(Bloomberg) -- The Federal Reserve published a fresh set of economic forecasts last week covering the next three years. Economists have been trying to make sense of the 2018 outlook ever since.

Here’s the conundrum. Fed officials raised their forecast for growth by four tenths of a percentage point for next year, to 2.5 percent. That’s comfortably above the 1.8 percent rate they estimate the economy can sustain in the long run.

The unemployment rate falls just two tenths more under that robust forecast to average 3.9 percent in the fourth quarter of 2018 -- well under their estimate of full employment. Inflation moves up to just under 2 percent.

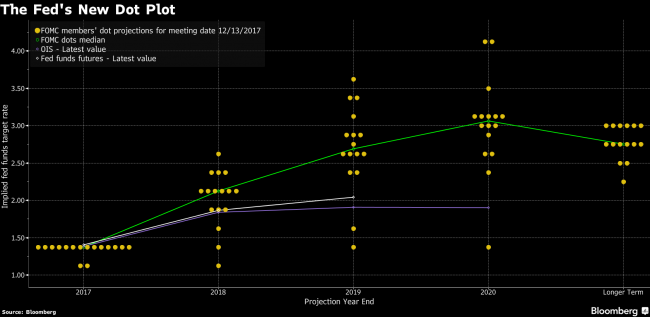

For all that, they kept their interest-rate projections for 2018 steady at three increases, presented in a dot-plot chart, to finish the year in a range of 2 percent to 2.25 percent. Put another way, the economy will run a lot hotter than the committee forecast in September, but the rate-hike path stays the same.

“The revisions to the forecast were inconsistent with the lack of revisions to the dots,” said Torsten Slok, chief international economist at Deutsche Bank AG (DE:DBKGn) in New York. “The number of dots should have gone up.”

Jerome Powell, nominated by President Donald Trump to replace Fed Chair Janet Yellen when her terms ends Feb. 3, discussed various “challenges” created by the dot plot in a February 2016 speech, including the fact that they are anonymous and quickly become stale.

If confirmed by the Senate, he’ll have a chance to do something about it under any review of the central bank’s communication strategy he decides to undertake. Meanwhile, economists are tossing explanations at the 2018 forecast to see if they can get something to stick. Here’s a look at some theories and where they might fall apart.

Positive Supply Side Shock

The economy can grow faster without much inflation if productivity suddenly picks up. The Republican tax plan currently being hammered out in Congress does create incentives for investment.

|

Caveat: It can take years for new investments to percolate through to higher productivity. If Fed officials really thought the economy was on the cusp of a supply boom, they would have raised their longer-run growth estimate. They didn’t. In her press conference, Yellen said she was uncertain about the tax plan’s supply-side benefits. |

Inflation Persistence

It may be that more Fed officials view inflation as less responsive now to low rates of unemployment. This was Yellen’s answer in her press conference: “You might think, well, shouldn’t I see more?” she said, referring to rate hikes, after cautioning that the projections are a mash-up of 16 different outlooks and not a consensus forecast.

“Well, okay, growth is a little stronger. The unemployment rate runs a little bit lower, that would perhaps push in the direction of slightly tighter monetary policy,” she said. “Counterbalancing that is that inflation has run lower than we expect, and, you know, it could take a longer period of a very strong labor market in order to achieve the inflation objective.

|

Caveat Fed officials did see inflation excluding food and energy rising to 1.9 percent at the end of next year, in effect reversing a soft spot that began in February. In other words, persistence fades at lower rates of unemployment.If officials believe it takes lower unemployment to get inflation moving, their estimate of the long-run sustainable unemployment rate should have moved lower from 4.6 percent. It didn’t. |

Politics

Goldman Sachs Group Inc (NYSE:GS). economists suggest Fed officials want to avoid showing an aggressive policy response on the eve of a vote on the Republican tax bill. “We think the monetary policy projections may be lagging the economic projections, perhaps in part due to political sensitivity,” they said in a note to clients on Dec. 13.

Bloomberg Economics chief U.S. economist Carl Riccadonna also thinks there was some political sensitivity that kept the committee from showing four hikes for next year. “The Fed is eager to avoid political meddling,” he said.

|

Caveat The Fed is in a period of transition. Powell is expected to take the helm in February, at which point Trump will have three vacancies to fill on the Board of Governors in Washington, including the influential post of vice chairman. Credibility is essential in times like this, and nobody expects Powell to squander what the Fed has built up over nearly four decades. |

Nevertheless, economists said the Fed is in show-me mode now with the tax package and inflation, while ready to move to faster hikes if necessary.

“If we saw of a series of inflation prints where inflation was moving higher, even just up to their target, we would see them be more aggressive on their rates,” said Robert Martin, an executive director at UBS Securities in New York and a former Fed economist.