Following last week’s RBA monetary policy decision, this week, the central bank torch will be passed to the RBNZ. No policy changes are expected, but following the government’s decision to take measures against a heating housing market, it would be interesting to see whether officials will sound more dovish than previously.

The US CPIs for March and China’s GDP for Q1 may also attract special attention.

On Monday, we have no major economic releases on the agenda.

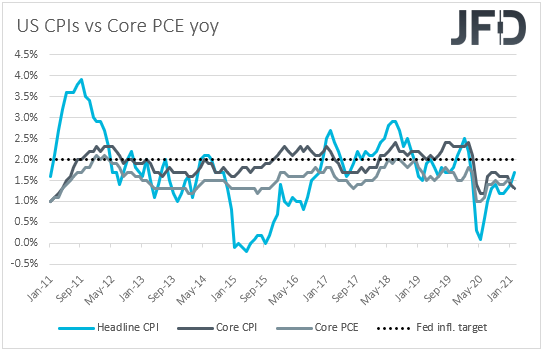

On Tuesday, the main item on the schedule may be the US CPIs for March. The headline rate is expected to jump to +2.5% yoy from +1.7%, while the core one is anticipated to rise to +1.6% yoy from +1.3%. This is likely to prove positive for the US dollar, but we don’t expect any recovery to last for long.

After all, the Fed has clearly noted that any surge in inflation this year is likely to prove to be temporary and that inflation will rise and stay above 2% for some time—the goal for beginning to normalize policy—in the years after 2023. Let’s not forget that Fed Chief Powell himself has been repeatedly stating that it is too early to start discussing policy normalization.

With all that in mind, we would expect the US dollar to pull back again soon, and equities to continue trending north.

As for the rest of Tuesday’s data, during the Asian session, we have New Zealand’s NZIER business confidence index for Q1 and Australia’s NAB business confidence index for March. That said, no forecast is available for either of those indicators.

China’s trade balance for March is also due to be released and the forecast points to a declining trade surplus, to USD 52.05bn from USD 103.25bn.

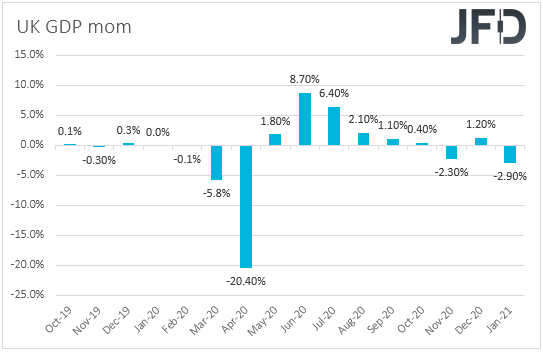

During the early EU morning, UK’s monthly GDP for February is coming out, alongside the nation’s industrial and manufacturing production rates for the month. No forecast is available for the GDP, but industrial and manufacturing productions are expected to have both rebounded +0.5% mom, after sliding 1.5% and 2.3% respectively.

This is likely to result in a slight improvement in GDP following January’s slump of 2.9% mom, but we don’t believe that this will be enough to support the recently wounded pound. Traders of the British currency stayed mostly focused on developments surrounding the AstraZeneca (NASDAQ:AZN) vaccine, with safety concerns raising fears that the UK’s successful vaccine rollout may slow down.

That may be the reason why the pound has been on the back foot recently, and as long as those concerns remain elevated, it may continue to perform poorly. The UK trade balance for February is also coming out, with the forecast suggesting that the nation’s deficit has widened somewhat.

Later in the day, Germany’s ZEW survey for April is due to be released. The current conditions index is expected to have risen to -52.0 from -61.0, while the economic sentiment one is forecast to have inched up to 79.5 form 76.6.

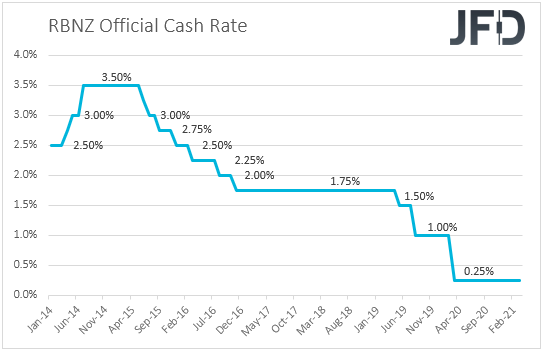

On Wednesday, during the Asian session, the RBNZ decides on monetary policy. At its previous meeting, in February, this Bank decided to keep its official cash rate and its Large-Scale Asset Purchase program unchanged, noting that they agreed to stay prepared to provide additional support if necessary, with the options including a lower OCR.

The kiwi slid initially, perhaps as the statement may have revived speculation over negative interest rates by this Bank, but it was quick to rebound, recover the losses, and trade even higher, perhaps as investors started scanning the quarterly Monetary Policy Report, in which the economic forecasts showed the OCR turning higher from December.

However, since then, data showed that New Zealand’s economy contracted in the last quarter of 2020, while the government decided to take measures in order to cool its hot housing market, including higher taxes. Those developments suggest that the RBNZ may push back the timing when it expects to start raising rates. Policymakers are expected to keep their monetary policy settings unchanged once again, and thus, all the attention may be on whether they will sound more dovish this time around.

In other words, it would be interesting to see whether they will keep the door for a rate cut open, and whether they will hint that interest rates are likely to stay low for longer than previously assumed.

If so, the New Zealand dollar is likely to come under selling interest. That said, we don’t expect this to result in a major downtrend, as the risk-linked currency may be helped by a potential further improvement in the broader market sentiment. We would prefer to exploit any kiwi weakness against the aussie. In AUD/NZD, any strengthening or weakening due to the broader market sentiment may be offset.

Thus, we believe that the main driver of this currency pair may be differences in monetary policy between the RBA and the RBNZ. With the RBA unlikely to ease policy further in the foreseeable future due to optimism with regards to its domestic economy, an RBNZ keeping the door open for lower rates and pushing back the timing of when it expects rates to start rising, may allow AUD/NZD to rebound.

As for the rest of Wednesday’s releases, the only one worth mentioning is Eurozone’s industrial production for February, which is expected to have contracted 0.9% mom after expanding 0.8% in January.

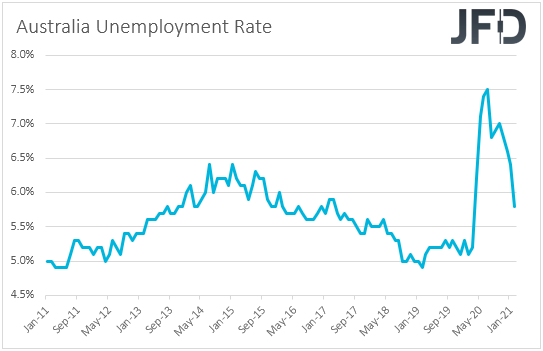

On Thursday, Asian trading, we get Australia’s employment report for March. The unemployment rate is forecast to have ticked down to 5.7% from 5.8%, while the net change in employment is forecast to show that the economy has gained 35.0k jobs, after adding 88.7k in February. A slowdown following February’s strong jobs growth appears more than normal to us, and thus, we would consider this to be a decent report.

At this month’s gathering, the RBA kept its policy unchanged, repeating that the economic recovery in Australia is well underway and that it is stronger than had been expected. Therefore, a decent employment report would add credence to that view and may diminish even further the chances for this Bank to ease policy further in the foreseeable future. This is likely to prove positive for the Australian dollar.

During European trading, Germany’s final CPIs for March are coming out and as it is almost always the case, they are expected to confirm their preliminary estimates.

Later in the day, we have the US retail sales and industrial production, both for March. Both headline and core sales are forecast to have rebounded 5.5% mom and 4.8% mom, after sliding 3.0% and 2.7% respectively, while IP is expected to have improved 2.8% mom after deteriorating 2.2%.

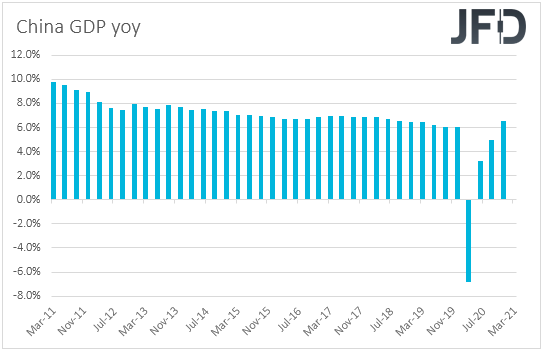

Finally, on Friday, during the Asian session, we get China’s GDP for Q1, as well as the nation’s industrial production, fixed asset investment and retail sales, all for March. GDP is expected to have slowed to +1.5% qoq from +2.6%. IP, fixed asset investment and retail sales are all expected to slow as well.

Having said that though, all prints are expected to stay on the strong side, with the yoy GDP rate anticipated to climb above 10% for the first time in a decade. Specifically, it is expected to jump to 18.9% from 6.5%, inflated by the coronavirus-related crash in the year-ago period.

Data supporting that the world’s second largest economy has recovered from the coronavirus-related damages and is now performing very well, may allow market participants to further increase their risk exposure.

Later in the day, we get Eurozone’s final CPIs for March, which are expected to confirm their preliminary estimates, as well as the US building permits and housing starts for March, which are forecast to have risen somewhat. The preliminary UoM consumer sentiment index for April is also coming out and the forecast points to a rise to 88.9 from 84.9.