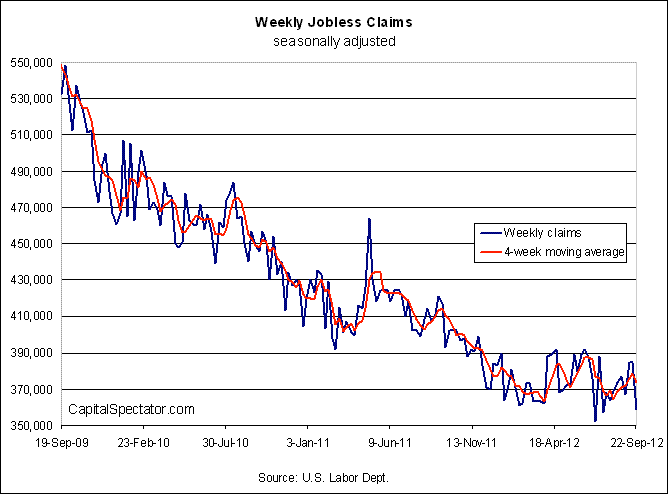

There’s good news and bad news in today’s economic reports. In the labor market, initial jobless claims dropped a hefty 26,000 last week -- the biggest weekly decline since July -- to a seasonally adjusted 359,000. That leaves new filings for unemployment benefits close to the post-recession low of 352,000 from the week ending July 7. But this encouraging news is marred by a steep drop in durable goods order for August. Does one data set trump the other? That’s to be determined in the weeks ahead as more numbers roll in. Meantime, there are two newly minted data points to consider, each one contradicting the other in rather stark terms. The macro truth will out, and probably quite soon. Meantime, today's menu of statistics offer a choice: darkness or light.

Looking Back On Claims

Choose wisely, grasshopper or, perhaps, not at all. At least not just yet. For perspective, let’s review how jobless claims stack up in recent history. As the first chart shows, last week’s substantial decline in new claims looks fairly decisive in terms of breaking the recent trend of moving sideways or inching higher. One week of data for this series doesn’t mean much, of course, but for the moment the case for optimism is a bit stronger.

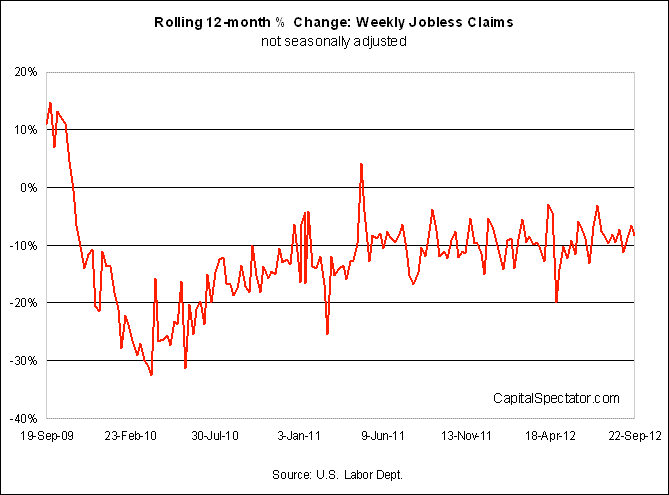

Actually, one could reasonably argue that nothing much has changed for the trend in jobless claims, last week’s data point notwithstanding. As I regularly advise, the clearer analysis of jobless claims -- an unusually noisy data set -- typically arises from looking at year-over-year changes before seasonal adjustment. By that standard, the news is relatively upbeat, as it has been for most of the past 12 months, namely: claims continue to fall by roughly 10% a year. If and when the annual pace starts rising on a consistent basis vs. year-ago levels, we’ll have a dark signal to consider for the business cycle. At the moment, however, we’re nowhere near that turning point, which is to say that the labor market continues to heal, albeit slowly.

Can't Sugarcoat Durable Goods

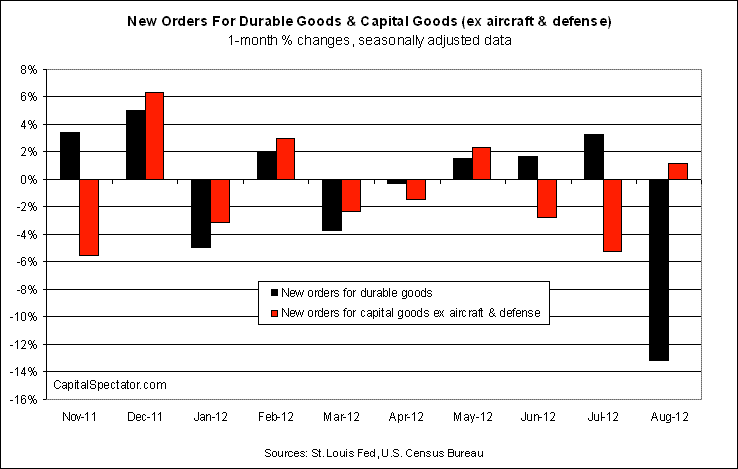

But all this happy talk is tarnished with the news that new orders for durable goods dropped 13.2% last month -- the biggest monthly decline since January 2009, when the recession’s fury was still raging. There’s no way to sugarcoat this tumble, although it’s worth pointing out that most of the drop is due to the volatile transport industry. Durable goods orders ex-transport was still down last month, but by a considerably milder 1.6% fall.

Take note too that capital goods orders -- a.k.a. business investment, or new durable goods orders less defense and aircraft -- actually rose in August, climbing a moderate 1.2%. That's the first monthly gain since May. Hmmm.

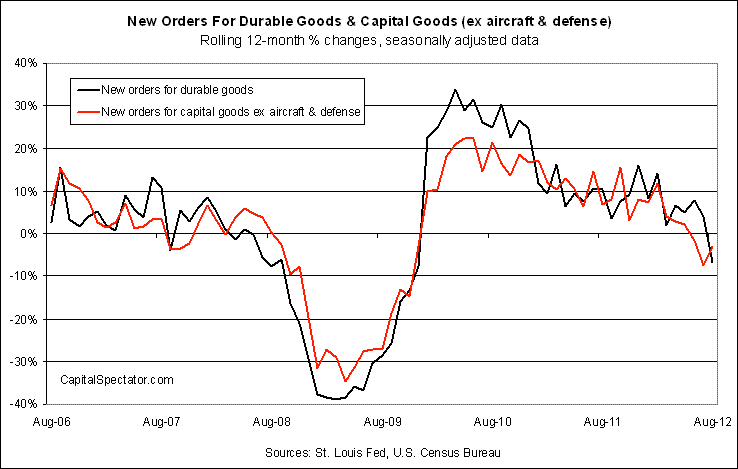

But there’s no getting around the fact that the trend in new orders has turned negative. As the next chart shows, demand for durable goods is shrinking -- for both the top line measure and for capital goods. That hasn’t happened in more than two years. It doesn’t help that today’s third revision of third-quarter real GDP fell to an annualized 1.3% rate, or down from the previous estimate of 1.7%. The slow recovery just got slower in broad terms, according to official numbers.

The Critical Question

Will the weakness in durable goods orders spill over into the rest of the economy? Or is the drop in this series just short-term noise? It’s folly to dismiss the risk that today's numbers imply, but it’s also premature to conclude that the business cycle’s fate has been sealed. We’ll need to see more darkness in more data sets before issuing a call to man the cyclical lifeboats and evacuate the passengers. But the possibility of rough seas and worse looks somewhat more plausible -- particularly if you ignore the jobless claims data, and quite a bit of the other numbers that collectively add up to the U.S. economy.

Nonetheless, we seem to be at another critical juncture. It's possible that we're being misled by the short-term noise. It wouldn't be the first time, and so it's important to maintain objectivity by looking at a broad cross section of the numbers. On that note, tomorrow we learn how personal income and spending fared in August. Once those numbers arrive, I'll update the Capital Spectator's Economic Trend Index and GDP nowcast for a fresh benchmark for evaluating how the outlook has changed. Stay tuned…

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Contradiction Du Jour: Durable Goods vs. Jobless Claims

Published 09/27/2012, 10:28 AM

Updated 07/09/2023, 06:31 AM

Contradiction Du Jour: Durable Goods vs. Jobless Claims

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.