- Yen falls as BoJ defies bets for more policy tweaks

- US retail sales and PPI data the dollar’s next test

- Wall Street at the mercy of data and earnings

Yen tumbles as BoJ keeps yield control policy untouched

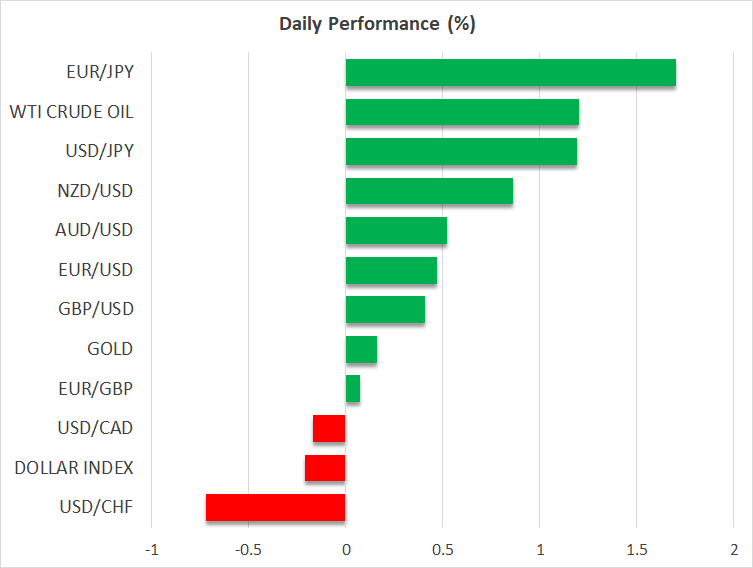

The protagonist in the first chapter of today’s FX episode is the Japanese yen, which came under strong selling interest after the Bank of Japan stuck to its ultra-loose monetary policy, disappointing expectations that it could further tweak its yield curve control policy.

Following the Bank’s decision last month to widen the band it sets around its 10-year bond yield target and heading into this meeting, there was speculation that officials may proceed with additional action to correct distortions in the yield curve. However, the only amendment officials did was to modify some operation rules so they can prevent long-term interest rates from rising too much.

Just ahead of the decision, the 10-year JGB yield was trading fractionally above the Bank’s upper bound of 0.5%, with the disappointment resulting in a 15bps drop to a low of 0.36%. Although the Bank will still have to strongly defend its band in coming weeks, speculation of imminent tightening may have cooled, especially with no new economic forecast at the March meeting.

However, that doesn’t mean the yen is headed for a trend reversal. With data later this week expected to show that underlying inflation continues to accelerate in Japan, investors are likely to maintain the view that the BoJ is starting its own tightening crusade at a time when the Fed is headed for the exit. They may have just decided to push their expectations to the April meeting, after Kuroda steps down.

Governor Kuroda has been adamant he is in no rush to dial back stimulus until wages rise enough to boost household income and consumption. So, with wages slowing notably in the last couple of months, waiting for April may be wiser now, as it will be the first gathering, not only under a new Governor, but also the first after the “shunto” spring wage negotiations.

Dollar traders lock gaze on retail sales and PPI data

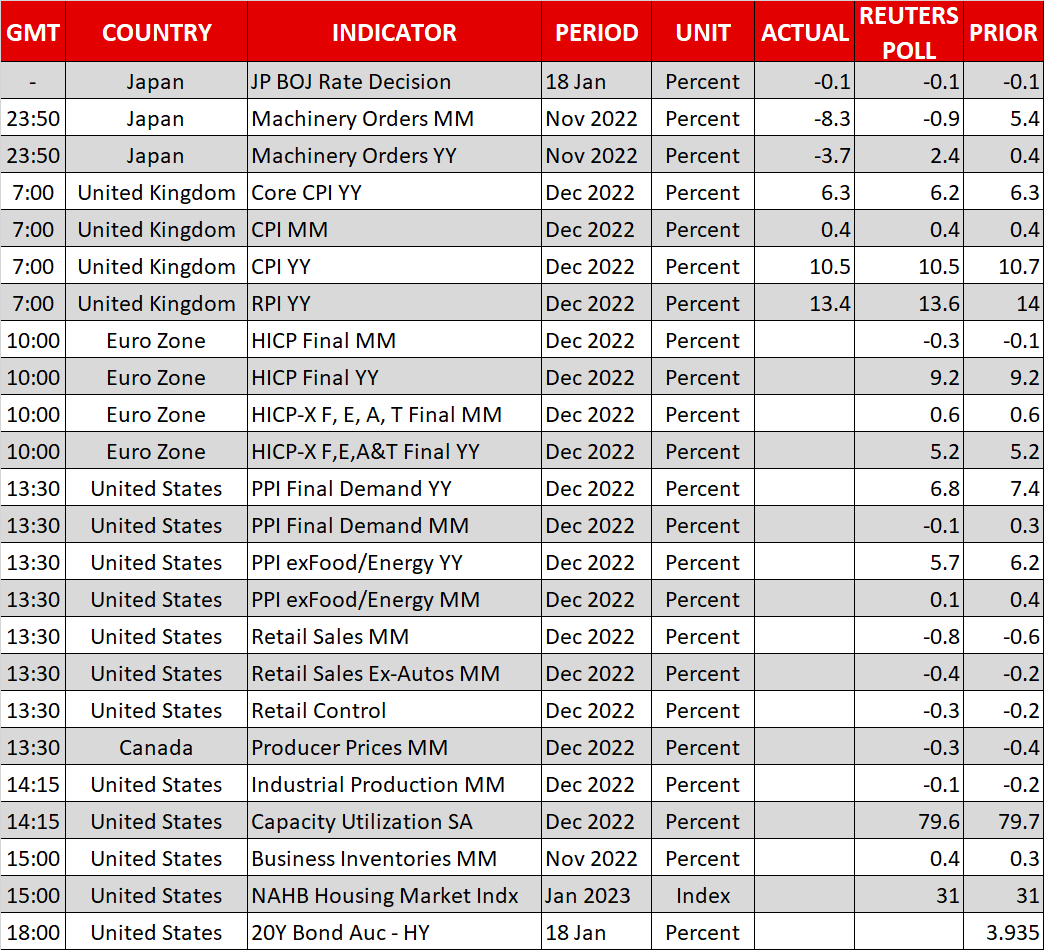

Later today, the spotlight is likely to turn to the US retail sales and PPI data for the month of December. Both headline and core retail sales are forecast to have declined further and more than in November, which means that consumers are becoming more reluctant to spend and thereby, inflation in the US could come further down in the coming months. This is also supported by the PPI forecasts. Both the headline and core PPI rates are expected to have continued declining, with the monthly headline print expected to tick into the negative zone just as the CPI rate did.

Another soft retail sales data set could also add to concerns about the performance of the US economy, especially following the slide of the ISM non-manufacturing PMI for December into contractionary territory. Ergo, expectations of softer inflation blended with concerns about the performance of the US economy could further solidify investors’ opinion that the effect of the prior interest rate hikes may not be fully reflected in economic data yet, and that consequently interest rates may need to be cut at some point later this year. This could possibly result in more dollar selling.

Wall Street awaits economic data amid earnings season

European equities closed at a fresh nine-month high on Tuesday, possibly boosted by a report that ECB officials are considering slowing their rate increments at the March gathering. Perhaps that’s also why the euro slid somewhat yesterday. However, market pricing is still pointing to a 50bps hike in February and nearly another one of the same size in March, which means that traders have not drastically altered their view after the report. Thus, expectations that the ECB could still continue tightening more aggressively than the Fed henceforth may result in another leg north in euro/dollar.

Despite the gains in European equities, the picture in the US was more mixed. The Dow fell more than 1% due to weak earnings from Goldman Sachs (NYSE:GS), but the surge in Tesla (NASDAQ:TSLA) retail sales in China helped the Nasdaq end the session in positive territory. Stock investors are likely to stay largely focused on the earnings season, but today they may also pay attention to economic releases. Disappointing retail sales may add to recession fears and result in some selling, especially with the S&P 500 hovering just below its key one-year downtrend line drawn from the high of January 4, 2022.