Next 6-12 months crucial for prediction platforms like Kalshi and Polymarkets

Introduction & Market Context

Olin Corporation (NYSE:OLN) presented its second-quarter 2025 earnings results on July 29, 2025, revealing a mixed performance across its business segments amid challenging market conditions. Despite reporting an unexpected earnings per share loss of $0.01 against forecasts of $0.02 gain, the company’s revenue outperformed expectations at $1.76 billion versus the anticipated $1.66 billion.

The market responded positively to Olin’s results, with shares rising 4.08% following the earnings release, suggesting investors were encouraged by the company’s revenue growth and strategic initiatives despite bottom-line challenges.

Quarterly Performance Highlights

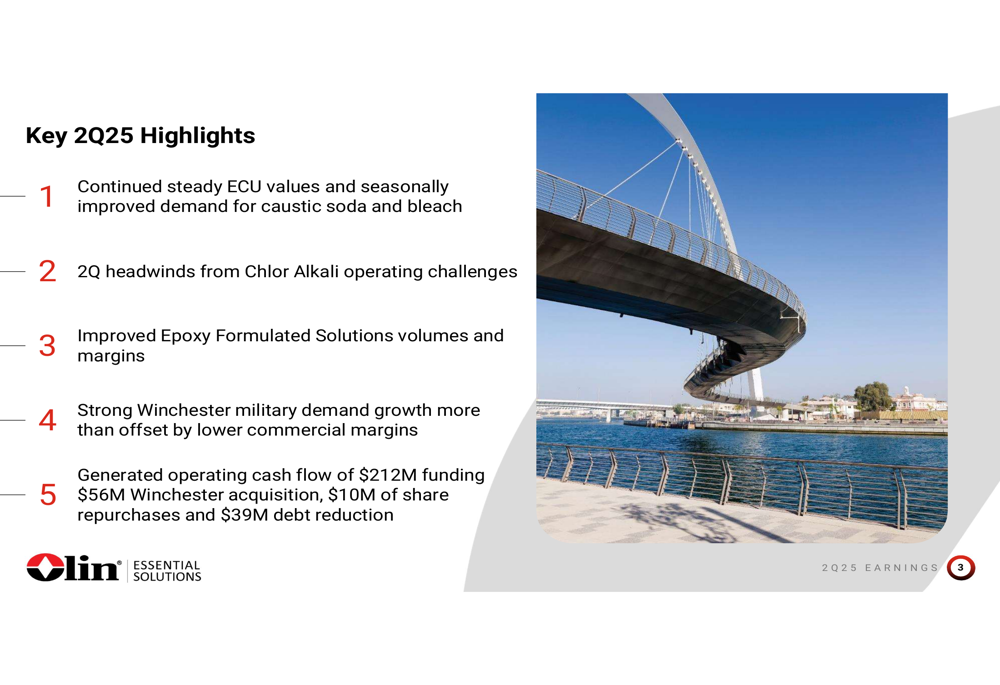

Olin reported second-quarter adjusted EBITDA of $176.1 million, down from $278.1 million in the same period last year. The company highlighted several key achievements, including strong cash flow generation of $212 million, which funded a $56 million Winchester acquisition, $10 million in share repurchases, and $39 million in debt reduction.

As shown in the following quarterly highlights slide:

The company’s performance varied significantly across its three main business segments:

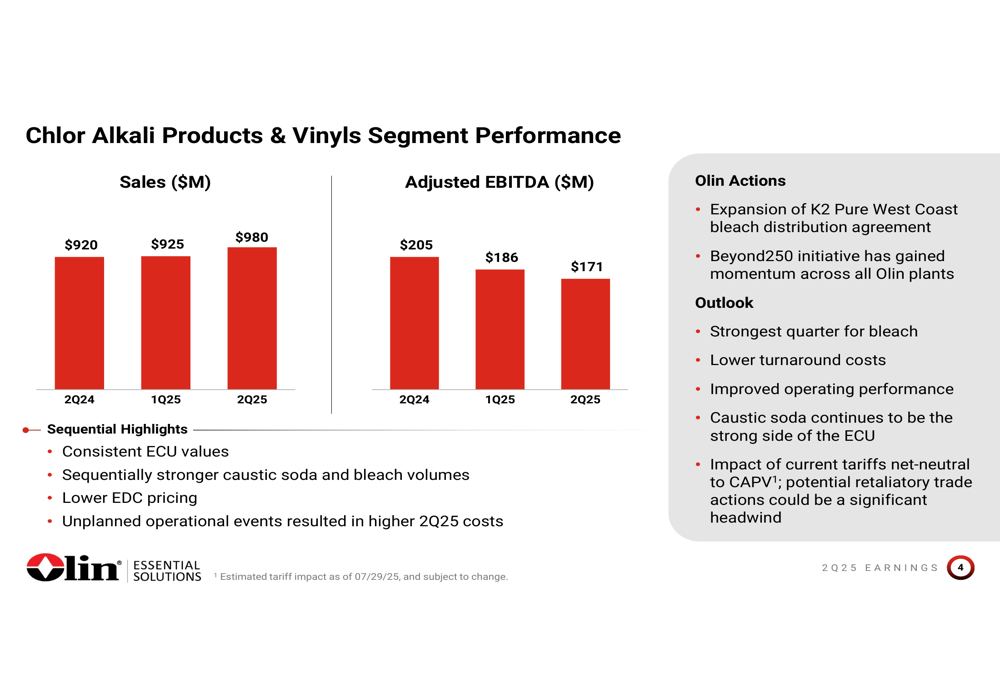

The Chlor Alkali Products & Vinyls segment saw sequential sales growth to $980 million in Q2 2025, up from $925 million in Q1, but adjusted EBITDA declined to $171 million from $186 million in the previous quarter. The segment benefited from consistent ECU values and seasonally improved demand for caustic soda and bleach but faced headwinds from unplanned operational events and lower EDC pricing.

The segment’s performance is illustrated in this chart:

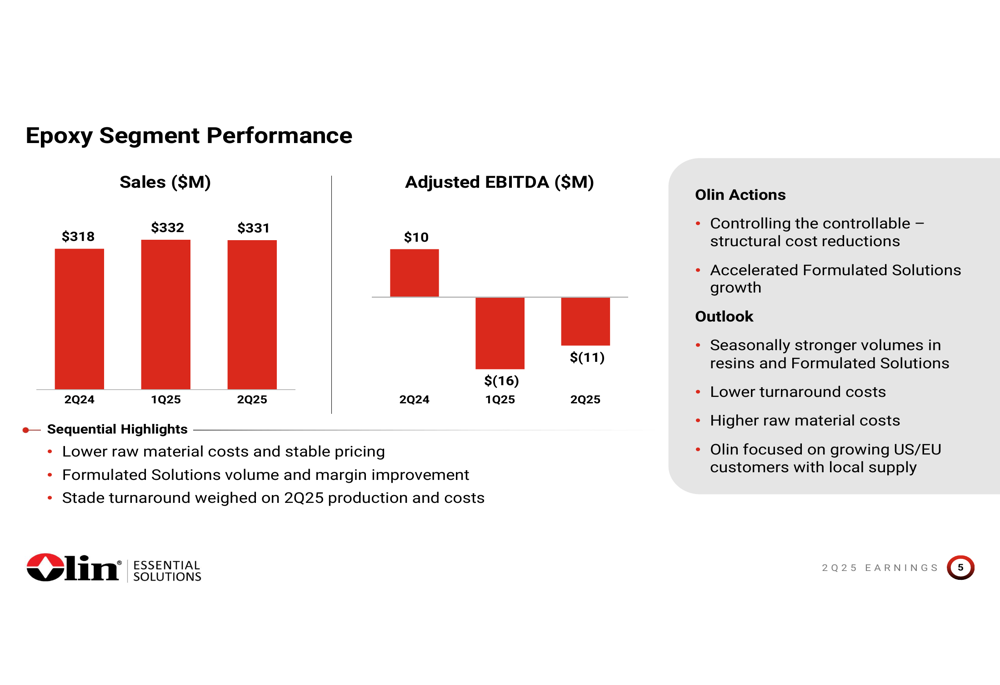

The Epoxy segment continued to struggle with negative adjusted EBITDA of -$11 million, though this represented a slight improvement from -$16 million in Q1. Sales remained relatively stable at $331 million. The segment saw lower raw material costs and improvements in Formulated Solutions volumes and margins, but these gains were offset by the Stade turnaround, which impacted production and costs.

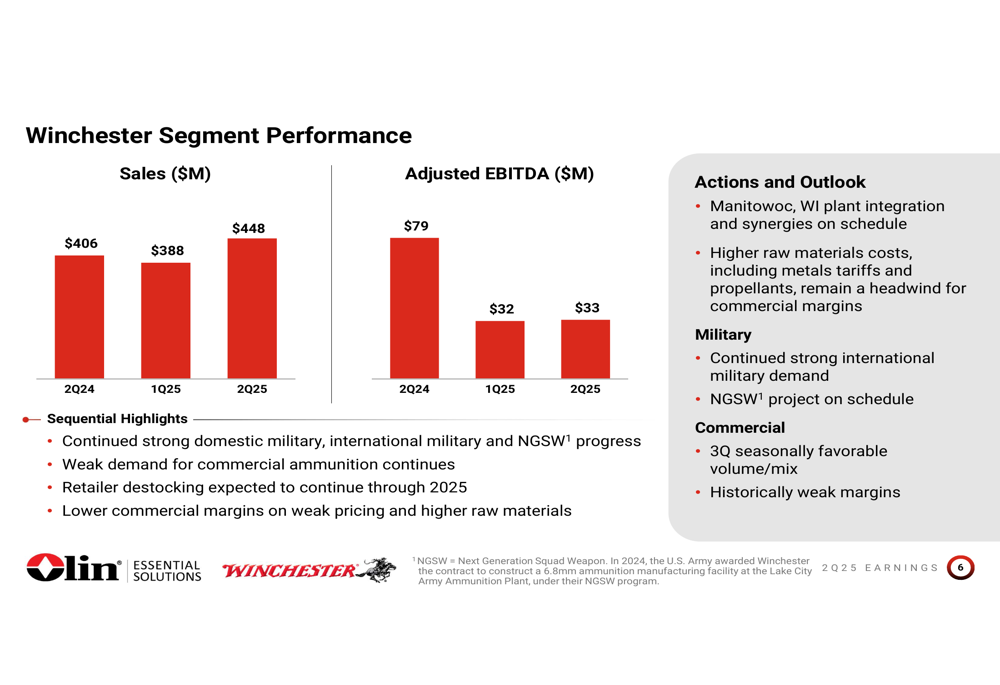

The Winchester segment showed the strongest sales growth, increasing to $448 million from $388 million in Q1, driven primarily by strong military and international military demand. However, adjusted EBITDA remained nearly flat at $33 million (versus $32 million in Q1) due to weak commercial ammunition demand, retailer destocking, and lower commercial margins.

Strategic Initiatives

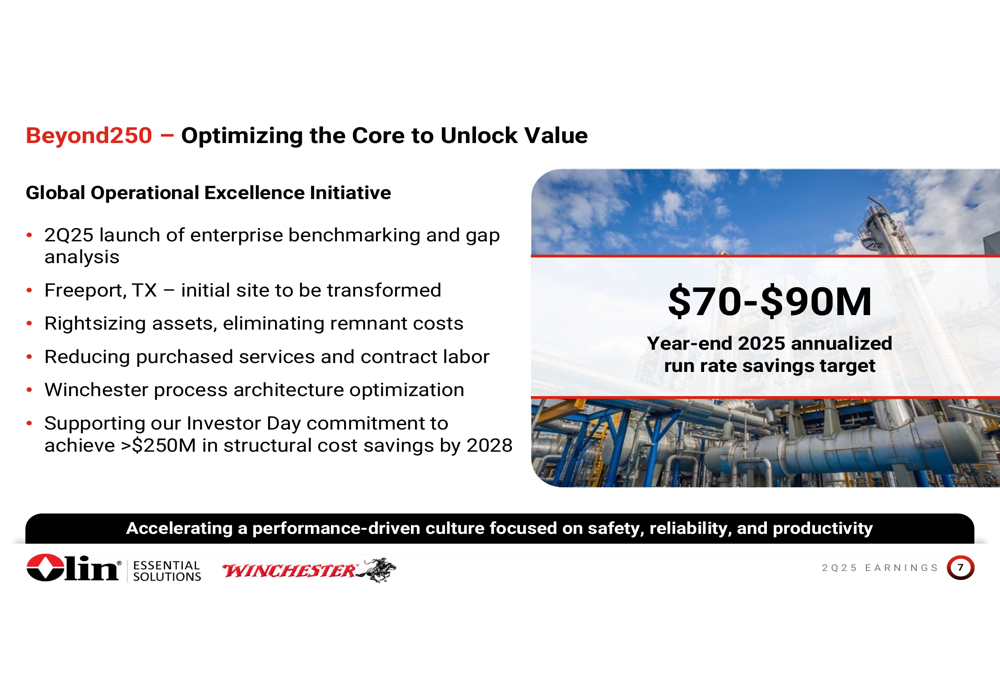

A central focus of Olin’s presentation was its Beyond250 initiative, a global operational excellence program targeting more than $250 million in structural cost savings by 2028. The company has set an ambitious year-end 2025 annualized run rate savings target of $70-90 million.

The initiative includes enterprise benchmarking and gap analysis, with Freeport selected as the initial implementation site. Key focus areas include rightsizing assets, reducing purchased services, and optimizing Winchester’s process architecture.

As detailed in this strategic initiative slide:

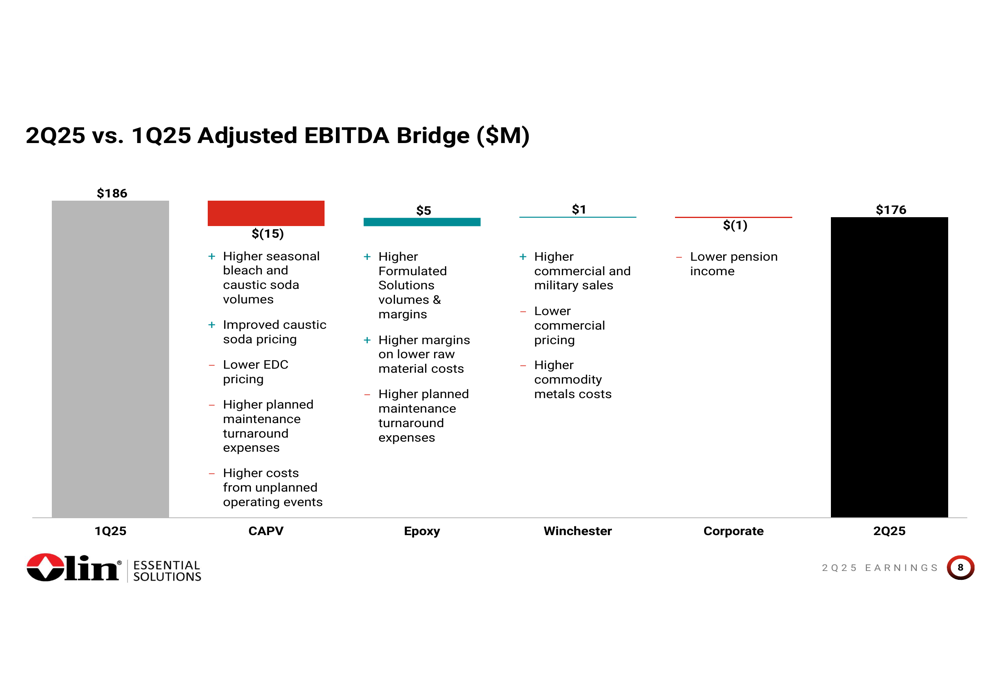

The company also highlighted its quarter-over-quarter EBITDA performance through a bridge analysis, which shows the factors contributing to the change from Q1’s $186 million to Q2’s $176 million in adjusted EBITDA:

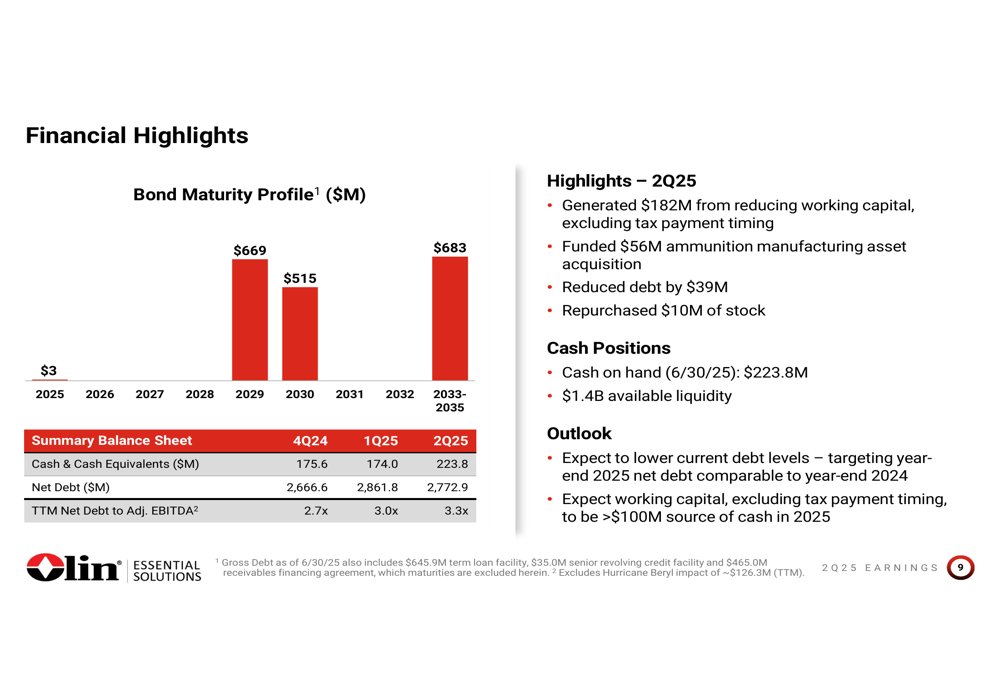

Financial Position

Olin maintained a solid financial position despite operational challenges. As of June 30, 2025, the company reported:

- Cash and cash equivalents of $223.8 million

- Net debt of $2,772.9 million

- Trailing twelve-month net debt to adjusted EBITDA ratio of 3.3x

- Available liquidity of $1.4 billion

The company’s debt maturity profile shows manageable near-term obligations, with significant maturities not occurring until 2030 and beyond. Working capital reduction generated $182 million in the second quarter, contributing to the company’s strong cash flow.

These financial metrics are presented in the following financial highlights slide:

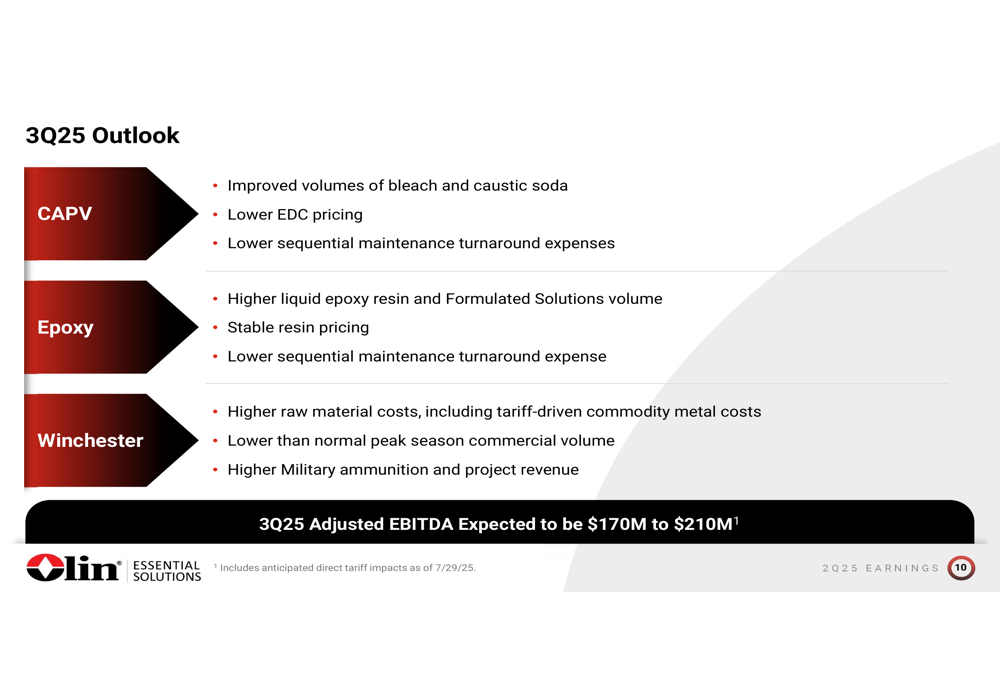

Forward Outlook

Looking ahead to the third quarter of 2025, Olin expects adjusted EBITDA to range between $170 million and $210 million. The company anticipates improved bleach and caustic soda volumes in its Chlor Alkali segment, higher liquid epoxy resin and Formulated Solutions volume in the Epoxy segment, and continued strong military ammunition demand in the Winchester segment.

However, the company also noted several headwinds, including lower EDC pricing, higher raw material costs (including tariff-driven commodity metal costs), and lower peak season commercial volume in Winchester.

The detailed Q3 outlook is presented in this forecast slide:

For the full year 2025, Olin provided several modeling assumptions, including:

- Capital spending of $200-220 million, expected to be above 2024 levels

- Depreciation and amortization of approximately $525 million

- Interest expense of $180-185 million, with about 40% of debt at variable interest rates

- Cash taxes of approximately $175 million

- Working capital expected to be a source of cash exceeding $100 million for the year (excluding tax payments)

During the earnings call, CEO Ken Lane emphasized the company’s focus on maintaining stability and generating value in challenging market conditions, stating, "We’re focused on being disciplined. We’re focused on being able to maintain stability with our portfolio to generate as much value as we can at the trough conditions that we’re in."

The company’s performance in the coming quarters will largely depend on its ability to execute the Beyond250 cost-saving initiative, navigate operational challenges, and capitalize on areas of strength such as military ammunition demand and improved caustic soda and bleach volumes.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.