(Bloomberg Opinion) -- Federal Reserve Chairman Jerome Powell was a lot more popular when stocks were setting records.

Now he and other Fed officials can’t seem to find friends anywhere they turn. President Donald Trump has lambasted the central bank several times since the S&P 500 peaked on Sept. 21. Investors questioned Powell when he remarked in early October that “we’re a long way from neutral at this point, probably,” pushing Treasury yields to the highest levels in years and sending equity prices tumbling. Bond traders held out a bit longer, pricing in two full 2019 interest-rate increases as recently as Nov. 8. They have since lost faith, too, seeing only one more move at best in the next 12 months.

For the first time since early 2017, the financial markets are truly fighting the Fed. U.S. equities are in outright revolt, with the S&P 500 falling to the lowest intraday level of the year on Tuesday. Parts of the Treasury yield curve inverted earlier this month for the first time in more than a decade, signaling that bond traders don’t see any real risk of rate increases in the years after 2020. Nor do they see many in the immediate future, either: The two-year yield is 2.66 percent, or just 40 basis points above the upper bound of the fed funds target rate. It’s by far the narrowest gap for the day of a Fed decision at which a rate hike was expected since June 2017. It was at a similar level in February 2017, when the market was unwilling to price in a March interest-rate boost until Fed speakers forced the issue.

This time around, the Fed seems more likely to cave to the markets’ demands. Odds are still in favor of policy makers raising the fed funds rate to a range of 2.25 percent to 2.5 percent on Wednesday — at this point, standing pat would probably raise more questions than just sticking to the plan. But the overwhelming expectation is for the Fed to communicate a dovish outlook, reiterating data dependency and perhaps even shifting down their median expectations for future interest rates. If they don’t, a whole bunch of markets look mispriced, most notably short-term rates.

Of course, Fed officials might just not care about investors being caught offside. After all, their mandate focuses on the labor market and price stability, both of which fall well within appropriate ranges: The unemployment rate is the lowest in 49 years and inflation is right around the central bank’s 2 percent target. Powell has called the U.S. economy “extraordinary,” referring to the combination of low unemployment, higher wage growth and seemingly lessened risk that prices will skyrocket.

Yet comments last month from Richard Clarida, the Fed vice chairman, betray that singular focus. He said that policy makers have to factor the outlook for global growth into their decisions and that there’s “some evidence that it’s slowing.” On top of that, domestically, Citigroup Inc (NYSE:C).’s U.S. economic surprise index is near the lowest since late August.

By all accounts, Powell doesn’t want the Fed to be viewed as the world’s central bank, nor does he want to be seen as subject to the whims of Wall Street. Under his leadership, the Fed has largely gone on tightening alone while the European Central Bank and Bank of Japan lagged behind. He has looked through emerging-market turmoil and volatility-inspired weakness in stocks. By and large, the message from the Powell Fed has been that the economy is strong, it can handle gradual rate increases, and policy makers are going to keep doing that until they see data that says they shouldn’t.

I’m not sure anything has changed much from that standpoint. That’s why my initial read on the reaction to Clarida’s comments was that bond traders were just hearing what they wanted to hear about the Fed slowing down. With the S&P 500 down an additional 7 percent since then, though, I’m no longer as convinced. Policy makers may attempt to ease the market angst with at least some combination of scaling back their projected pace of increases and removing the “further gradual” language.

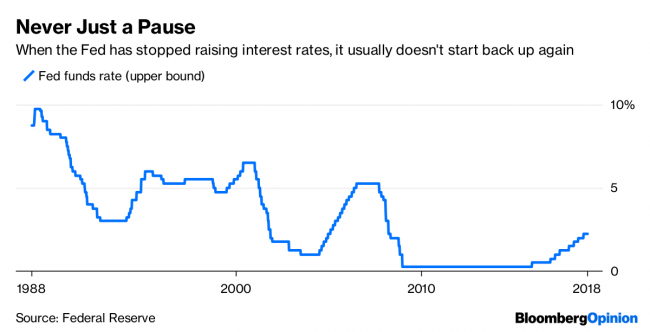

A telegraphed pause would probably bring some relief to markets into the end of the year. From the Fed’s perspective, the problem with a pause is that it’s never just that. A quick look at the fed funds rate shows that over the past 30 years, once the Fed stops tightening, it’s practically always followed eventually by a cut. Still, assuming the central bank moves on Wednesday as planned, the short-term rate will have increased by 2 percentage points since the beginning of December 2016. That’s quite an accomplishment considering just how long it remained locked near zero. If this is as far as the Fed can go, then it’s been a good run.

Bloomberg’s Fed reporters called this “perhaps its most scrutinized session in years,” and for good reason. Given the rapid market moves, there’s no way to interpret the central bank’s decision apart from them. The question, then, is if this latest bout of Wall Street turbulence is just another tantrum about higher rates, or if it’s truly sowing the seeds of a bear market and reflecting a dim view of the U.S. economy. Either way, the Fed doesn’t sound as if it wants to push its luck.

")