Monday’s a busy day for updates with purchasing managers indexes (PMIs) in the manufacturing sector. Several releases are revisions to the flash estimates for November that were previously released — Germany (08:53 GMT) and the Eurozone (08:58 GMT), for instance. As usual, the second round of PMI estimates aren't likely to change much from the earlier numbers, or so history suggests. By contrast, the surprise potential is higher with today’s first look at November manufacturing PMI data for Spain and Italy. Later, keep an eye on the debut of the US ISM Manufacturing Index for November.

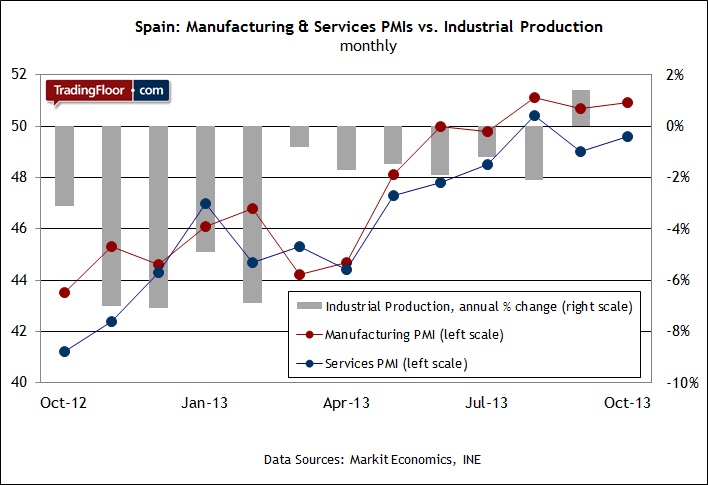

Spain Manufacturing PMI (08:13 GMT) Europe’s fourth-largest economy continues to dispense encouraging economic data. Spain is still deeply depressed, of course, but the numbers have been moving in a positive direction lately and so today’s PMI update for November will offer an early clue for deciding if the trend will roll on. Meantime, the latest hard data on industrial production paints an upbeat picture. Indeed, industrial output increased in September for the first time in more than two years on a year-over-year basis, the National Statistics Institute in Madrid reported last month.

An upbeat number in today’s PMI release for manufacturing would boost confidence that Spain’s recovery has momentum. The prospect of even tepid growth for this battered economy is crucial at a time of heightened worries about disinflation/deflation for the Eurozone overall.

Although last week’s flash estimate of November inflation inched higher to an annual rate of 0.9 percent vs. 0.7 percent in the previous month, the rate is still far below the European Central Bank’s (ECB) two percent target. “The overall assessment remains that inflation is very low,” an economist at Ernst & Young observed on Friday. “We think that the ECB needs to recognise the risk of deflation more clearly and act pre-emptively.” If one of Europe’s main macro burdens can continue to recover, the ECB’s job will be easier and the general outlook for the Eurozone brighter. Deciding if that’s still a plausible scenario begins anew this week, starting with today’s PMI update for Spain.

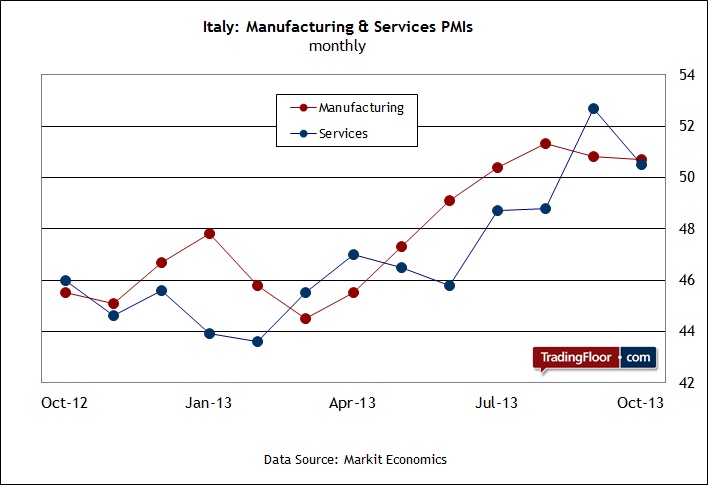

Italy Manufacturing PMI (08:43 GMT) Italy is still the weakest of Europe’s big-four economies, as suggested in last week’s retail PMI update from Markit Economics. Retail spending dropped at the fastest rate in four months, according to this survey data. The contraction marks nearly three years of falling sales. Unfortunately, there are few signs that the pain is ending. “The past two months have seen the pace of decline [in retail sales] quicken, leading businesses to further streamline their operations through more job cuts and inventory depletion,” an economist at Markit said in the November retail PMI report (pdf).

Meantime, Italy’s manufacturing and services PMIs hold out tentative signs of hope. Both indicators have remained above the neutral 50 mark in recent months, implying that the economy still has some modest capacity for forward momentum. But the tentative signs of recovery are vulnerable for a country that continues to struggle overall. The European Commission anticipates that Italy’s GDP terms will begin growing again next year, but only marginally. By contrast, Spain GDP has already turned the corner, rising 0.1 percent in this year’s third quarter.

“The real problem is that [Italy] has not grown for the past 15 years,” economist Luigi Zingales at the University of Chicago observed recently. If there’s any room for improvement on that dire state of affairs, the best hope lies in today’s PMI update. Some economists think we’ll see a slightly higher number for the November manufacturing survey data, which would suggest a slightly faster rate of growth for sector in the hard data releases to come. No one should confuse a bit of good news on this front as anything more than marginally upbeat news. But given the depth and breadth of Italy’s problems, any news that reflects progress on any level is critical at this stage for thinking that Europe overall isn’t in imminent danger of slipping into the business-cycle ditch.

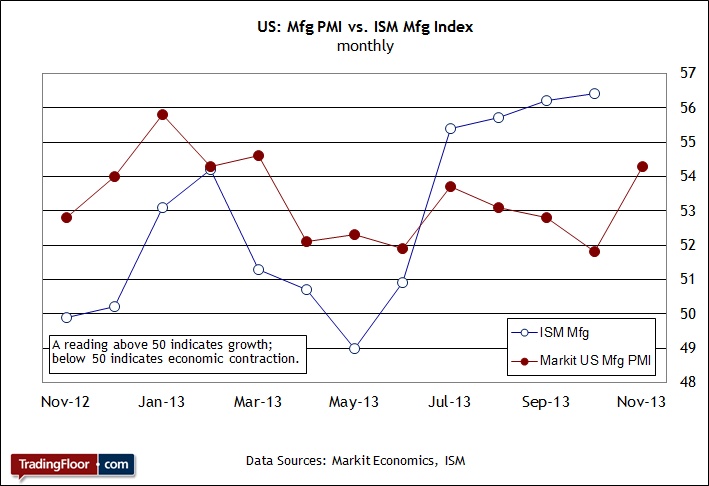

US ISM Manufacturing Index (15:00 GMT) The outlook for the US manufacturing sector has been murky lately, in part due to the recent divergence between a pair of competing measures of sentiment. But the flash estimate of Markit’s Manufacturing PMI data for November reflects a strong rebound after a run of weak monthly reports. “The PMI bounced back from the fall seen in October, linked to business returning to normal after the uncertainty and disruption caused by the government shutdown,” a Markit economist explained (pdf) last month. In turn, the revival suggests that the stronger ISM numbers of late are correct after all.

Economists think that today’s ISM release for November will post a moderate retreat, although my econometric modeling suggests that the decline will be milder than expected. In any case, it wouldn't be surprising to see a narrowing of the gap between the ISM and PMI numbers.

Meantime, today’s final revision for the PMI read on November (also scheduled for release today, at 13:58 GMT) will probably stick close to the previously published flash estimate. When the dust clears, it’s reasonable to assume that we’ll again see both manufacturing indicators pointing in a moderately bullish direction. In that case, the initial macro profile for the US economy will be off to an encouraging start for the November data. Keep in mind that the tailwind looks good overall, as reflected in the October numbers published to date (see my summary here). In addition, the latest decline in weekly jobless claims to the lowest level since September suggests that the labour market may perk up in this Friday’s payrolls report for November.

If today’s twin reports on manufacturing remain comfortably in growth territory, which seems likely, the case will strengthen for expecting positive updates for the US economy in the weeks ahead. As a result, it may be time to revise expectations up a bit for the US macro outlook.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

3 Numbers To Watch: Manufacturing In Focus For Spain, Italy & US

Published 12/02/2013, 04:32 AM

Updated 03/19/2019, 04:00 AM

3 Numbers To Watch: Manufacturing In Focus For Spain, Italy & US

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.