What is Accrued Interest Receivable?

Accrued interest receivable refers to the interest that has been earned on an investment or loan but has not yet been received in cash. It arises in situations where interest payments are due at intervals (e.g., quarterly or annually) but are recognized in the financial records over time.

For example, if an investor owns a bond that pays annual interest, the interest will accrue daily or monthly, even if the actual payment isn’t made until the end of the year. The investor records the interest accrued until the payment is received, reflecting the earned amount as accrued interest receivable.

This concept applies to a wide range of financial instruments, including bonds, loans, and other interest-bearing assets.

How to Calculate Accrued Interest Receivable?

The calculation of accrued interest receivable is straightforward. The formula involves multiplying the principal amount by the interest rate and adjusting for the time period for which the interest has accrued.

The general formula is:

Accrued Interest Receivable = Principal Amount × Interest Rate × Number of Days Accrued / Total Days in Year

Here’s what the components mean:

- Principal Amount: The initial amount borrowed or the face value of the bond.

- Interest Rate: The rate at which interest accrues annually, expressed as a decimal.

- Accrued Period: The number of days the interest has been earned but not yet received.

- Total Period in a Year: It is typically 365 days, though for certain calculations, it could be adjusted for 360 days.

Example Calculation of Accrued Interest Receivable

Consider that an investor holds a bond with the following terms: following data:

- Principal Amount: $50,000

- Annual Interest Rate: 6% (expressed as 0.06 in decimal form)

- Interest Payment Frequency: Semi-annual (twice a year)

- Accrual Period: 90 days (from the date of the last interest payment)

- Days in the Year: 365 days (standard practice for most calculations)

The task is to calculate the accrued interest receivable for the 90-day period.

The formula for accrued interest receivable is:

Accrued Interest Receivable = Principal Amount × Interest Rate × Number of Days Accrued / Total Days in Year

Accrued Interest Receivable = 50,000 × 0.06 × 90/365

Accrued Interest Receivable = 50,000 × 0.01479 = 739.73

The accrued interest receivable for the 90-day period is $739.73. This represents the portion of interest that has already been earned but is unpaid for the 90 days.

The accrued interest receivable of $739.73 will be recorded in the investor’s books as follows:

- Debit: Accrued Interest Receivable (an asset account) — $739.73

- Credit: Interest Income (revenue account) — $739.73

This entry recognizes the interest income earned during the period, even though the cash has not yet been received.

Why is Accrued Interest Receivable Important?

Accrued interest receivable helps investors and businesses account for income as it is earned, not just when it is received. Even though the cash payment is deferred, the accrued interest is treated as an asset on the balance sheet. Below, we explore the key reasons why this metric is significant for investors.

Accurate Financial Reporting

Accrual accounting requires that interest income be recognized when earned, not when received. By accounting for accrued interest, businesses and investors ensure their financial statements reflect the true economic activity of the period.

Investment Performance Tracking

For investors, understanding accrued interest provides insights into the overall return on investments, especially in fixed-income securities like bonds. It helps gauge how much interest is accumulating between payment periods.

Tax Compliance

Accrued interest may have tax implications. For example, interest earned but not yet received may need to be reported as income, even if the payment is delayed. Properly tracking accrued interest ensures compliance with tax laws.

How to Interpret Accrued Interest Receivable?

Interpreting accrued interest receivable involves understanding its impact on an entity’s financial health and performance.

Asset for Investors

For investors, accrued interest receivable is a short-term asset on the balance sheet. It signifies the interest that has been earned but is yet to be paid. As the payment date approaches, the accrued amount is collected, converting the receivable into cash.

Impact on Profitability

Accrued interest contributes to the total income recognized in a given period, providing a clearer picture of profitability. Even if cash is not yet received, the interest is considered earned and must be reported as revenue.

Timing and Accrual Period

The timing of when interest is accrued affects how the asset is interpreted. A larger accrued interest receivable balance could indicate that interest payments are due soon, whereas a smaller balance could suggest payments are further in the future.

What Is a Good Accrued Interest Receivable?

A “good” accrued interest receivable balance depends on the specific circumstances of the company or investor. Generally, a good balance would indicate that:

- The interest is likely to be received soon. This is especially important for businesses that rely on timely cash inflows for operations.

- Interest payments are regularly scheduled. A consistent schedule of interest payments reduces the risk of non-collection.

- The company is able to manage its financial obligations effectively. This ensures that accrued interest receivable does not overwhelm cash flow management.

Limitations of Accrued Interest Receivable

While accrued interest receivable is crucial for financial transparency, there are some limitations to its use:

Cash Flow Timing Issues

Accrued interest receivable does not reflect the timing of actual cash flow. Even though interest may be recognized as earned, delays in payment can lead to discrepancies between reported income and actual cash received.

Risk of Non-Collection

In some cases, accrued interest may not be collectible if the borrower defaults or faces financial difficulties. This risk requires investors to assess the likelihood of receiving the interest payments on time.

Complexity in Long-Term Investments

For investments with long maturities or irregular interest payments, tracking and managing accrued interest can become complex. The longer the accrual period, the more difficult it may be to predict the exact amount of interest that will be ultimately received.

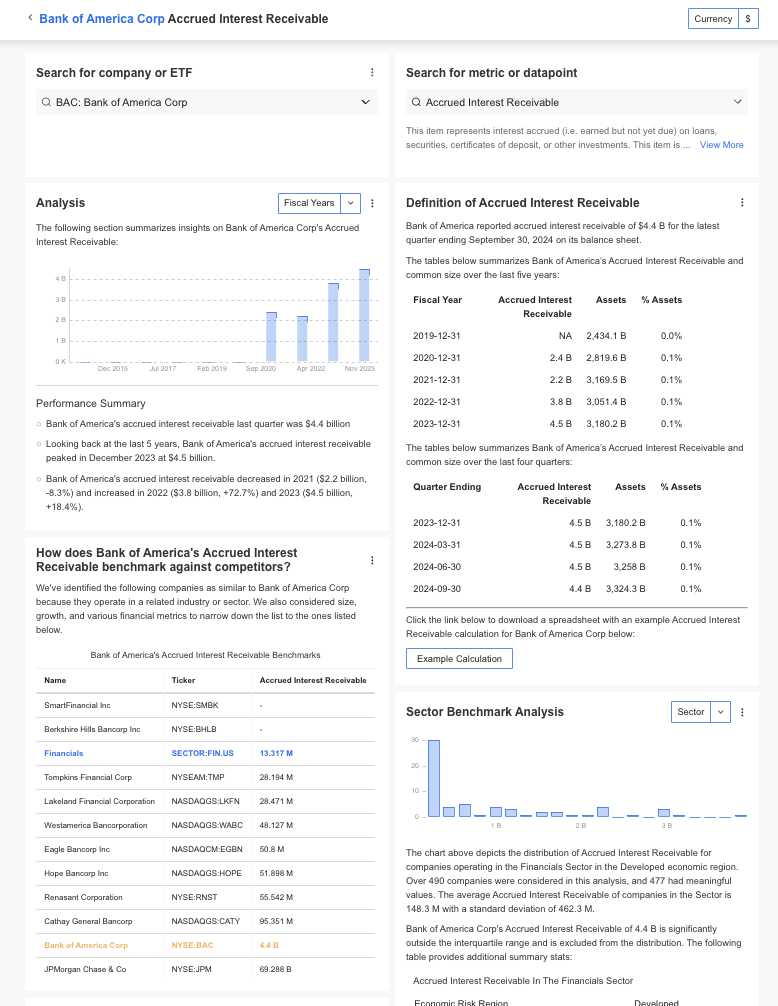

How to Find Accrued Interest Receivable?

InvestingPro offers detailed insights into companies’ Accrued Interest Receivable including sector benchmarks and competitor analysis.

InvestingPro+: Access Accrued Interest Receivable Data Instantly

Unlock Premium Data With InvestingPro 📈💸

Gain instant access to Accrued Interest Receivable data within the InvestingPro platform

🛠 Access to 1200+ additional fundamental metrics

🔍 Competitor comparison tools

📊 Evaluate stocks with 14+ proven financial models

Accrued Interest Receivable FAQ

What is the difference between accrued interest receivable and accrued interest payable?

Accrued interest receivable refers to interest earned but not yet collected, while accrued interest payable refers to interest owed but not yet paid. Both are tracked to ensure accurate financial reporting.

How does accrued interest impact tax filings?

Accrued interest income is typically taxable in the year it is earned, even if it hasn’t been received yet. Businesses and investors must report accrued interest as income, subject to applicable taxes.

Can accrued interest be waived or adjusted?

In some cases, companies may negotiate with debtors to defer or adjust interest payments. However, any changes must be reflected in the financial statements to maintain transparency.

Is accrued interest receivable a short-term or long-term asset?

Accrued interest receivable is typically a short-term asset unless the payment is due in more than a year, in which case it may be classified as a long-term asset.