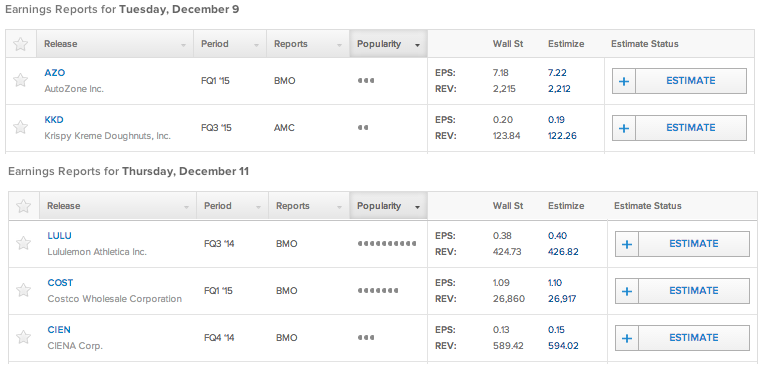

Tuesday - AutoZone

Auto parts retailer AutoZone Inc (NYSE:AZO) is set to report Tuesday before the opening bell. Last quarter AutoZone reported an 8% gain in year over year (yoy) earnings per share and a minor drop in total revenue.

Earnings at AutoZone have been growing by a YoY average of 16% each quarter over the past 2 years. In the second quarter of this year that rate of expanson dropped to 8%, it’s lowest reported value in 24 months.

After a brief tumble leading into last quarter’s earnings release date AutoZone stock has picked up steam, climbing 17% since the last report. AutoZone has a history of reporting within a relatively tight range compared to estimates and Tuesday analysts on Estimize are executing AutoZone to get back to it’s winning ways by reporting 15% EPS growth.

Tuesday - Krispy Kreme Doughnuts

The huge trend supporting organic and healthy food options at the expensive of fast food joints continued rolling on Monday. McDonald’s reported an awful sales figure, disclosing that same store sales sank 4.6% in November. Although secular forces appear to be lined against of Krispy Kreme (NYSE:KKD), sales at the glazed doughnut company have been holding up just fine in recent months.

Last quarter Krispy Kreme saw its revenue climb 7%. However, results on the bottom line did not shimmer the same way that sales did. Krispy Kreme’s EPS dropped by 7% last period. In last quarter’s press release CEO Tony Thompson commented that the top line revenue growth was spurred by promotions and increased spending on marketing. Domestic same store sales were up 2.8% and the overall store count rose 3.4% last quarter.

Tuesday analysts on Estimize are looking for Krispy Kreme to improve its margin blues and report a15% EPS increase alongside a 6% hike in total sales.

Wednesday - Lululemon

(Graph above from ChartIQ Visual Earnings)

Since early June 2013 shares of Lululemon (NASDAQ:LULU) have been trending lower. Revenue growth has fallen between a moderate range landing between 7% and 37% each quarter within the past 2 years. This quarter Estimize contributors are looking for $427 million in revenue, or slightly more than a 12% yoy gain. That would be just under last quarter’s 13% sales boost.

On the bottom line the picture is less pretty, and this is likely one of the factors driving the stock price down. Despite erratic revenue growth, profit gains grinding to a halt as more competitors enter the yoga-wear market. Another factor plaguing profitability is that same store sales dropped 5% last period. Operating more stores with fewer sales invariably leads to lower earnings.

Wednesday - Costco

Costco (NASDAQ:COST), the second largest retailer in the United States behind only Wal-Mart (NYSE:WMT) reports 3rd quarter earnings on Wednesday. Costco has been steadily growing on the top and bottom line and the giant’s fundamentals jolted higher last quarter with growth coming in well above its average levels.

Costco announces its sales figures monthly on its website. Throughout October and November the wholesaler announced comparable sales growth between 4% and 5%. If it weren’t for the negative impact of the strong US dollar on international sales and deflating gasoline prices that growth would have come in between 6% and 7%. Analysts on Estimize are forecasting CostCo to power through limiting conditions and report a quarter slightly ahead of Wall Street’s forecast.

Wednesday - Ciena

Telecommunications networking equipment company CIENA (NYSE:CIEN) is also set for a Wednesday report. Ciena has now strung together 3 consecutive quarters of earnings beats and the Estimize community is looking for a fourth one midweek.

Although Ciena has beaten the Estimize community’s 3 times in a row, the stock has still fallen since the start of the year. Year to date shares of Ciena are down 28%. In early September Ciena beat earnings expectations for its summer quarter but cut its outlook for the current period. In its revised forecast Ciena warned that Wednesday’s report will contain sales between $570 million and $610 million, significantly behind expectations which were in the $630 million range.

Estimize contributors are projecting that Ciena will beat Wall Street’s earnings expectations by 2 cents per share and report sales of $594 million, slightly north of management’s guidance midpoint.