- Markets cautious before BoJ as traders on guard for another policy tweak

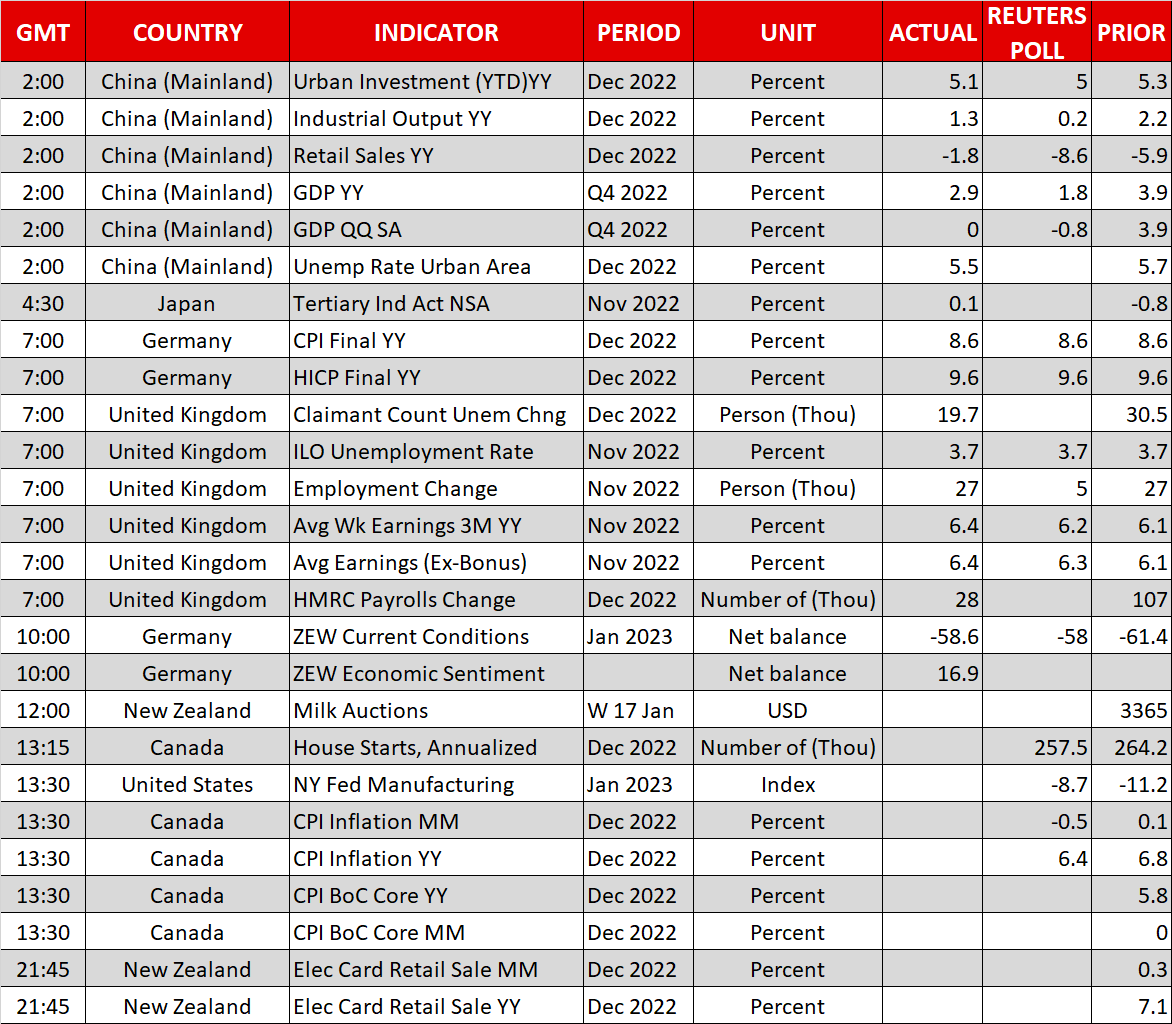

- China’s economy slows but avoids contraction, stocks turn lower

- Dollar steady as US data and Fed speakers eyed for direction

Yen rally takes a breather as BoJ awaited

The Japanese yen extended its retreat from its latest highs on Tuesday, though it was flat against the US dollar, amid intense speculation as to what the Bank of Japan will decide when it concludes its two-day policy meeting on Wednesday. There aren’t very high expectations of the BoJ pulling off another surprise tomorrow so soon after the December meeting when it caught investors off guard by widening the yield target band. But with Japan’s 10-year yield repeatedly breaching the upper cap of 0.50% in the last few sessions, a further adjustment in yield curve control policy cannot be ruled out.

The Bank of Japan has a real dilemma on its hands as the previous tweak failed in its objective of making yield curve control more sustainable. Thus, it’s questionable whether policymakers will be able to continue defending the upper yield cap until Kuroda’s replacement takes over the helm in April, as this requires heavy intervention in the bond market.

The worry is that if they opt for another tweak, the yield ceiling would likely come under attack again and so it might make more sense to abandon the controversial policy altogether. Traders are therefore going into the meeting better prepared this time, putting the yen’s ascent on hold for now.

Some caution despite China GDP beat

Overall, the mood was somewhat mixed on Tuesday as investors processed the latest growth data out of China while awaiting more clues on Fed policy from Wednesday’s US retail sales report and the FOMC members scheduled to speak this week.

Growth in the world’s second largest economy slowed to 2.9% year-on-year in the fourth quarter of 2022 and the figure for the whole year was 3.0%, well below the government’s target of around 5.5%. But the lifting of zero-Covid policies in December boosted both retail sales and industrial output during the month, beating the gloomy forecasts, and for the quarter, GDP defied predictions of a contraction, holding flat.

Whilst there are question marks about the reliability of the data given that right until the relaxation of Covid curbs began, large swathes of the country were in lockdown, the recovery is expected to gather more steam in the coming months and so the outlook remains positive. Beijing is determined to kickstart growth and more plans emerged today about further help for the country’s troubled property sector.

Lacklustre mood in stock markets

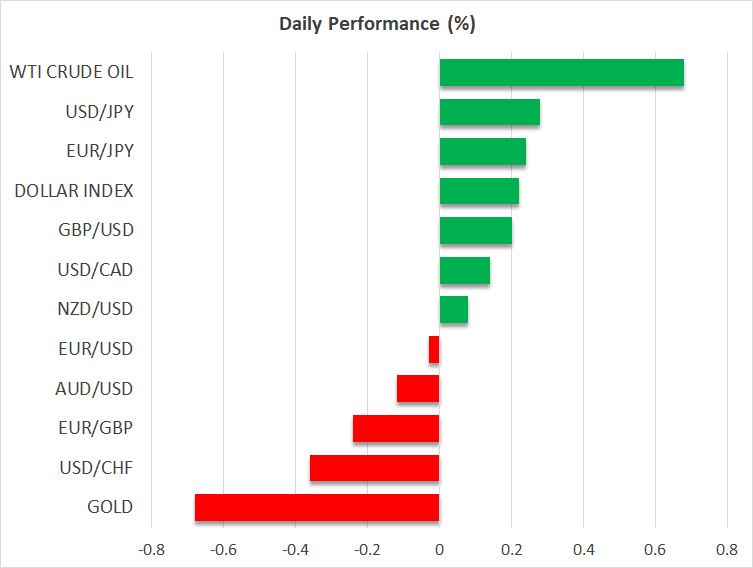

But in equity markets, US futures and Asian and European stocks were taking a break from the New Year rally to slip into the red.

With the earnings season getting underway and bond yields ticking higher this week, today’s caution seems warranted. Traders should find some direction when Wall Street reopens later on following yesterday’s holiday, and when the earning results from Goldman Sachs (NYSE:GS), Morgan Stanley (NYSE:MS) and United Airlines start flowing in. The risk that an earnings recession hasn’t been fully priced into US stocks hasn’t gone away, so the recent dip in volatility might not last much longer once the big guns start reporting.

Will policymakers dent optimism about end of rate hikes?

Elsewhere, the US dollar was trading marginally firmer against a basket of currencies, aided by higher Treasury yields, which in turn was weighing on gold. The precious metal has gained about 4.5% so far in 2023 on the back of growing investor confidence that inflation is peaking around the world.

This has given way to optimism that the Fed and other central banks will soon halt their tightening cycles, and even battered cryptocurrencies seem to be benefiting from this. Bitcoin has surged about 28% this year.

But there’s a danger that policymakers will once again push back against expectations of an early pivot. Investors will get to hear from the ECB’s Lagarde and SNB’s Jordan when they speak at the World Economic Forum in Davos later this week, while today, comments from the New York Fed’s Williams might draw some interest.