Structurally speaking, call and put options are relatively simple. A put option allows an investor to sell a security, usually though not always a stock, at a predetermined price. A call option allows that investor to buy a security at a predetermined price.

It’s simple to buy call or put options, as options are available on nearly every major exchange on the majority of stocks and exchange-traded funds.

An option provides a leveraged bet on the underlying security. That leverage increases both potential rewards and potential risks. Indeed, as the old Wall Street adage goes, “Options traders are like options: they usually expire worthless.”

What’s the Difference Between Call Options and Put Options?

| Call Options | Put Options |

| Gives the holder the right to buy shares | Gives the holder the right to sell shares |

| Option seller has unlimited risk | Option seller has limited risk, equal to the strike price multiplied by the number of shares involved |

| Option buyer has limited risk | Option buyer has limited risk |

What Is A Put Option?

A put option is a contract which assigns the buyer the right to sell one hundred shares of the underlying security to the seller. The transaction takes place:

- At a specified underlying price, known as the strike price;

- Before a certain date, known as the expiration date;

- For a total price known as the premium.

One important fact to keep in mind is that put options thus are bearish. A put buyer profits from a decline in the underlying security.

What Is A Call Option?

Conversely, a call option is a contract which allows the buyer to buy one hundred shares of the underlying security at a set strike price at any time before the expiration date.

In contrast to put options, call options are bullish. A buyer of a call option profits when the underlying security rises.

How Do Put Options Work?

The strike price and expirations for an underlying security are set by the options exchange. Heavily-traded stocks often have options with weekly expirations, as well as so-called LEAPs (Long-Term Equity Anticipation Securities), whose expiration is at least one year into the future. Issues with smaller volumes may only offer a handful of expirations that extend for as little as four to six months.

Both put and call options are quoted on a per-share basis, even though the contract covers 100 shares. The quote will include a ‘bid’, or the price the market maker will offer to buy the option. It will also include an ‘ask’, the price the market maker requires to sell the option. A put option asked at $2.00 will require a $200 total premium.

Strike prices generally are within range of the current trading price. It’s rare for an exchange to, for instance, offer a put option with a $100 strike price for a stock that only trades at $7.

In short, both the range of strike prices and the range of expirations vary widely among differing underlying securities. And those ranges can change over time. As demand rises and falls, new strikes and longer expirations can be added, or removed, based on market response.

How To Buy and Sell Put Options?

Call and put options can be purchased — and sold — through most major brokerages.

Buying a put option requires the investor only to put up cash or margin capacity equal to the premium required. The premium is the maximum risk to the trade. Investors buying a put option should use a limit order, ideally at a price below the quoted ask. The market maker may not accept the lower price; if desired, an investor can then raise the limit until an order is accepted.

But selling a put option is different. The maximum risk is far higher. It equals the strike price less the premium received. An option with a strike price of $50, sold for $5, can in theory lose $45 if the underlying stock goes to zero.

And so exchanges will require far more capital. One strategy is to sell what is known as a “cash-secured put,” in which the put seller uses existing cash in the account to cover the entire risk of the trade. This is the only strategy allowed in Individual Retirement Accounts (IRAs), which do not allow margin trading. Taxable accounts can use margin when put selling, but that creates a significant risk: that losses on the put sale can exceed the available cash in the account.

Call and Put Options Examples

As an example, ABC Corporation stock is trading at $100. A bearish investor will want to buy a put on ABC stock. But the nature of her bearishness will determine the strike price and the expiration she chooses.

For example, ABC might be releasing quarterly earnings in two days — and our investor believes the market will react poorly to the report. In that case, she’ll choose a cheaper, near-term expiration. Near-term call and put options are cheaper because they have a shorter time to expiration — and thus less time for the underlying stock to move.

Our investor might be bearish on ABC for more general, mid-term reasons. She might think the stock is simply overvalued and/or that business will decline in coming quarters. That thesis isn’t necessarily going to play immediately. Thus, she requires a longer-term expiration — which, again, will be more expensive than its near-term counterpart.

She next has to choose a strike price. The more aggressive the strike price, the greater the risk — and the greater the reward. An ‘out of the money’ option is an option that has no ‘intrinsic value’. In other words, if immediately exercised, the option is worthless.

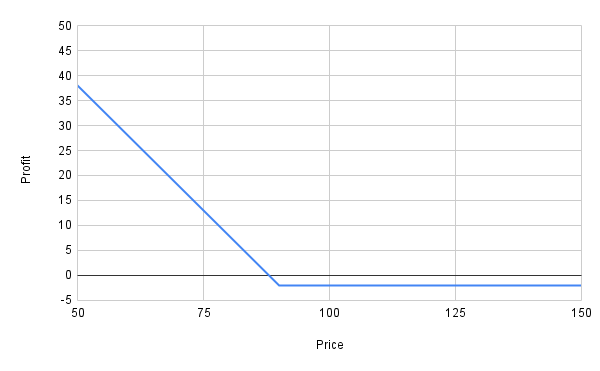

In our example, an ABC $90 put option with expiration a week out might only cost $2.00. But ABC stock must decline 10% by expiration for the option to have any value at all. ABC stock must fall 12% to $88 for the option trade to be profitable:

Of course, if ABC makes such a big move, the profits are huge. Should the stock fall to $85 after earnings, the option is worth $5, since our investor can sell an $85 stock for $90. She’s made a handsome 150% profit in a matter of days.

Perhaps the investor doesn’t believe ABC stock will necessarily decline that far. She can buy a put option with a higher strike price. The higher strike creates a higher breakeven — but also requires a higher price. The near-term $90 put option costs only $2; the 100 strike (known as ‘at the money’) could cost $7. That option breaks even at a higher level — ABC must only decline to $93 against $88 for the $90 strike — but offers lower rewards.

Going further, an ‘in the money’ option, which has intrinsic value, can be purchased. A $110 strike might cost $14, meaning ABC stock only needs to drop 4% to $96 for the trade to break even. But the price is higher and the rewards are lower. The same move to $85 that creates 150% returns in the $90 strike ‘only’ moves the $110 put from $14 to $25 — a smaller, though still-handsome, gain of 79%.

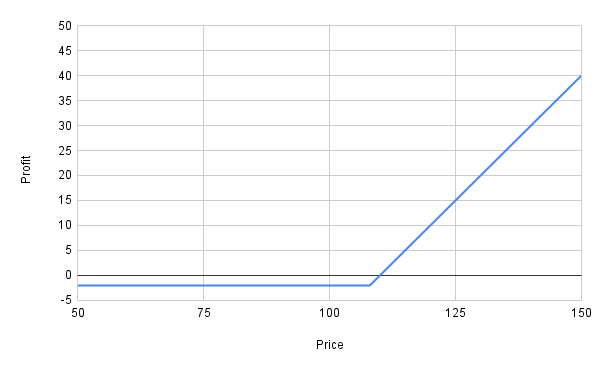

For call options, the math is simply reversed. Our investor might want to bet on a strong earnings report. The aggressive trade is an out-of-the-money near-term option, perhaps a 110 strike call that costs $2:

The stock now must increase 12%, to $112, for the trade to become profitable. Here, too, rewards are huge if the trade does work. A 20% gain to $120 means the option is now worth $8; our investor has quadrupled her money.

How To Exercise A Put Option

When an option trade is in the money, an investor will want to exercise that option. This is a relatively simple task. In fact, most brokerages will exercise in the money options automatically.

In theory, investors can exercise an option at any time before expiration. In practice, exercising a put option or a call option before expiration is a poor decision.

Exercising an option sacrifices the time value of that option, or the ability of the stock to move between the present and expiration. Should an investor want to take profits, she can simply sell the option on an exchange.

There are exceptions to the general rule, which arise mostly when an option is exceptionally close to expiration. But in most cases, exercising a put option or a call option gives up value — value other investors might be willing to pay for.

Call Options Vs. Put Options, Which Is Right For Me?

Traders do not need to limit themselves to either call options or put options. The essential mechanics are the same.

For an option buyer, the risk is capped at the premium, while the potential profit (almost always) is far higher. For an option seller, the profile reverses: losses can be enormous, while profits are limited to the premium received.

And so one way to think about the two sides of an option trade is that the buyer is betting on movement in the underlying stock, and the seller is betting against movement in the underlying stock. Technically, that movement is known as volatility. Indeed, the well-known CBOE Volatility Index, colloquially known as the ‘VIX’, is based on the pricing of options on the Standard & Poor’s 500 index.

Again, from a buyer’s perspective call options are bullish: the trader is betting on a move higher. Conversely, put options are bearish bets on a move lower. But in both cases the traders require a big move. Traders can lose on even an at-the-money or in-the-money option if the stock moves in the right direction, but doesn’t move enough.

There are scenarios in which a trader might be bullish long term, but have less conviction about near-term movement. In these scenarios, selling options is a viable strategy — because, again, selling an option is selling volatility in the underlying.

Selling puts is one such strategy. Whether on margin or a cash-secured basis, a put seller is betting that the stock won’t go down. That is not the same as betting that the stock will go up, or at least that it will go up quickly.

Investors can in fact sell puts not just as a trade, but as a hedged buy. Assume ABC stock trades at $45, but an investor would like to own it for $38. They can sell a put at the 40 strike for a premium of $2.

If the stock stays above $38, our investor makes a profit on the put sale. If it dips below $38, they own the stock at an effective price of $38, as in the put sale they agreed to buy the stock for $40 (and received $2 per share in cash in the process).

A covered call — in which an investor owns the underlying stock and then sells a call option — is the same trade from a different direction. In both cases, investors are giving up near-term upside as part of a plan for longer-term ownership.

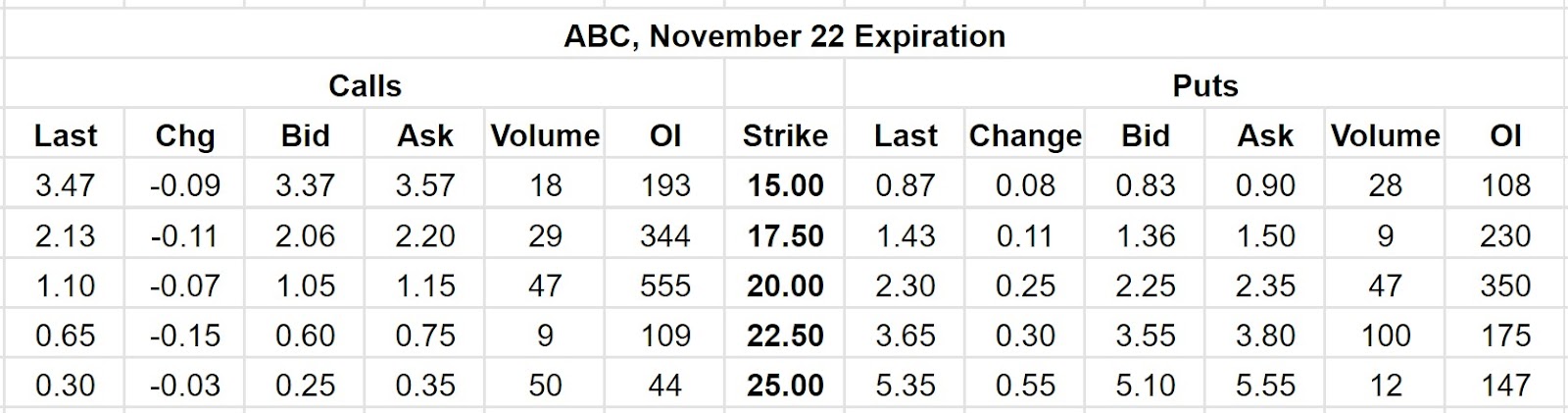

How To Read Options Tables

Option prices usually are listed in what is known as an “option chain”. Each expiration date will have its own chain, centered around varying strike prices, as this sample shows:

Generally speaking, call options are listed to the left, and put options to the right. The chain will list the “last” price at which the option traded hands. It will disclose the change (‘Chg’ in our sample) in price from the prior session close (not from the last trade).

The ‘bid’ represents the price at which the market maker will buy the option (whether a call or put option) at that strike price and expiration. The ‘ask’ is the price at which the market maker will sell that same option. The bid will always be less than the ask. The difference between the two, known as the ‘spread’, represents the market maker’s profit.

The chain should also detail information on trading activity. Volume represents the number of options (as with pricing info, this is the specific option at that expiration and strike price) traded that day. Open interest (often abbreviated as “OI”) represents the total number of contracts still outstanding. Some contracts can be closed, either through option exercise or, more commonly, through a trader reversing the trade (i.e., selling a put option they currently own).

All of these data points are important. The bid and ask show the actual cost of buying or selling an option at the moment. The spread represents a very real cost in executing the initial option trade — but also signals what the cost might be to close that trade. Spreads can eat up a chunk of profits, even if the trade winds up working out.

Volume highlights how interested traders are in the options (and the underlying stock) at the moment. Open interest can be a measure of sentiment: if open interest is heavier on calls than on puts, for instance, that suggests options traders are optimistic toward the stock.

This data alone can’t show whether an option trade is worth putting on. Traders need to have a thesis on the direction, timing, and strength of the move in the underlying stock. But option tables provide the data needed to devise the best trade to play that thesis.

Understanding The Risks In Options Trades

Again, options are leveraged bets. That provides higher rewards – and higher risks.

When buying a put option, the maximum loss is capped at that premium paid. But even more conservative option trades are risky. A long-term in the money put option can still expire worthless if the underlying stock rises. The bullish thesis underlying a call option may play out – but not fast enough.

Selling call and put options can be an even riskier trade. Remember, the potential loss in buying an option is capped to the premium paid. But when selling a call or put option, the maximum gain is capped at the premium.

An out-of-the-money put sale ahead of earnings might seem like an easy way to garner cash. But a poor earnings report could lead to losses that are multiples of the premium garnered.

It bears repeating: call and put options provide leveraged bets. That increases the rewards – and the risks.