This year was always going to be about central banks and their interest rate decisions. So far, no asset class can be disappointed, because tagging along with central bank decisions is volatility, a word that could 'not' be applied to the forex market over the past 18-months. With mirrored monetary policies central banks had managed to handcuff the forex market, deadening volatility and opportunity. So far in 2014 that's all changed, volatility is back with a vengeance, bringing with it trading opportunities. There never was going do be a "follow thy leader campaign" – that has been done. Rate divergence is the name of the new game and the "mighty" dollar is expected to benefit greatly from it before this year is out.

USD/TRY" title="USD/TRY" align="bottom" border="0" height="200" width="300">

USD/TRY" title="USD/TRY" align="bottom" border="0" height="200" width="300">

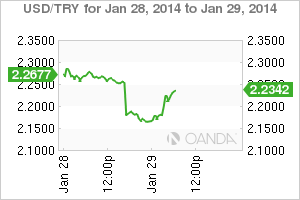

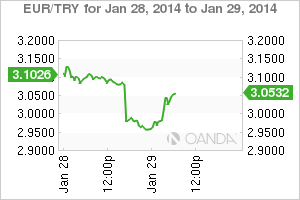

The knock on effect from the Emerging Markets fallout is making it interesting for capital markets. EM currencies, including the Argentina's peso (ARS) and India's rupee (INR), have been under pressure from expectations that the Fed and the Bank of England would pull back on their stimulus measures. Previously, developed QE had been driving "inflows" to developing economies, which in turn financed their aggressive growth leading to an obvious side effect - inflation. EM central banks need to be belligerent when combatting rampant inflation and Turkey's CBRT aggressive actions overnight certainly follow that mantra. The CBRT raised their overnight lending rate by +425 bps from +7.75% to +12%. Turkey now joins India (last night) and Brazil (2-weeks ago) with a more aggressive than expected policy tightening, pledging to maintain tight monetary policy until there is a clear improvement in the inflation outlook. EUR/TRY" title="EUR/TRY" align="bottom" border="0" height="200" width="300">

EUR/TRY" title="EUR/TRY" align="bottom" border="0" height="200" width="300">

Is Turkey's proactive central bank measure to curb inflation and prevent disorderly outflows going to be short lived? Watching the JPY and CHF back in demand during this mornings Euro session would suggest the safe haven play is currently dominating. This is in contrast to the increased risk taking that transpired throughout the Asian session overnight. The TRY is in danger of wiping out its post-rate hike gains. USD/TRY fell from around 2.25 to 2.1635 in the wake of the central bank action and is now back up to 2.23. However, if the market believes that the CBRT has now gotten ahead of the curve and ready to deploy all their tools to fight inflation should be capable of restoring some further TRY confidence. Investors can expect global policy makers to collectively talk up the EM region as well. Obviously the downside to the CBRT actions is that being too aggressive does create potential problem for domestic economic growth, and can put pressure on Turkish bonds and equities.

EUR/USD" title="EUR/USD" align="bottom" border="0" height="200" width="300">

EUR/USD" title="EUR/USD" align="bottom" border="0" height="200" width="300">

Turkey's aggressive hike is good for markets, but if the Fed hiked it would be deemed detrimental. The Fed is now in focus and consensus believes that a CBRT rate hike will do nothing to sway US policy makers later this afternoon. Even yesterday's dismal US durable goods headline (-4.3%) is not expected to distract anyone at the Fed. US policy makers are on course to follow through with tapering their monthly asset purchase at a "measured pace." Last month a token taper of $10 billion was initiated and there is no evidence to suggest that Ben and company will be deviating from their game plan this afternoon. The December durable goods report was much weaker than expected almost across the board and the prior November numbers were all revised lower. Last months shortfall was broad-based and the biggest drop in five-months.

USD/JPY" title="USD/JPY" align="bottom" border="0" height="200" width="300">

USD/JPY" title="USD/JPY" align="bottom" border="0" height="200" width="300">

The fixed income dealers are beginning to lean on the supply factor argument on tapering. Dealers are maintaining that the Fed needs to taper because the Treasury is tapering. With the US budget deficit narrowing there has been a drop off in debt product supply at some note auctions of late. On the flipside, less product supply is managing to artificially keep treasury yields in check, especially after last years pop in yields. Combine this with China and Japans record holding of US treasuries will continue to benefit both the US consumer and businesses by keeping interest rates at agreeable levels.

GBP/USD" title="GBP/USD" align="bottom" border="0" height="200" width="300">

GBP/USD" title="GBP/USD" align="bottom" border="0" height="200" width="300">

Yesterday's soft durable report was immediately followed up by the Conference Boards bullish consumer confidence headline (80.6). It seems that the US consumers are beginning this New Year feeling a bit better about their own economy. Even the present situation index (consumers' assessment of current economic conditions) rose to 79.1 from 76.2. This is further proof that the US consumer confidence is back on track, which could suggest that the US economy may actually pick up some momentum in H1. Even the board's survey on current labor conditions is more upbeat than what actually transpired in the last NFP report (+74k vs. the markets +200k expectations).

USD/CHF" title="USD/CHF" align="bottom" border="0" height="200" width="300">

USD/CHF" title="USD/CHF" align="bottom" border="0" height="200" width="300">

Helicopter Ben will be overseeing his last meeting of the Fed. Very little is a forgone conclusion nowadays, but the market expects the bank to continue tapering its monthly purchase program. Even last months weaker than projected job report is not expected to have any effect on the decision. Analysts have been quick to write off the weather influenced dismal print as just another polar vortex blip. Many have predicted the USD to benefit from the taper, but so far, it is only apparent in relation to commodity currencies. Throw in more EM mayhem and the color of US green looks even more attractive.