Yelp Inc (NYSE:YELP) posted disappointing first quarter earnings on April 29, falling short on revenue estimates and posting slowed user growth for the second consecutive quarter. The report sent shares down about 16% after it was released.

Yelp posted quarterly revenue of $118.5 million, marking a 55% year-over-year increase though missing analysts’ estimates of $120 million. Revenue derived from advertising increased 51% year-over-year to $98.6 million, making up the majority of Yelp’s total revenue. Yelp posted a net loss of ($0.02) per share, slightly wider than the analyst consensus of ($0.01) per share. However, this was a narrower loss compared to ($0.04) posted in the same quarter last year.

Investors are wary of slowed growth rates on the website. Yelp posted an 8% year-over-year increase in average monthly unique visitors, though this marks slowed growth as this metric increased 30% a year prior and increased 13% in the previous quarter.

Yelp acquired Eat24, a food delivery platform, as a way to increase daily consumer engagement on Yelp.

Looking forward, Yelp expects to post second quarter revenue between $131 million and $134 million, which would be an approximate 49% year-over-year increase. For the full-year 2015, Yelp expects to post net revenue between $574 million and $579 million, which would be an approximate 53% year-over-year increase. This outlook falls on the low side of analysts’ expectations.

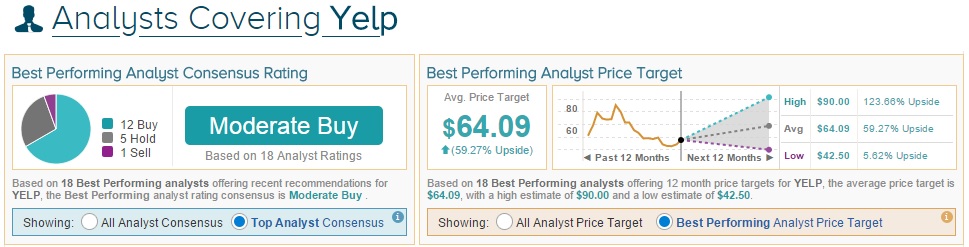

Analysts issued varying ratings following Yelp’s report.

Robert Peck of SunTrust maintained a Buy rating on Yelp though reduced his price target from $70 to $52. Peck attributed the revenue miss to currency headwinds. He added that Yelp’s full-year guidance implies “growth reacceleration” in the second half of the year driven by “continued bolstering of the sales force and CPC offerings (Local), launch of mobile programmatic (Brand), Eat24 (Other), and ramp of marketing spend.” Peck believes Yelp has a “strong core” and opportunities in the international market, Eat24, and SeatMe.

Robert Peck has a 60% overall success rate recommending stocks with a +14.7% average return per rating.

Separately, Mark Mahaney of RBC Capital downgraded Yelp following the report from Outperform to Sector Perfom and lowered his price target from $82 to $50. Mahaney upgraded the stock “almost a year ago” when the stock was experiencing a “major pullback,” but he now admits his call did not pan out and he does not “have confidence that it will from here either.” He continued, “We still view YELP as a top-of-funnel, strong-brand unique asset with downstream transaction capability. But that transaction capability could take a long time to play out… We still see strategic value to YELP, but that by itself isn’t enough to keep us from moving to the sidelines.”

Mark Mahaney has a 68% overall success rate recommending stocks with a +23.8% average return per rating.

After the earnings report, analyst Darren Aftahi of Northland Securities downgraded Yelp from Market Perform to Underperform and lowered his price target from $49 to $35. After Yelp’s weak guidance and underperformance in the quarter, Aftahi commented that “continued decelerating y/y growth in its overall user base continues to give [him] pause.” Although mobile app users increased this quarter, “overall mobile users continue to show deceleration.” Aftahi concluded, “Downside risk remains meaningful… with an ever increasing competitive landscape.”

Darren Aftahi has a 57% overall success rate of 57% and an average loss of -1.1% per recommendation.

On average, the top analyst consensus for Yelp on TipRanks is Moderate Buy.